Worldwide Glass Cockpit Displays for Aerospace: Strategic Intelligence Briefing — PW Consulting

Why this report matters for 2026 decisions

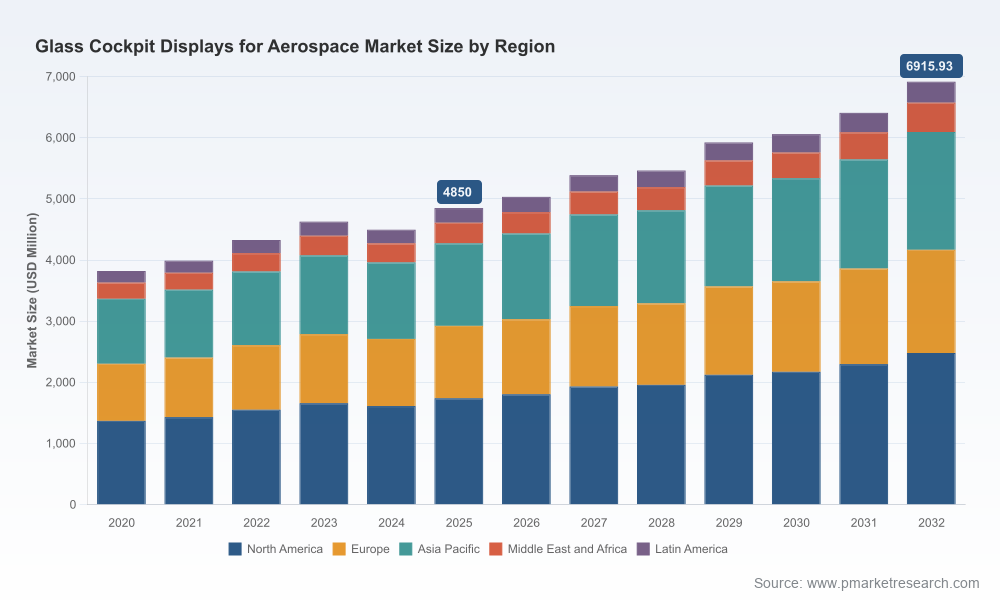

As aerospace programs enter a new cadence of fleet renewals, retrofit waves and defence modernization, cockpit displays are again at the center of OEM, Tier‑1 and systems integrator investment decisions. Our new market study, covering historical performance through 2025 and forward through 2032, synthesizes financial trajectories, competitive positioning and operational constraints that will determine winners and losers in the coming planning cycle. The global glass cockpit displays market is not only expanding — it is evolving in structure and risk profile. The market grew from the early 2020s into a multi‑billion dollar opportunity, and PW Consulting’s modelling shows a continued upward trajectory through 2032 at a compound annual growth rate (CAGR) of 5.19%.

Worldwide Glass Cockpit Displays for Aerospace Market

High‑level trajectory (what the numbers tell you)

Three datapoints are sufficient to orient executive strategy: steady recovery after pandemic disruptions, a re‑acceleration tied to retrofit and new‑build programs by the mid‑2020s, and durable demand through the early 2030s due to platform service lifecycles and avionics upgrades. In our base‑case model the global market reaches a meaningful plateau in the mid‑2020s and expands steadily to 2032, reflecting both ongoing digitalization of flight decks and a multiyear retrofit tail as legacy fleets modernize. Market concentration is material — the top three suppliers capture a majority share, and the top five consolidate over seventy percent of market revenue — a fact that shapes pricing power, supplier selection and M&A strategies.

Worldwide Glass Cockpit Displays for Aerospace Market

What this means for 2026 corporate strategy

- For OEMs and Tier‑1s: Prioritize platform modularity and display commonality. With lead times for critical components still volatile, architectures that allow multiple qualified panel suppliers reduce program risk and protect EIS (Entry‑Into‑Service) schedules. Our scenarios show that modular HMI (human‑machine interface) designs materially lower program schedule risk without sacrificing certification flexibility.

- For suppliers and component manufacturers: Secure long‑lead semiconductor and driver‑chip supply through strategic contracts, dual‑sourcing and localized buffer inventories. Semiconductor availability dragged display panel deliveries by an average of 6–9 months in the 2023–2025 window; that exposure should be a top procurement KPI in 2026.

- For MROs and retrofit specialists: Build differentiated retrofit packages combining cost‑to‑install optimizations with lifecycle software support. The retrofit market remains a reliable revenue stream as operators seek to extend platform utility without full airframe replacement.

- For investors and corporate development teams: Target upstream content providers — rugged display glass, specialized driver ICs and DAL‑A certified modules — and consider bolt‑on acquisitions that deepen supply resilience and certification expertise.

Operational levers that reduce program risk

Our report identifies four operational levers that materially alter program outcomes:

Worldwide Glass Cockpit Displays for Aerospace Market

- Certification depth and DAL capability: Embedded processing and DAL‑A capable display modules shorten qualification cycles for military and special mission integrators. Suppliers with proven DAL pathways command premium pricing and lower customer switching costs.

- Design for sustainment: Displays designed for easy software updates and modular hardware replacement reduce lifecycle costs and increase aftermarket revenues. Sourcing choices that optimize spare‑parts commonality across fleet variants pay back over the mid‑lifecycle horizon.

- Localized subassembly footprints: Tariff policy shifts in 2025 created friction for global avionics flows. Firms that preemptively localized critical subassembly lines near major assembly hubs mitigated lead‑time volatility and improved delivery certainty.

- Supply‑chain orchestration: Active control of driver chips, PCBs and structural components — together these subsystems represent the majority of component cost for modern displays — is a decisive procurement advantage.

