High NA EUV Lithography Process Market Expands with Rising Demand for Sub-2nm Semiconductor Manufacturing

Drinks |

2026-06-20 09:53:50

PW Consulting’s new Worldwide Contraceptive Pills Market report (base year: 2025) translates seven years of historical market behaviour and a rigorous forecasting engine into an actionable playbook for boardrooms, commercial teams, and public-health procurement offices preparing decisions in 2026. The global market reached USD 22,217.7 Million in 2025 and, under our central scenario, is positioned to grow at a compound annual growth rate (CAGR) of 6.51% through the 2026–2032 forecast window — approaching USD 34,548.7 Million by 2032. That macro momentum masks a complex interaction of regulatory shifts, distribution innovation, and competitive repositioning that will determine winners and laggards over the next 18–36 months.

Worldwide Contraceptive Pills Market

Regulatory displacement is real. The first nonprescription daily oral contraceptive (Opill) moved into mass-market channels and became broadly available across the United States in 2024–2025, and the precedent it set materially changes go‑to‑market assumptions for branded and generic manufacturers alike. We also tracked the FDA approval of a dissolvable (orally disintegrating) combined pill (Femlyv), a formulation innovation that creates new access vectors for populations with swallowing difficulties and provides payers with a differentiated product-value argument.

Worldwide Contraceptive Pills Market

Reimbursement and payer behavior remain uneven. While many insured women retain cost‑free access to prescription products in major markets, the absence of cohesive federal guidance for OTC contraceptives in some jurisdictions creates complex commercial calculus for manufacturers and retailers in 2026.

Worldwide Contraceptive Pills Market

Competitive concentration and consolidation are accelerating. The market shows relatively high concentration at the top: our analysis places the combined revenue share of the three largest firms at roughly 62.45% and the top five at about 78.12%. These dynamics produce strategic leverage for incumbents but also highlight attractive windows for nimble generics and novel entrants to capture niche value.

Demand-side elasticity and public procurement pressures — particularly in low- and middle-income settings — continue to be a critical lever. In many public-procurement contexts the cost of pills represents a material share of program spending, which amplifies sensitivity to unit-price changes and supplier reliability.

Our competitive framework groups players by strategic role rather than attempting a rules-based league table in this preview. Key archetypes and representative firms include:

Global innovators and incumbents (e.g., Bayer AG, Pfizer, Merck, Johnson & Johnson/Janssen, AbbVie): these firms retain strong branded franchises, channel relationships, and regulatory experience. Their strategic choices on pricing, OTC conversion, and lifecycle management will shape premium segments and payer negotiations.

Women's health specialists (e.g., Organon & Co.): focused portfolios and targeted channel strategies—especially around patient-centric formulations—create differentiated routes to market for new formulations or niche indications.

Generic leaders and scale manufacturers (e.g., Teva, Aurobindo, Lupin, Sun Pharma, Cipla, Zydus, Amneal): cost and supply reliability define their competitive advantage. Generics scale will be the primary mechanism constraining prices in mature markets and enabling access in emerging markets.

Public-sector and mission-oriented suppliers (e.g., HLL Lifecare): critical partners for country-level programs and tenders, especially in markets where government procurement shapes demand.

New OTC entrants and consumer-focused players (e.g., Perrigo with Opill): these firms demonstrate the commercial possibilities of direct-to-consumer and retail-bound contraception — influencing distribution, pricing, and marketing models across the board.

Recent industry events underscore these dynamics: the broad retail rollout of Opill following regulatory approval, the clinical and regulatory novelty of an orally disintegrating combined pill, and emerging evidence suggesting higher utilization where OTC availability expands access. Collectively, these developments change short‑term demand curves and reframe market-entry economics for 2026 launches.

Re-assess OTC strategy with a multi-track plan. For established brands, OTC conversion offers a growth and defensive pathway, but it requires new pricing models, retailer contract terms, over-the-counter merchandising investments, and a revised pharmacovigilance approach. For generics, OTC availability creates broader volume opportunities but also intensifies margin pressure.

Differentiate through formulation and packaging innovation. Orally disintegrating tablets and patient-centric packaging materially change adoption among specific user groups and can command premium positioning with payers that value adherence gains.

