Cosmetic Emollient Market Size, Share, Trends, Forecast 2024–2034

Networking |

2026-05-18 06:32:55

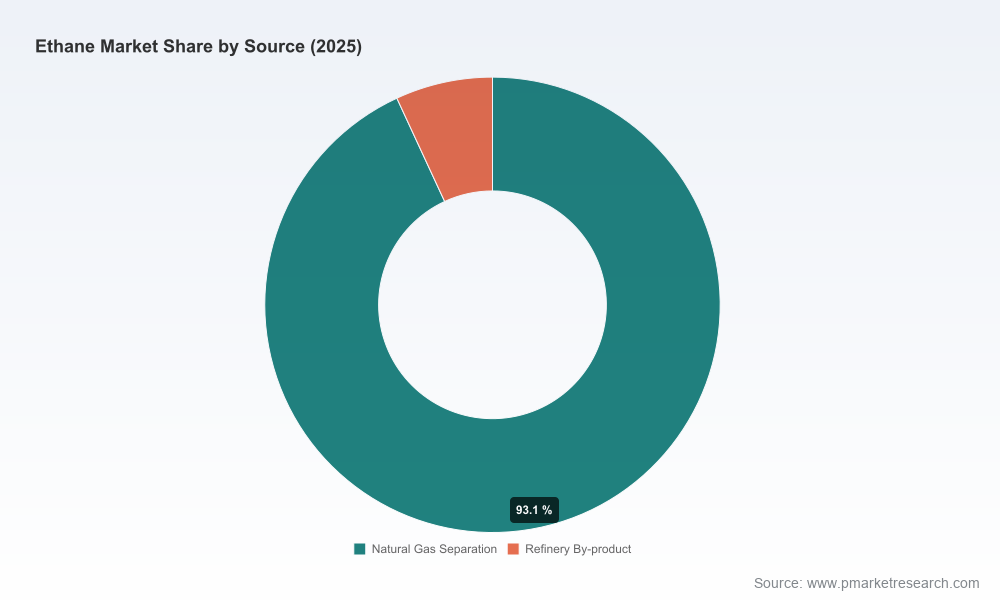

PW Consulting’s latest Worldwide Ethane Market report (base year 2025) arrives at a pivotal moment for petrochemical and midstream executives planning 2026 investments. The global ethane market has demonstrated sustained expansion over the past half‑decade and, on our baseline projections, is set to continue growing through the forecast window (2026–2032) at a compound annual growth rate (CAGR) of approximately 5.02%. From a market value of roughly USD 36.8 Billion in 2025, the sector is forecast to progress to the low‑fifties by 2032 under central assumptions. This briefing highlights the strategic value of the report for 2026 decision cycles — showing where to focus analysis, what levers move value, and how competitive dynamics will shape outcomes — while preserving the granular datasets and segment maps available in the full release.

Worldwide Ethane Market

Ethane’s role as a preferred cheap carbon feedstock for ethylene production has translated into structural demand growth across global petrochemical chains. Three interlocking drivers underpin our outlook for 2026:

Worldwide Ethane Market

These forces combine to produce a market that is growing steadily but also becoming more dynamic in flow patterns and pricing sensitivities. The PW Consulting report quantifies these dynamics in a scenario framework that links supply additions, terminal utilization and feedstock conversion to near‑term price and margin outcomes.

Worldwide Ethane Market

For corporate boards, C‑suite leaders and commercial teams preparing 2026 plans, the report’s central value is translating macro forecasts into actionable strategic options. The most consequential decisions fall into three buckets:

PW Consulting’s templates and sensitivity matrices permit rapid evaluation of these choices under multiple price and volume scenarios, enabling procurement, treasury and strategy teams to move from intuition to quantified trade‑offs within weeks.

Our stress testing for 2026 emphasizes several high‑impact risks accompanied by practical monitoring indicators:

Each risk is paired in the report with specific lead indicators and a recommended response ladder — from low‑cost commercial fixes to investment‑grade contingency plans — to help teams calibrate resource allocation within 2026 planning cycles.

The market is neither atomistic nor fully consolidated. Our concentration assessment shows that the top‑three commercial players account for roughly 38% of market activity, while the top‑five account for just over half. That structure creates both powerful incumbents and ample space for mid‑market players to execute differentiated strategies.

Key strategic archetypes we profile include:

The report contains concise, decision‑focused profiles for the major players — identifying their strategic posture, recent moves and likely next plays — so leadership teams can prioritize counterparties for JV, offtake or M&A dialogues. Recent industry developments include a wave of export infrastructure commissioning in 2025, planned cracker start‑ups in 2026, and a cluster of cracker feedstock conversions in key consuming markets; together these events materially reshape the 2026 supply‑demand frontier.

Beyond the narrative, the report is built as an operational toolkit for immediate use in 2026 planning:

These deliverables are intentionally modular: procurement teams, corporate strategy groups, and M&A desks can extract the components most relevant to their mandate and integrate them into existing planning cycles.

We recommend a pragmatic 90‑day playbook for senior teams preparing 2026 decisions:

Maintaining a tight governance loop with weekly cadence between commercial, operations and finance will ensure rapid course corrections should feedstock spreads or commissioning schedules change.

The 2026 planning horizon for ethane is defined by choices: whether to secure and lock feedstock, to anchor growth in export infrastructure, or to pursue flexible, service‑based approaches that preserve optionality. PW Consulting’s Worldwide Ethane Market report translates high‑level growth (CAGR ~5.02% across the forecast window) into executable decisions — including model‑driven risk assessments, actionable commercial playbooks and a clear view into how competitive moves will reconfigure margins.

For teams preparing final 2026 budgets, negotiating major offtake contracts, or evaluating midstream investments, the full report provides the granular regional and application splits, pricing curves, project‑level timelines and company‑level financials required to finalize commitments. Access to the interactive model and the complete data suite is available through our report portal, and PW Consulting stands ready to support scenario workshops and bespoke valuation slices to accelerate your 2026 decision cycle.

PW Consulting — strategic clarity for volatile feedstock markets. Visit our Worldwide Ethane Market report page for the complete dataset, segmentation maps, and the interactive forecast model.

For detailed analysis of this topic, please visit the official page:Worldwide Ethane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com