Patient Engagement Technology Market Size, Share & Growth Forecast 2025–2031

Other |

2026-07-14 14:17:45

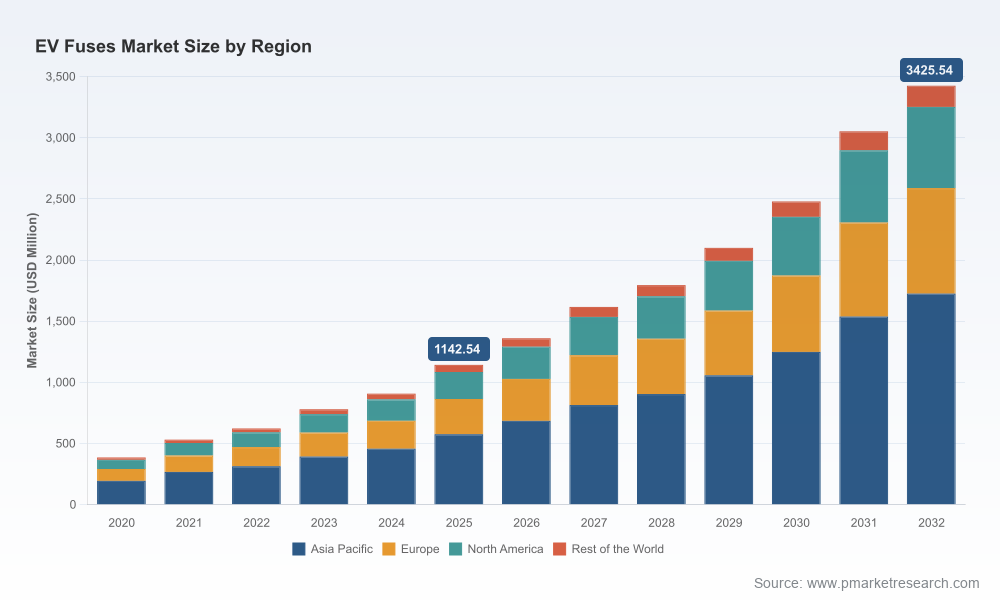

PW Consulting’s latest market study on the Worldwide EV Fuses Market provides an evidence-based roadmap for executives, product leaders, procurement chiefs and investors who must make binding decisions in 2026. Our proprietary model traces the market from its 2020 baseline through a 2025 reference point and projects forward across 2026–2032. The market expanded from roughly USD 385 million in 2020 to about USD 1,143 million in 2025 and, under our central-case assumptions, is forecast to reach USD 3,426 million by 2032 — a period CAGR of 16.98% for the 2026–2032 forecast window. These headline dynamics create both strategic urgency and clear windows for value capture.

Worldwide EV Fuses Market

Electrical safety is now a system-level differentiator for EV platforms. As voltage architectures climb and energy density increases, fuses shift from passive commodity parts to critical safety components that influence pack architecture, thermal design, and certification timelines.

Worldwide EV Fuses Market

Supply-side pressure is tangible. Raw material dynamics — notably record-high copper prices in early 2026 and the persistent step-up in copper intensity of EV platforms — raise cost and sourcing risk for fuse manufacturers and OEMs alike.

Worldwide EV Fuses Market

Regulatory and standards complexity is growing. Compliance requires coordinated engineering, validation and supplier management across ISO 8820, AEC‑Q200, UL 248‑20, IATF 16949 and relevant IEC families. Missing these checkpoints delays vehicle launches and can create warranty and liability exposure.

Market structure favors scale with specialization. Our concentration analysis shows a market where the top-three suppliers capture a material share and the top-five further consolidate power — a dynamic that changes how new entrants and Tier‑2 vendors should approach partnerships and niche plays.

Transparent market-size trajectory and sensitivity testing: annualized historical series (2020–2025), a 2026 baseline build, and scenario-driven forecasts to 2032 with upside/downside pathways and sensitivities to copper, EV production, and regulatory change.

Supply-chain heatmaps and cost-to-produce models: bill-of-materials and process-cost breakdowns to quantify the impact of copper and ceramic inputs on unit economics at different production volumes.

Technology deep dives: end-to-end engineering notes on pyro fuses, high-voltage DC fuses, PCB through-hole solutions and integrated fuse‑contactor hybrids — including test failure modes, thermal derating guidance and qualification roadmaps aligning to automotive standards.

Competitive playbooks and supplier scorecards: qualitative and quantitative assessments of leading OEM suppliers, their product breadth, manufacturing footprint, design wins and likely strategic moves over the next 12–24 months.

Commercial execution tools: procurement negotiation templates, price-index clauses tied to copper benchmarks, and go-to-market frameworks for suppliers seeking OEM/Tier‑1 adoption.

M&A and investment matrix: prioritized capability targets — e.g., high-voltage pyro manufacturing, semiconductor-protection fuses and intelligent fuse/contactors — with valuation anchors and integration risk checklists.