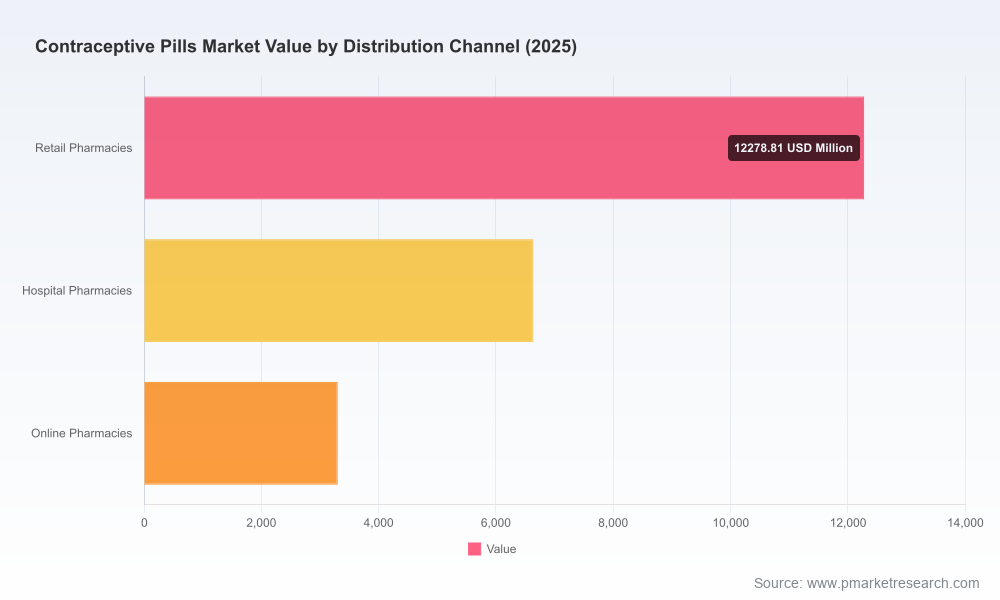

Shift channel strategies to reflect hybrid demand. Online pharmacies and retail channels have accelerated share, while hospital and clinic channels remain important for provider‑initiated models. Optimizing omnichannel distribution and tailoring promotional tactics per channel will be decisive.

Lock down supply resilience and cost transparency. Raw-material and API supply issues remain a source of execution risk. Scenario-based procurement planning, secondary-source qualification, and near-shore manufacturing options must be part of the 2026 capital and operational plans.

Use real-world evidence to influence payers and policy. Demonstrating adherence, safety, and economic benefits from OTC availability or new formulations will accelerate favorable reimbursement and formulary decisions — especially where state-level policies or private payers set coverage rules for nonprescription products.

Consider targeted M&A and partnership plays. Given the market’s concentration, strategic acquisitions—particularly of capabilities in OTC commercialization, digital-first brands, or formulation technologies—deliver fast access to scale and differentiated assets.

Our report is deliberately structured to move leaders from insight to execution. Highlights include:

Probabilistic market model and three scenario forecasts (conservative, central, upside) with monthly and annual outputs through 2032, stress‑tested for regulatory and pricing shocks.

Regulatory pathway maps and timing templates for OTC conversions, combination-product approvals, and novel formulation filings across major jurisdictions.

Commercial playbooks for OTC launch, retail roll‑out, and online-first strategies — including merchandising tactics, reimbursement engagement scripts, and retailer contracting templates.

Payer-impact modelling and pricing‑elasticity matrices to quantify revenue and margin trade-offs across different coverage scenarios.

Competitor heatmaps, capability-gap analyses, and an M&A opportunity index focused on formulation technologies, digital engagement assets, and manufacturing capacity.

Supplier risk matrix and mitigation playbook, incorporating raw-material concentration analysis and contingency sourcing pathways.

Country-level launch scenarios and public-procurement tender playbooks for priority emerging markets.

In keeping with our “trailer” approach, we present these deliverables and their strategic implications here but intentionally withhold the granular regional and product-type tables that underpin our modelling. Those detailed segment and channel data, including downloadable spreadsheets and sensitivity models, are accessible in the full report package on our website.

Executives: Prioritize an OTC-readiness program, revise P&L assumptions for OTC cannibalization vs. incremental reach, and accelerate digital and retail partnerships for consumer engagement.

Commercial teams: Re-tool promotional mix to support self-care narratives, refine pricing ladders for over‑the‑counter vs. prescription lines, and deepen data partnerships to measure real-world uptake.

Supply-chain leaders: Implement dual‑source API strategies, increase buffer inventories for critical intermediates, and evaluate manufacturing footprint shifts to manage volatility.

Investors and M&A teams: Look for targets with OTC commercialization proof points, differentiated formulation IP, or cost advantages in high-growth geographies.

Public-health procurement planners: Reassess tender design to account for evolving OTC availability and to ensure continuity of access in public programs.

If your leadership team will be allocating resources, approving launches, or sizing M&A targets in 2026, the PW Consulting report functions as both a diagnostic and an execution guide. Begin with the scenario outputs to stress‑test your base case, use the regulatory timelines to prioritize dossier submissions or OTC filings, and adopt the supplier-risk playbook to harden your supply chain ahead of any demand surge. For boards, the concentration metrics and the OTC precedent should prompt explicit discussions on defensive strategies and portfolio rebalancing.

To access the full dataset, granular market tables by region, type, and channel, and the complete suite of operational templates, download the full Worldwide Contraceptive Pills Market report on our website. The detailed tables and model templates included in the full report will allow your team to run customized scenarios and produce board-ready financials within days.

For detailed analysis of this topic, please visit the official page:Worldwide Contraceptive Pills Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com