Micromachining Market Industry Trends Precision Manufacturing Demand and Growth Outlook

Networking |

2026-03-02 10:35:07

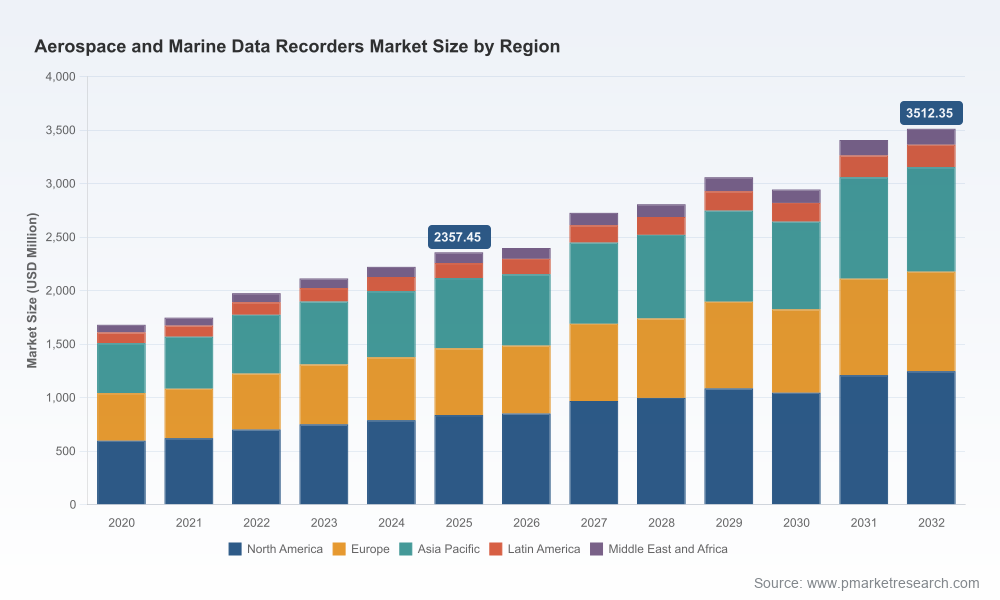

PW Consulting’s latest market study on Aerospace and Marine Data Recorders delivers a focused, decision-ready perspective for executives planning capital allocation, product roadmaps, and M&A activity in 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the report synthesizes regulatory drivers, supplier positioning, technology trajectories, and service-led monetization models. At the aggregate level, the market has shown steady expansion through 2025 and is projected to continue growing at a compound annual growth rate (CAGR) of approximately 5.85% across the forecast period — taking the market from its 2025 size into a materially larger and more complex ecosystem by 2032.

Aerospace and Marine Data Recorders Market

Regulatory deadlines are creating near-term demand windows. Recent mandates from civil aviation and maritime authorities — notably updated CVR duration requirements and IMO VDR performance obligations — have shortened procurement timetables and shifted spending to certified, crash‑survivable, solid‑state architectures.

Aerospace and Marine Data Recorders Market

Technology convergence is changing value capture. Connected recorders, remote data handling and analytics, and integrated flight/ship systems are turning what were once hardware-centric purchases into multi-year software, services, and data partnerships.

Aerospace and Marine Data Recorders Market

Market structure favors scale and certified incumbency. The sector exhibits moderate concentration among top suppliers, yielding differentiated advantages in certification, aftermarket reach, and platform OEM relationships — characteristics that will determine winners in retrofit waves and new platform fits.

Aggregate market sizing in our base analysis shows a clear recovery and acceleration through the mid-2020s, culminating in a 2025 market level that reflects both retrofit and OEM replacement cycles. The forecast path through 2032 — underpinned by the 5.85% CAGR scenario employed in the model — implies meaningful cumulative demand for recorder hardware, associated avionics/shipboard integration, aftermarket services, and recurring data-management revenues. For corporate planners, this trajectory supports multi-year investments in certification programs, digital platforms, and capacity expansion, but it also underscores the importance of timing: projects that achieve certification and distribution readiness in 2026–2027 will capture the densest portion of retrofit demand.

Regulatory changes are the proximate cause of the most immediate contract opportunities. Civil aviation regulators (FAA, EASA) have consolidated requirements for extended-duration cockpit voice recording and crash‑survivable solid‑state designs, while ICAO standards continue to shape minimum parameters for flight data recorders. In the maritime domain, IMO and SOLAS mandates paired with IEC standards maintain mandatory VDR fitment and drive replacement cycles for merchant and passenger vessels. Beyond the baseline compliance necessity, regulators are increasing emphasis on data integrity, secure remote access, and post-incident data availability — shifting procurement evaluation criteria to include software, certification pedigree, and cybersecurity postures in addition to hardware durability.

The industry map in 2025–2026 is characterized by a blend of long‑standing incumbents with deep certification portfolios and smaller, agile firms that specialize in a narrow slice of recorder capabilities or digital services. Our analysis highlights several archetypes:

Platform incumbents with broad OEM relationships and multi-decade heritage in crash‑survivable systems — these firms command trust in airline and shipowner procurement processes and carry certification economies of scale.

Specialist maritime and military suppliers that pair recorder hardware with vessel-performance systems or defense-grade resilience — these players monetize niche technical differentiation and long-term service contracts.

