Bird Repellent Market Growth Accelerates Through Smart Wildlife Control Solutions

Other |

2026-07-09 10:01:55

As global industries accelerate lightweighting, electrification, and performance-driven design, the market for composite preforms is entering a phase of sustained, commercially meaningful growth. Our new PW Consulting report — benchmarked to a 2025 base year and projecting through 2032 — quantifies that trajectory: the market expanded from roughly USD 3.02 billion in 2020 to about USD 4.25 billion in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 7.1% across the 2026–2032 horizon. Under our central forecast, the market moves into the mid-single-digit billions in 2026 and approaches the high single-digit billions by the end of the forecast window.

Worldwide Composite Preform Market

For C-suite executives, plant managers, procurement heads, and private equity sponsors evaluating capital allocation in 2026, these topline dynamics are only the beginning. The substantive strategic value lies in understanding how that growth will be distributed across technologies, supply chains, regulatory regimes, and end-markets — and in translating that understanding into defensible, time-sensitive decisions. This press release provides a high-level précis of the PW Consulting findings, outlines the strategic implications for 2026 decision-makers, and highlights why the full report is a necessary read for stakeholders who need to convert market momentum into margin and market share.

Worldwide Composite Preform Market

Post-pandemic recovery and new platform ramps (aerospace, high-performance EVs, and utility-scale wind) are synchronized with supply-side capacity shifts. The result is increased unit demand for differentiated preforms and heightened pressure on lead times and raw-material sourcing.

Worldwide Composite Preform Market

Raw-material cost and regulatory inputs are changing the economics of preform production. Notably, carbon fiber pricing in Germany reached ~USD 33.8/kg in late 2025 with a Q1 2026 outlook at ~USD 34/kg, while epoxy resin indices show regional variance (global index ~USD 3.6/kg in April 2026, with higher levels reported in North America and Europe). These inputs directly compress margins for commodity preforms and create premium opportunities for design efficiency and integrated supply propositions.

Policy and trade actions — including increased US tariffs on certain composite imports in 2025 — are driving near-term reshoring, vendor qualification programs, and supplier diversification strategies. Firms that move early to secure capacity and to redesign supply agreements will gain a pronounced competitive advantage in 2026.

Our intent was to create a practitioner-grade instrument for 2026 planning cycles. The report combines proprietary market models, qualitative competitive intelligence, and transaction-grade operational playbooks. Key deliverables include:

A dynamic market model (2020–2032) with scenario toggles for raw-material price paths, regulatory cost impacts, and end-market demand shocks. This model is shipped with an Excel workbook for in-house sensitivity analysis.

Supply-chain and capacity maps, identifying bottlenecks and near-term capacity additions by technology class and manufacturing process (braiding, 3D weaving, NCF, automated preform layup). The maps are paired with practical mitigations — e.g., co-investment frameworks, tolling arrangements, and onshore expansion templates.

Vendor scorecards and procurement negotiation playbooks covering manufacturing footprint, technology competency, quality systems, and commercial terms — designed to shorten vendor selection cycles and reduce integration risk.

Go-to-market and product roadmaps for OEMs and Tier 1 suppliers that balance cost, cycle-time, and certification timelines. Includes case-based recommendations for integrating hybrid preforms and moving from prototype to high-rate production.

M&A and partnership playbooks for strategic and financial buyers: target sizing, valuation sensitivities under different demand scenarios, and integration checklists focused on intellectual property, processes, and talent retention.

Regulatory impact assessments and emissions/cost modeling to help manufacturers and downstream users plan capex and compliance strategies across major jurisdictions.

To preserve the strategic integrity of client decisioning, this press release intentionally omits granular segmentation tables and specific regional or application dollar-breakouts; those detailed figures and the full proprietary dataset are available in the complete report and accompanying model.

