Early Detection Technologies Are Redefining the Prostate Cancer Diagnostics Market

Networking |

2026-06-17 12:26:35

PW Consulting’s new report on the Worldwide Potassium Carbonate Hydrate market delivers an actionable strategic framework for 2026 decision-making. The market has expanded from roughly USD 382.5 Million in 2020 to USD 479.8 Million in our 2025 base year, and our forecast indicates growth to about USD 648.5 Million by 2032. The compound annual growth rate for the forecast window is 4.4%. These macro trajectories reflect a market that is stable, specialty-driven, and increasingly sensitive to upstream feedstock and regulatory shifts — conditions that will shape commercial, operational, and M&A choices in 2026.

Worldwide Potassium Carbonate Hydrate Market

Several structural changes converge as companies plan for 2026 execution cycles. First, a new tax treatment effective January 1, 2026 introduces a Superfund-related cost vector for producers whose predominant processes generate taxable chemical substances by weight. Second, feedstock and energy cost volatility is already transmitting into regional price differentials; our market monitoring recorded material price gaps in late 2025 across East Asia and Europe. Third, regulatory review processes — notably the USDA National Organic Program sunset deliberations into 2027 — create demand risk for certain agricultural uses of potassium carbonate. Taken together, these developments convert what has been a largely supply-driven market into one where regulatory foresight, contract design, and strategic positioning will materially affect 2026 outcomes.

Worldwide Potassium Carbonate Hydrate Market

Understanding the chemistry matters for strategy. Potassium carbonate is most commonly produced via carbonation of potassium hydroxide (KOH), a flow that typically forms a hydrated intermediate (K2CO3·1.5H2O) that may be subsequently dehydrated to anhydrous product. This upstream linkage means KOH and potash markets — and the energy required for dehydration — are key cost drivers. Energy intensity of carbonation and drying steps creates sensitivity to regional gas and electricity prices, which in turn drives regional price dispersion and influences where new capacity economics are viable.

Worldwide Potassium Carbonate Hydrate Market

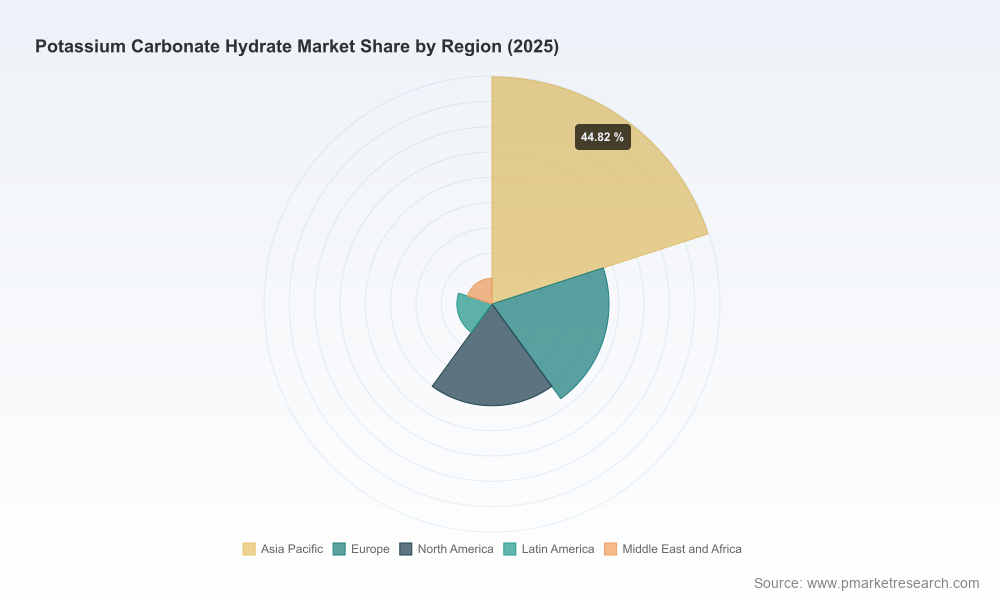

Price benchmarks observed in December 2025 exemplify this sensitivity: Northeast Asian prices tracked noticeably lower than European equivalents, reflecting differential feedstock availability and energy regimes. Those spreads underpin arbitrage opportunities, export flows, and localized capacity expansion decisions.

