PW Consulting: Robotic Vacuum Market to hit USD 10,970M by 2032 at 12.45% CAGR

Health |

2026-07-12 05:36:38

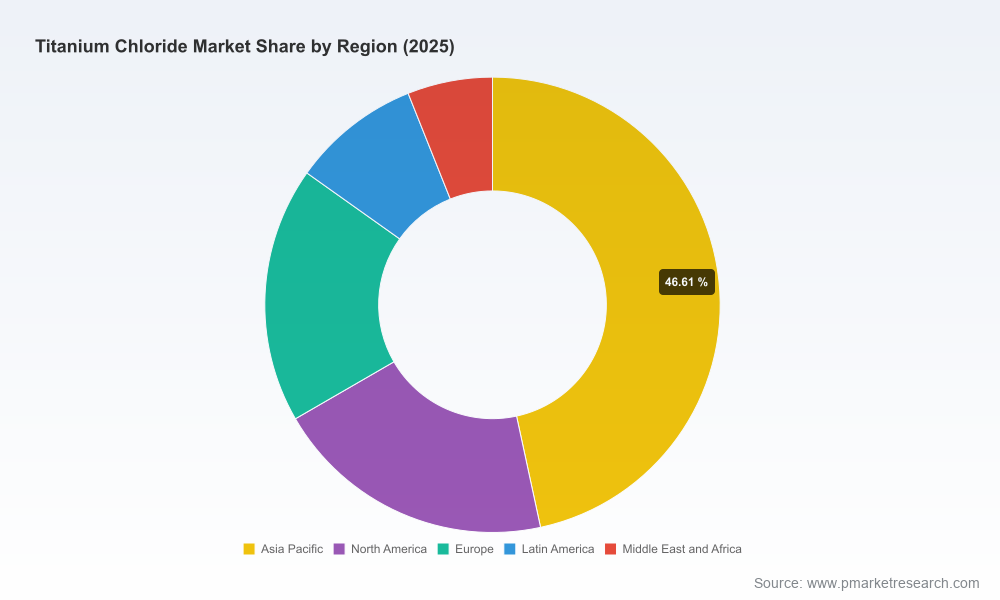

As corporates prepare capital allocation and procurement strategies for 2026, the titanium chloride (TiCl4) market is transitioning from recovery-driven dynamics into a phase of structural repositioning. PW Consulting’s new report — benchmarked on a 2025 base year and spanning a historical window (2020–2025) with forward-looking forecasts to 2032 — shows a stable mid-single-digit compound annual growth (4.8% CAGR) through the forecast horizon. That trajectory reflects a market expanding from a mid‑teens billion USD scale in the base year toward a low‑twenty billion USD global market by the end of the decade. Against this backdrop, the report provides the decision-grade intelligence that C-suite strategists, procurement chiefs, and transaction teams need to act in 2026.

Worldwide Titanium Chloride Market

Capital planning: modest but sustained growth and periodic supply volatility mean brownfield optimizations and selective brownfield expansions can deliver higher returns than large greenfield bets for many participants.

Worldwide Titanium Chloride Market

Procurement and pricing: even with steady demand growth, intermittent regional tightness and feedstock-driven cost swings create windows for strategic purchasing, long‑term offtake agreements, and indexed contracts that protect margins.

Worldwide Titanium Chloride Market

M&A and partnerships: market concentration metrics indicate that a relatively small group of global producers capture a meaningful share of merchant flows — creating premium opportunities for bolt‑on acquisitions and supply alliances that improve integration into TiO2 and titanium metals value chains.

Our model, calibrated with granular plant‑level outages, maintenance schedules, and observed pricing episodes, yields a 4.8% CAGR across 2026–2032. This pace of expansion is sufficient to support additional merchant capacity where economics are robust, but not so rapid as to eliminate the periodic price rallies caused by synchronized maintenance, energy spikes, or logistics disruptions. In plain terms: buyers should expect a generally stable market envelope punctuated by episodic tightness; sellers should prioritize reliability and feedstock flexibility as differentiators.

Feedstock and cost pressure: ilmenite and chlorine inputs remain the principal cost drivers. Recent market intelligence points to discernible upward pressure on feedstock procurement costs in certain sourcing corridors, which translates into elevated TiCl4 breakevens for non‑integrated producers.

Production intensity and technical ratios: plant‑level consumption metrics (for example, industry averages for TiCl4 input per tonne of titanium metal produced) underline how incremental shifts in upstream availability materially alter downstream economics for sponge and specialty metal producers.

Regulatory environment: increasingly frequent environmental inspections in key producing geographies and trade policy measures such as anti‑dumping duties have already reconfigured supply flows and will remain a material line item in corporate risk assessments.