Newer entrants and software-led providers that augment legacy hardware with remote download tools, analytics suites and cybersecurity layers — these actors are rapidly transforming the aftermarket value chain.

Selected competitive profiles and recent industry moves illustrate these dynamics. Leading aerospace suppliers have launched or certified next‑generation connected recorders to meet extended CVR requirements and are moving into distribution partnerships with major OEMs and MRO networks. Maritime specialists continue to enhance VDR and S‑VDR offerings with ship performance monitoring. Licensing deals and collaborations to enable standardized data downloads and accelerated fleet upgrades are becoming more frequent, reflecting the industry's pivot from discrete hardware sales to platform and service contracts.

Connected, certified recorders: Expect certified, connected recorders that support secure remote retrieval and fleet‑level health monitoring to be table stakes for new procurement from 2026 onward. Strategies should combine hardware certification timelines with software security validation.

Data services and software monetization: There is a meaningful shift toward recurring-revenue models — predictive maintenance, data analytics, and compliance-as-a-service will be central to capturing post‑installation value.

Cybersecurity and provenance: With data integrity now a compliance and liability concern, integrating secure encryption, authenticated chain-of-custody, and tamper-evident logging into product roadmaps is necessary for both aerospace and marine solutions.

Cross-domain capabilities: Suppliers that can translate aerospace-grade crash survivability and certification expertise into maritime or defense contexts will expand addressable markets without proportionate incremental certification risk.

Aftermarket and MRO positioning: Service capability — remote diagnostics, fast turnarounds, standardized parts, and global spares networks — can yield higher lifetime customer value than initial hardware margins.

PW Consulting recommends that executive teams treat 2026 as an inflection year: regulatory compliance deadlines compress demand and create a window for strategic moves that will determine mid‑decade market share. Key recommended actions include:

Prioritize certification pipelines: Accelerate certifications for platform variants that align to impending regulatory timelines and OEM retrofit schedules. Time-to-market remains a primary determinant of retrofit win rates.

Build software and services capabilities rapidly: Acquire or partner to add remote download tools, analytics stacks and compliance reporting modules to convert hardware buyers into platform customers.

Strengthen OEM and MRO channels: Secure distribution partnerships and MRO agreements to ensure retrofit access; co‑sell arrangements can materially reduce customer acquisition costs for fleets subject to regulators’ mandates.

Consider targeted M&A: Use M&A to close capabilities gaps (e.g., cybersecurity, analytics, maritime-specialist recorders) where internal development would miss the 2026 demand window.

Optimize aftermarket economics: Rebalance commercial terms toward performance and service contracts that deliver predictable recurring revenues and higher customer retention.

The full report is structured to be directly actionable for corporate strategy and commercial teams. Highlights include:

Top-down market sizing and scenario-based forecasts through 2032, with sensitivity analyses around regulation timing, retrofit uptake rates, and platform replacement cycles.

Regulatory tracker and compliance calendar that maps mandates (aviation and maritime) to retrofit and OEM procurement windows.

Competitive benchmarking across product, certification, channel, and aftermarket metrics, including supplier scorecards and relative positioning versus certification and service coverage.

Technology roadmaps covering recorder hardware, data acquisition units, remote-download tooling and analytics stacks, along with cost-of-ownership comparisons.

Commercial playbooks: pricing strategy templates, go-to-market routes for OEM vs retrofit, and MRO integration checklists.

M&A shortlist and diligence templates for buyers: target capability maps, integration risks, and quick-reference valuation considerations.

Operational tools: 100‑day integration and certification acceleration plans, supplier ecosystem maps, and a risk register tailored to recorder projects (certification, cyber, supply chain).

The market shows measurable concentration among the largest suppliers, reflecting the premium placed on certification track records and OEM relationships. This concentration amplifies the value of strategic partnerships and licensing arrangements as levers for newer entrants or adjacent-industry players to scale quickly without duplicative certification costs. For incumbent firms, the competitive advantage derives less from raw manufacturing capacity and more from trusted certification histories, global aftermarket networks, and cross-platform product families that reduce integration friction for customers.

For OEMs and system integrators: fast-track a two-pronged investment — certify a compliant connected recorder variant while piloting a subscription-based analytics offering with select fleet customers.

For pure-play hardware suppliers: prioritize channel relationships with MROs and OEM distributors. Reframe sales conversations around fleet-level operational benefits and compliance assurance rather than unit price alone.

For investors and private equity: prioritize targets with recurring-service tails, strong certification pedigrees and modular software IP that can be cross-sold across aerospace and maritime segments.

The Aerospace and Marine Data Recorders market in 2026 will be shaped by a confluence of regulation-driven demand, software-enabled aftermarkets, and supplier consolidation. Companies that align certification timelines with digital service rollouts and distribution partnerships will capture disproportionate share of the compliance-driven retrofit wave. PW Consulting’s full report provides the granular, executable intelligence — from scenario models to M&A targets and 100‑day operational plans — that leadership teams need to translate the 2026 opportunity into concrete market outcomes.

For executives seeking the complete dataset, supplier scorecards, and actionable playbooks referenced in this brief, access to the full report and supporting tools is available on our website. PW Consulting’s advisory team is also available for bespoke strategy workshops to translate findings directly into your 2026 operating plan.

For detailed analysis of this topic, please visit the official page:Aerospace and Marine Data Recorders Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com