Note: this press summary highlights the report’s scope and strategic value. Detailed regional and application-level segmentation tables, supplier share-by-node, and project-level customer footprints are intentionally excluded from this release to preserve the full report’s value proposition.

Littelfuse, Inc. (Chicago, USA) — breadth and engineering depth: a comprehensive range of high-voltage automotive fuses positions Littelfuse as a go-to for passenger and commercial EV battery packs, power distribution and charging systems. Their portfolio approach supports OEMs seeking one-stop sourcing and rapid qualification cycles.

Eaton Corporation (Dublin, Ireland) — scale and system penetration: with the Bussmann line and dedicated EV fuse assembly facilities, Eaton combines production scale with a product suite that spans pyro protection and energy‑storage applications. Their capacity expansion signals intent to compete on global supply security.

Mersen S.A. (Paris, France) — semiconductor‑centric protection: Mersen’s focus on high-performance fuses for inverters and battery systems makes it a strategic partner for electrified drivetrain and power-electronics suppliers where high-current semiconductor protection is the priority.

PACIFIC Engineering Corporation (Japan) — legacy specialization: a long history in EV and pyro fuses and recent catalog updates for higher-voltage systems underscores PEC’s role as a reliable supplier for high-voltage OEM architectures, particularly where tight quality control and Japan-origin supply matter.

SCHURTER, Bel Fuse, SOC, Daicel, Autoliv, Sensata, ABB, Siemens — differentiated vectors: these suppliers compete on axes such as high-voltage performance (SCHURTER), automotive-grade voltage ratings (Bel Fuse), compact form factor & automotive qual (SOC), pyro and safety integration (Daicel, Autoliv), and system-level switching/protection (Sensata’s GigaFuse/FaultBreak). ABB and Siemens play in the infrastructure and industrial protection layer where charging and stationary storage intersect with vehicle safety needs.

Market concentration and strategic implications: the market shows a moderate‑to‑high concentration profile, with the top three and top five suppliers accounting for a large portion of market share. This supports premium pricing for certified, high-reliability fuses and creates hurdles to scale for new entrants, while opening specialized niches (e.g., ultra‑compact main-circuit fuses, integrated fuse‑contactor systems) for focused innovators.

Sensata (Mar 2026) launched an integrated switching/protection product that blurs lines between passive fuses and electromechanical contactors; implication — OEMs will increasingly value system-level safety modules, not just discrete fuses.

SOC Corporation (Mar 2026) updated its AEC‑Q200-qualified lineup, signaling continued tightening of automotive qualification expectations and making time-to-market dependent on supplier qualification velocity.

SCHURTER (Aug 2025) and Eaton (Sep 2025) released HV-focused portfolios and global EV fuse portfolios respectively — moves that favor suppliers with both product specialization and global manufacturing footprints.

PEC (Jun 2024) updated catalogs to cover >750 VDC systems and pyro offerings, reinforcing that higher-voltage architectures are becoming mainstream rather than niche.

Procurement & sourcing: Implement layered hedges against copper volatility — e.g., index-linked contracts, strategic consignment stocks, and dual-sourcing with regional back-up. Negotiate qualification timelines and price‑escalation clauses explicitly tied to metal benchmarks.

Product & engineering: Prioritize system-level integration: fuse‑contactor hybrids and fuses with embedded diagnostic capability will command premium positioning. Invest in accelerated AEC‑Q200 and ISO/UL test paths to shorten vehicle release cycles.

Manufacturing footprint: Balance centralization (scale) with regional cell‑level supply (risk mitigation). Consider brownfield expansion near major EV clusters or partnerships with contract manufacturers to de‑risk capex.

M&A and partnerships: Target acquisitions or JVs that provide either category-leading pyro capabilities, semiconductor-protection expertise, or integrated safety modules. For OEMs, secure exclusivity or first‑source agreements with suppliers that offer system integration capabilities.

Commercial model: Move beyond per‑unit pricing to value-based contracts that monetize reduced warranty exposure, lower pack-level BOM cost through optimized fuse sizing, or faster time-to-market due to pre‑qualified platforms.

Regulatory & testing: Build internal competence in the evolving standards matrix and plan for front-loaded testing investments to avoid downstream launch delays. Early engagement with test houses and standards bodies can accelerate approvals.

Risk scenarios & KPIs: Track KPI dashboards aligned to copper spot & forward prices, supplier lead times, qualification pass rates, and fuse‑related warranty incidents. Run quarterly scenario reviews to update procurement and product roadmaps.

For leadership teams making 2026 commitments, the choice is binary: treat EV fuses as tactical commodities and accept rising cost and program risk, or elevate fuses into product, supply-chain and regulatory strategies that protect margins and shorten time-to-market. PW Consulting’s Worldwide EV Fuses Market report equips decision-makers with the data, scenario models and playbooks required to choose and execute the second path. To access the full dataset, supplier breakdowns, and downloadable commercial toolkits referenced in this summary, please consult the complete report available via PW Consulting’s publications portal.

For detailed analysis of this topic, please visit the official page:Worldwide EV Fuses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com