Competitive landscape: who matters and how they play

The market is led by a mix of established avionics integrators, diversified aerospace conglomerates and niche rugged display specialists. Understanding their strategic vectors is essential for partnership, procurement and M&A decisions.

- Collins Aerospace (RTX) — Strengths: deep avionics systems integration, large‑format LCD retrofit programs, and broad platform reach across commercial and military markets. Strategic posture: premium systems integrator that leverages retrofit programs (e.g., large transport platforms) to sustain revenue and cross‑sell avionics suites.

- Honeywell Aerospace — Strengths: avionics upgrade programs across business aviation and rotorcraft, and a strong installed‑base service footprint. Strategic posture: lifecycle services and upgrade monetization, with a focus on visibility, situational awareness and operator productivity features.

- Thales Group — Strengths: tactile large display systems with customizable HMI for both fixed and rotary wing; established OEM partnerships. Strategic posture: differentiation via HMI innovation and integration into broader mission systems, particularly for Airbus and key rotorcraft programs.

- Garmin Ltd. — Strengths: dominant position in GA and Part‑23 retrofit and forward‑fit segments with highly integrated glass flight decks and touchscreen solutions. Strategic posture: cost‑effective certified platforms and expanding footprint into advanced air mobility and select defense programs.

- Aspen Avionics — Strengths: focused, affordable certified glass solutions for general aviation. Strategic posture: defend GA price bands with certification cost efficiency and aftermarket service bundles.

- Specialists (ScioTeq, Astronautics, Elbit, Mercury Systems) — Strengths: rugged DAL‑capable displays, embedded processing, and defense program expertise. Strategic posture: capture mission‑critical pockets through niche certifications, rapid prototyping and European defence partnerships.

Recent competitive developments in early 2026 underscore shifting battlegrounds. Notable activity includes ScioTeq’s selection for air‑to‑air refuelling visualization systems and a letter of intent with a European defence prime on resilient avionics initiatives; these moves highlight demand for regionally resilient, certified visualization stacks. Emerging entrants and modular glass cockpit suppliers are targeting the Part‑23 and Part‑27 segments with rapid certification pathways, widening the supplier set for smaller platforms and advanced air mobility builds.

Supply chain, pricing and cost dynamics

Cost structure and supply availability are as consequential as top‑line demand. Industry data show that the display module itself comprises a meaningful single‑item share of total unit cost (roughly one third), with driver chips, PCBs and structural components collectively representing a large portion of the remainder. Raw material and component pricing volatility therefore transmits directly to both OEM margins and retrofit pricing. In 2025 the industry shipped approximately 309,000 cockpit display units at an average price in the low‑five‑figure range per unit — indicators that unit volumes remain substantial even as average selling prices are under upward pressure.

Semiconductor shortages in the early‑to‑mid 2020s imposed average program delays measured in months; by 2026, leading firms have implemented dual‑sourcing and strategic buffer strategies. Tariff measures introduced in 2025 accelerated localization trends — a structural change that procurement teams must factor into 2026 contracts and total landed cost models.

Scenarios and actionable playbooks for 2026

PW Consulting’s report presents three actionable scenarios (Base, Upside, Supply‑Constrained) that map to procurement, engineering and commercial actions. Key playbook items include:

- Base case (most likely): Focus on modular HMI roadmaps, embed certification path dependencies into program schedules, and secure second‑source agreements for driver ICs.

- Upside case (accelerated retrofit wave): Scale aftermarket operations, invest in calibration/installation tooling, and expand spare distribution networks while pursuing platform OEM partnerships for widebody retrofit tenders.

- Supply‑constrained case: Prioritize legacy stock deployment, lock multi‑year agreements with panel fabs, and accelerate qualification of regional subassembly suppliers to avoid program interruptions.

What the report contains (practical, decision‑grade deliverables)

PW Consulting’s market study delivers a blend of quantitative and qualitative deliverables tailored for C‑suite and program leaders:

- Multi‑scenario market sizing through 2032 with sensitivity to material cost inflation and certification timelines.

- Competitive heatmaps and capability matrices for Tier‑1s, niche display makers and new entrants, including DAL capabilities and aftermarket footprints.

- Supply chain vulnerability analysis with recommended mitigation contracts, inventory buffers and localization thresholds tied to program KPIs.

- Commercial playbooks for OEMs, integrators and MROs covering pricing, bundling and retrofit productization strategies.

- Regulatory and geopolitical impact assessment focused on tariff regimes, export controls and the implications for supplier selection.

Next steps for leaders planning 2026 moves

- Embed the PW Consulting market scenarios into your FY26 planning cycle to stress‑test procurement, product and M&A assumptions.

- Use the supplier capability matrices to identify strategic partners (or acquisition targets) that close DAL, processing and regional production gaps.

- Prioritize investments in software updatability and lifecycle support; these choices convert one‑time hardware projects into multi‑year service streams.

Closing — an invitation

This briefing outlines the strategic contours executives must weigh as they set budgets and programs for 2026. It intentionally highlights the major market drivers, risk vectors and competitive dynamics while preserving the granular segment and regional tables that are part of the full analysis. For executives requiring decision‑grade detail — including segment‑level forecasts, supplier scorecards, and program‑level financials — the complete Worldwide Glass Cockpit Displays for Aerospace Market report contains the full datasets and scenario inputs that informed this briefing. Visit our report page to access the comprehensive data and tools your team needs to convert insight into action.

For detailed analysis of this topic, please visit the official page:Worldwide Glass Cockpit Displays for Aerospace Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com