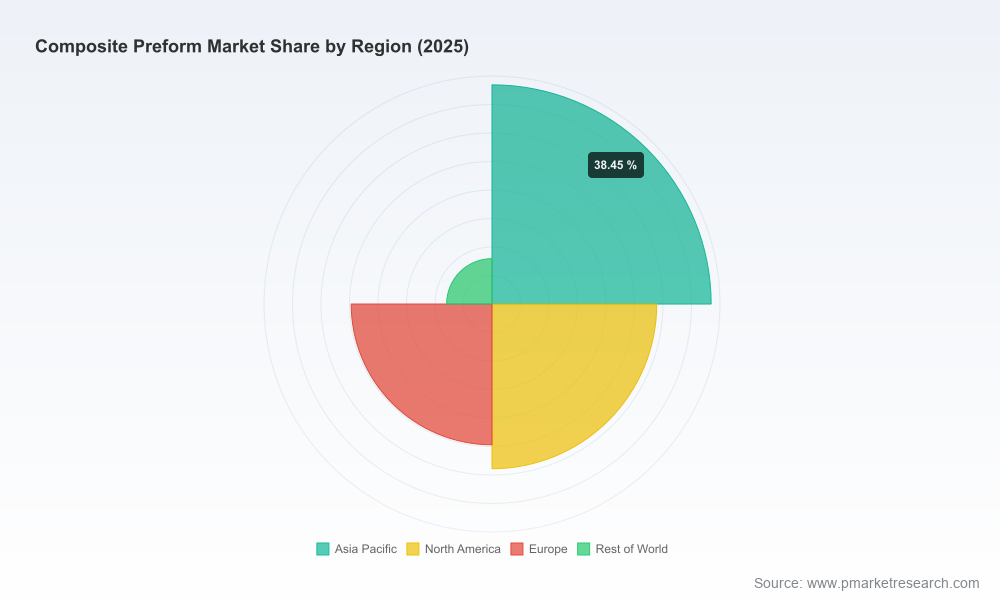

The market exhibits a moderate degree of concentration (CR3 ~38.5%, CR5 ~52.1%), indicating strong incumbent positions but also clear runway for challengers with technology differentiation, scale economics, or integrated service offerings. The competitive field is a mix of textile specialists, carbon-fiber champions, and systems integrators — each pursuing distinct routes to capture preform value.

A&P Technology Inc. (Cincinnati) remains a leader in high-rate braided solutions and complex net-shape preforms, with strong relevance in aerospace structural applications. Its high-throughput capability and breadth of sleevings/braided fabric products make it a go-to for manufacturers seeking certification-ready preforms at scale.

Albany Engineered Composites (AEC) focuses on 3D weaving and integrated molding solutions targeted at aerospace engine systems and critical structural fittings. Their depth in 3D textile engineering and systems-level certification experience positions them well for OEM programs where part count reduction and co-cured assemblies are strategic priorities.

Bally Ribbon Mills has reinforced its niche in 3D woven joints and high-temperature thermal protection systems. Their orientation toward extreme-environment applications makes them a preferred supplier for defense and TPS applications, and their trade-show activity signals continued investment in woven structural complexity.

Hexcel’s recent product introductions — including woven net-shape textiles and a rapid-cure prepreg system unveiled at JEC World 2026 — demonstrate an integrated-materials play that compresses cycle times and simplifies downstream processing. These product moves can materially affect cost-per-part and lay the groundwork for broader OEM adoption.

European textile specialists (e.g., Kümpers Composites, Sigmatex) and material giants (Toray, SGL Carbon) are closing the loop between fiber technology and preform architecture. Their comparative advantage lies in raw-material control, fiber engineering, and advanced textile processes that enable weight and performance optimizations for high-value programs.

Compsys and other solution-focused firms continue to commercialize novel preform geometries aimed at transportation stringers and beams — a reflection that performance-led design improvements offer a route to premium pricing even as material costs rise.

Recent trade-show and product launches (e.g., Hexcel at JEC World 2026; SAERTEX’s sustainability-focused Planet Composite initiatives; Bally Ribbon Mills highlighting 3D woven TPS at CAMX 2025) underscore two parallel trends: incumbents are broadening product portfolios to reduce total part cost, and textile specialists are elevating sustainability and manufacturability as differentiators.

Raw-material volatility and regulatory costs are the dominant margin levers in 2026. With carbon fiber and resin prices elevated and regional disparities pronounced, manufacturers and OEMs must deploy layered risk management:

Procurement: greater use of long-term offtake agreements, indexed pricing mechanisms, and regional sourcing contracts to lock supply and dampen spot exposure.

Design: material-efficiency programs (design-for-manufacture and design-to-cost), substitution where feasible, and adoption of hybrid preform architectures to balance performance and cost.

Operations: co-investment in regional capacity to avoid tariff shocks and to accelerate qualification cycles for local OEMs; selective vertical integration for critical feedstocks where margin capture justifies capex.

Innovation: accelerated adoption of rapid-cure chemistries, automated layup systems, and near-net-shape textile technologies that lower labor content and cycle time.

Raw-material price inflection — any sustained movement above our baseline price-path materially changes competitive advantage toward vertically integrated suppliers.

Large aerospace platform decisions — new fuselage or wing structure selections by OEMs will drive multi-year preform demand cycles and qualifier lists.

Automotive architecture shifts — mass-market EV program launches that commit to composite-intensive structures can reallocate volume and favor high-rate preform producers.

Regulatory and trade developments — changes in emissions regulation or tariffs will prompt rapid supplier requalification and capacity redeployment.

Technological breakthroughs and product rollouts — rapid-cure prepregs, HexShape-style net-shape textiles, and new 3D woven assemblies that reduce secondary operations will accelerate adoption if they demonstrate repeatable cost and cycle-time benefits.

For teams preparing 2026 budgets, sourcing strategies, or M&A pipelines, the PW Consulting Worldwide Composite Preform Market report is designed to be an executable input. The full report includes the granular segmentation, regional and application-specific demand analysis, supplier scorecards, and the downloadable financial model that we intentionally withheld from this summary to preserve the commercial value of the dataset.

Contact PW Consulting to access the full report, request a walk-through of the forecast model, or commission a tailored advisory engagement — including scenario workshops, supplier due diligence, and integration planning. In a market marked by steady growth but asymmetric risk, the right intelligence in 2026 will determine who converts demand into durable share and who competes on cost alone.

For detailed analysis of this topic, please visit the official page:Worldwide Composite Preform Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com