Worldwide Wearable Inertial Sensors Market: Strategic Preview for 2026 Decision-Making

PW Consulting — Official Release

As enterprises finalize product roadmaps, R&D allocations, and M&A pipelines for 2026, the wearable inertial sensors market is entering a phase where near-term choices will determine competitive positioning for the remainder of the decade. PW Consulting’s new market study — using 2025 as its base year and projecting through 2032 — synthesizes historical performance (2020–2025), a rigorous forecasting model, primary vendor intelligence, and regulatory scenario analysis to translate market momentum into actionable strategy.

Worldwide Wearable Inertial Sensors Market

Macro Outlook: Growth with Direction

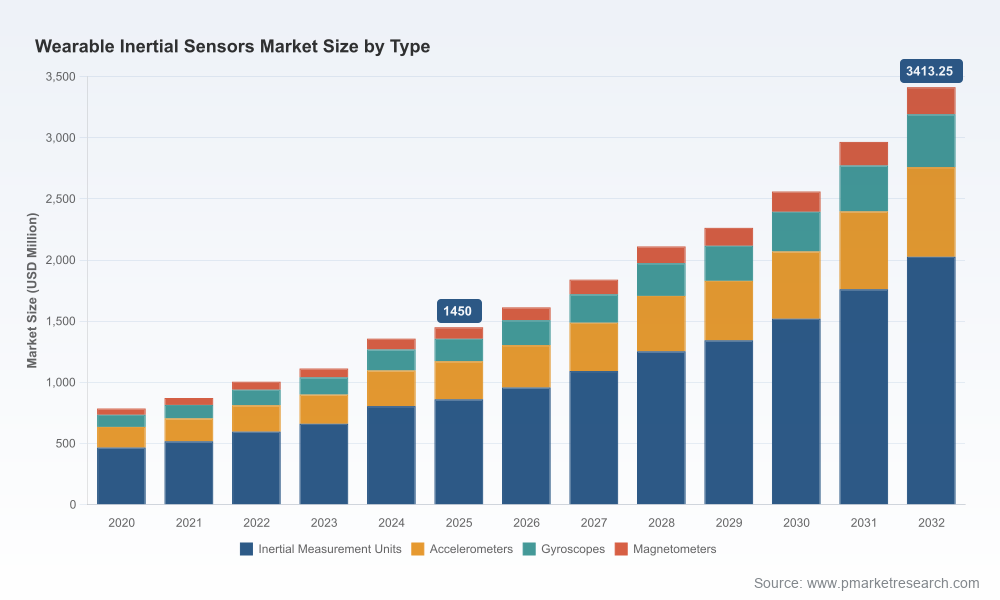

Wearable inertial sensors have moved from niche instrumentation toward foundational building blocks of next-generation consumer and clinical devices. Our report quantifies that transition: the global market expanded from under USD 800 Million in 2020 to roughly USD 1.45 Billion in 2025, with our forecasting framework projecting continued expansion to about USD 1.61 Billion in 2026 and climbing to approximately USD 3.41 Billion by 2032. That trajectory reflects an expected compound annual growth rate (CAGR) of roughly 13.01% across the forecast window (2026–2032).

Worldwide Wearable Inertial Sensors Market

Two implications stand out for 2026 planners. First, the market’s scale and growth profile justify near-term investment in sensor-enabled product variants and embedded signal-processing capabilities. Second, the pace of adoption and supplier concentration dynamics mean that timing—rather than simply capability—will be a decisive factor for capturing share in high-value segments.

Worldwide Wearable Inertial Sensors Market

Why This Report Matters for 2026 Decisions

- Investment Prioritization: The market’s mid-teens CAGR signals expanding addressable opportunities but also intensifying supplier competition. Our report maps where device makers and systems integrators should allocate incremental R&D versus where strategic partnerships or licensing make more sense.

- Product Roadmaps: Miniaturization, power-efficiency, and embedded AI are converging. The study identifies practical product architectures and implementation trade-offs to accelerate time-to-market without compromising regulatory readiness.

- M&A and Partnership Playbooks: With a moderately concentrated vendor landscape, 2026 is a pivotal year for bolt-on acquisitions and technology licensing to accelerate access to validated IMU stacks and sensor-fusion IP.

- Regulatory & Reimbursement Navigation: The report provides an actionable framework for classifying device risk, aligning to international standards, and scoping clinical validation to support market access and reimbursement conversations.

What the Report Contains — Practical, Executable Intelligence

Beyond headline forecasts, this study is designed as an instrument for decision-makers. Key deliverables include:

- Transparent modelling files and scenario runs (base, upside, downside) that let users stress-test assumptions against price erosion, component shortages, and accelerated standards adoption.

- Vendor benchmarking and a segmentation-agnostic vendor matrix focused on product maturity, integration support, power/size trade-offs, and embedded compute capabilities.

- A go-to-market toolkit for device OEMs: procurement scorecards, sample contract language for sensor supply and calibration services, and a checklist for in-field validation and post-market surveillance.

- Regulatory readiness playbook: mapping of FDA and EU requirements, template clinical evidence plans for different intended uses, and a compliance timeline calibrated to 2026 submission cycles.