Logistics and energy risk: the market’s recent episodes of regional tightening were amplified by maintenance and higher energy costs, illustrating how operations planning and energy sourcing strategies have outsized returns on reliability.

The sector exhibits a mix of integrated pigment producers, merchant specialists, and regional champions. Key corporate archetypes identified in our analysis include:

Large integrated pigment and chemicals groups that use TiCl4 as a core intermediate and thus prioritize feedstock flexibility and proprietary chloride‑process technology. These companies often hold strategic advantages in upstream sourcing and can absorb short‑term margin pressure.

Merchant specialists and chemical suppliers who differentiate on product specification, logistics capability, and service to niche high‑purity applications. Their appeal is strongest where consistency, certification, and containerized logistics matter.

Representative firms profiled in the full report include, among others, established international producers and regional leaders across North America, Europe, Japan and China. Each profile dissects asset footprints, integration logic, quality platforms and strategic intent — enabling acquirers and partners to map counterparty fit against corporate objectives.

Supply tightening episodes in late 2025 highlighted how scheduled maintenance, energy cost spikes, and logistics friction can trigger rapid price adjustments in certain routes. These events exposed the tactical advantage of diversified sourcing and flexible contract terms.

Operational resumption at a major chloride‑process facility following regulatory clearance illustrates how single‑asset changes can restore balance to constrained regional supply pools — and why monitoring local permitting and resource constraints is critical to near‑term planning.

Capacity additions by prominent producers signal continued strategic focus on chloride‑process growth, but the timing and commissioning of these projects create transient conditions where margins and merchant flows can diverge from long‑run forecasts.

For procurement: adopt a layered buying strategy combining short‑term tactical coverage with selective long‑dated offtakes; include explicit clauses for feedstock cost pass‑through and force‑majeure adjudication tuned to maintenance seasons.

For operations and supply chain: prioritize capacity reliability, chlorine sourcing contracts, and logistics resilience. Investments in modular purification and containerization can unlock premium markets with lower competition.

For corporate development: use a nucleus of supply‑chain telemetry to identify M&A targets that add capacity, improve feedstock access, or secure downstream offtake; small to mid‑sized bolt‑ons often deliver faster payback than greenfield plants in the current growth phase.

For risk & compliance: incorporate evolving regulatory inspections and trade measures into scenario tests; maintain flexible contingency plans for rapid pivoting of merchant supply across regions as policy and tariffs evolve.

We designed the report to be a turnkey decision support tool for 2026. Key deliverables include:

A calibrated baseline and three forward scenarios (Stabilized Growth, Episodic Tightness, and Accelerated Integration) with implications for pricing, margins and supply buffers.

Plant‑level breakeven models and an operations calendar that align scheduled outages with demand seasonality to identify probable tight windows.

Contract design templates — including indexed pricing clauses, quality specifications, and logistics SLAs — that reflect market realities and reduce negotiation friction.

Due‑diligence checklists and valuation heuristics for M&A and joint ventures, emphasizing feedstock security, permitting risk, and integration synergies.

Competitive profiles and scenario playbooks for buyers, sellers, and merchant traders to execute tactical and strategic moves with quantified upside and downside.

The most consequential sensitivities we model are: feedstock cost shocks, synchronized maintenance across key plants, abrupt regulatory enforcement in major producing jurisdictions, and sizeable tariff shifts affecting trade flows. Combined, these factors can compress or expand merchant availability faster than demand growth alone would suggest. Our scenario outputs quantify the directionality of each shock and offer concrete mitigants — from contract re‑routing and short‑term leasing of storage capacity to strategic inventory policies and targeted investments in purification.

0–90 days: operationalize monitoring dashboards for plant outages, feedstock tenders and freight availability; renegotiate critical short‑term contracts to add flex and liquidity.

90–180 days: conduct tactical sourcing campaigns, evaluate selective term offtakes tied to feedstock pass‑throughs, and execute logistics hedges for high‑risk corridors.

180–360 days: pursue bolt‑on M&A or strategic partnerships to shore up feedstock access or to enter higher‑margin, high‑purity segments; align capital plans with the scenario that best matches risk appetite and balance‑sheet capacity.

This brief surfaces the strategic contours and the high‑level quantitative framework that will matter in 2026, but it purposefully omits granular segment tables and route‑level allocations to preserve the context and commercial sensitivity of those outputs. PW Consulting’s full Worldwide Titanium Chloride Market report provides the complete datasets, plant‑level maps, pricing decks, and the downloadable model workbook needed to execute the recommended actions. For teams planning capital, procurement or M&A activity next year, those details are operationally indispensable.

Contact PW Consulting for an executive briefing, a customized scenario workshop, or immediate access to the full report and data model. Our analysts will walk you through extractable value‑creation opportunities specific to your role — procurement, operations, finance, or corporate development — and provide a tailored implementation roadmap for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Titanium Chloride Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com