On the demand side, growth is being pulled by specialty, high-purity applications (pharmaceuticals, certain glass and electronics uses), while traditional bulk uses (agrochemicals, industrial processing) retain steady baseline demand. The market’s supply structure is moderately concentrated: top-tier firms capture a substantial share of global capacity, creating oligopolistic dynamics in certain product grades and forms.

Armand Products Company (USA) — As a global leader with ISO 9001:2015-certified facilities and large-scale capacity for both anhydrous and hydrated grades, Armand is positioned to defend volume markets while selectively targeting premium segments. Their global shipping footprint supports contract supply to multinational downstreams, but exposure to Superfund taxation and energy inputs requires recalibration of long-term pricing models.

Vynova Group (Europe) — Vynova’s strength is breadth of form factors and European market integration, making it a preferred supplier for food and pharmaceutical processors in the region. For 2026, Vynova’s strategic choices will revolve around margin protection via product differentiation and targeted service offerings.

INEOS KOH — Vertical integration is INEOS’s structural advantage. Producing liquid potassium carbonate from internally sourced KOH enables margin and supply-chain control for liquid-grade applications, especially in high-value specialty niches. This model will be instructive for competitors assessing backward integration or long-term feedstock contracts.

Hawkins, Inc. — A differentiated position in high-purity 47% liquid products and a focused end-market reach (electronics, boards, food preservation, oil & gas) gives Hawkins strategic optionality. Their playbook emphasizes technical service and application support — a useful blueprint for suppliers seeking to escape low-margin commoditization.

Asian manufacturers (UNID, Zhejiang Dayang, Wentong Potassium Salt Group, etc.) — Several large Asian producers combine scale with export orientation and ongoing capacity expansion, particularly for high-purity grades targeting electronics and specialty industrials. These firms will continue to shape global availability and pricing, and are core candidates for off-take and joint ventures.

Specialty chemical players (Evonik, AGC, Altair Chimica) — These firms compete on high-spec purity, technical certifications and tailored supply chains. Their strategic advantage lies in co-development with downstream OEMs and access to regulated markets.

Strategic implication: competition is less about sheer volume and more about product form, grade, proximity to feedstock, and regulatory compliance. The market concentration metrics reflect a landscape in which top participants set price references; mid-market players must choose between niche specialization or consolidation strategies to protect margins.

Beyond providing forecasts and benchmarks, our report includes executable templates — supplier scorecards, contract language playbooks, capital expenditure build-vs-buy calculators, and a regulatory impact module tailored to the Superfund tax and organic review scenarios. These tools are designed for rapid adaptation into procurement, finance and corporate strategy workflows so that leaders can convert insight into 2026 action plans within weeks, not months.

Potassium carbonate hydrate is no longer a simple commodity; it sits at the intersection of feedstock markets, energy dynamics, and evolving regulatory design. Our analysis shows a market growing at a steady mid-single-digit CAGR with varied upside by product grade and region. For companies planning 2026 budgets, the immediate priorities are stress-testing contracts for tax and feedstock shocks, upgrading pricing governance, and defining where to compete along the value chain.

To access full segmentation, proprietary regional and application breakouts, the supplier benchmarking dataset, and the interactive scenario model, please visit the report landing page for Worldwide Potassium Carbonate Hydrate Market (full datasets and Excel workbooks available). PW Consulting stands ready to convert these insights into a customized implementation roadmap for your business.

For detailed analysis of this topic, please visit the official page:Worldwide Potassium Carbonate Hydrate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com