- M&A guide and valuation heuristics tailored to sensor and system integrator targets — including revenue multiples by maturity band and estimated time-to-synergy for platform integrations.

Competitive Landscape: Profiles and Strategic Postures

The wearable inertial sensors market blends legacy MEMS suppliers, precision-sensor specialists, and vertically integrated wearable-system companies. Our analysis distills strengths and strategic moves by key players to help buyers and investors orient quickly.

- Bosch Sensortec (Germany) — A leader in ultra-low-power IMUs designed for consumer wearables and hearables. Their product family targets compact form factors and integrated sensor-fusion, making them a default choice for high-volume consumer designs where power budget is a primary constraint.

- STMicroelectronics (Switzerland/France) — A significant MEMS and IMU supplier that has been pushing embedded AI processing into package footprints. Recent launches further position ST as a supplier that can offload basic activity classification to the sensor, reducing system-level compute needs.

- TDK InvenSense (United States) — Known for high-performance MEMS IMUs widely used across wearables and smartphones. Their strength is in scale and the high-integrity motion sensing demanded by complex consumer and mixed-reality use cases.

- Analog Devices (United States) — Focused on precision IMUs where accuracy and stability matter for clinical and professional applications. Their portfolio is attractive for entrants targeting premium clinical-grade devices and instrumentation.

- Movella / Xsens (Netherlands/United States) — Specializes in wearable motion-capture systems for biomechanics and real-world movement analysis. Their strength is system-level sensing and validated algorithms for research-grade motion tracking.

- Shimmer Sensing (Ireland) — Provides wearable IMU platforms targeted at clinical research, with prior medical-class certification experience — a differentiator for customers pursuing regulated clinical studies.

- Noraxon, BTS Bioengineering, QSense Motion, ActiGraph, 221e — These firms occupy niches spanning gait analysis, clinical biomechanics, high-fidelity research platforms, and miniaturized medical-grade IMU solutions with embedded AI. Their market roles vary from OEM suppliers to full-stack device vendors.

Market concentration is meaningful: the combined share of the top three and five firms indicates moderate to high consolidation at the supplier level, elevating the importance of vendor selection, multi-sourcing strategies, and long-lead procurement hedges for device OEMs.

Regulatory and Standards Dynamics: Calibration for Compliance

Regulation and standardization are active forces shaping product design and commercialization schedules in 2026. Notable dynamics covered in the report include:

- FDA maintains a public database of authorized sensor-based digital health technologies; its posture increasingly distinguishes low-risk consumer wellness devices from regulated medical devices. A January 2026 guidance clarified that low-risk non-medical fitness devices will face limited FDA oversight — but devices that make clinical claims remain squarely within the agency’s purview.

- In the EU, MDR 2017/745 and associated IEC/ISO standards (such as IEC 60601, ISO 14971, and ISO 13485) continue to dictate device classification and lifecycle obligations. Manufacturers targeting European clinical markets must align product development and quality management timelines accordingly.

- Class I medical certifications for wearable IMU platforms exist and have precedent in the market, enabling commercial pathways for clinical research and low-risk medical use-cases; however, higher risk clinical functions will require more extensive evidence generation.

Recent Market Signals and What They Mean

- Product innovation continues at the sensor level: new IMUs integrating embedded AI capabilities are enabling on-chip preprocessing and event detection, which helps conserve battery life and simplify system architectures.

- IP activity around biometric authentication and touchless interfaces underscores adjacent value pools — companies active in gesture and biosignal fusion are creating optionality for authentication, safety, and personalization features in wearables.

- Component supply and MEMS roadmaps remain central: suppliers who combine low power with reliable scale will exert outsized influence on product roadmaps for consumer and clinical OEMs alike.

How to Use This Report in 2026

Executives, product leaders, and investors should treat this study as a decision-support instrument rather than a static market summary. Practical next steps we recommend for 2026:

- Run the included scenario files with your unit-cost and ASP assumptions to identify break-even points for sensor upgrades or embedded-AI add-ons.

- Map existing supplier relationships against our vendor matrix to reveal single-source risks and opportunities for strategic dual-sourcing.

- Use the regulatory checklist to align clinical validation timelines with planned launches, avoiding common rework and submission delays.

- For investors and M&A teams, apply the valuation heuristics and synergy timelines to prioritize targets that deliver immediate integration wins (e.g., validated IMU stacks, sensor-fusion IP, or regulatory-certified sensing platforms).

Conclusion — A Tactical Preview That Invites Deeper Engagement

The wearable inertial sensors market is growing rapidly and maturing unevenly across use cases. For firms that move decisively in 2026—investing in the right sensor capabilities, de-risking supply, and aligning regulatory strategy—the opportunity is substantial. PW Consulting’s report balances strategic foresight with hands-on tools to accelerate those moves. This preview is intended to demonstrate the report’s strategic depth while reserving full, segment-level intelligence and detailed vendor scoring for the full study.

To access the complete dataset, vendor matrices, scenario files, and the regulatory playbook that underpin these insights, please visit our official report page and download the full Worldwide Wearable Inertial Sensors Market study.

For detailed analysis of this topic, please visit the official page:Worldwide Wearable Inertial Sensors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com