Depyrogenated Sterile Empty Vials Market Emerging Pharma Trends

Other |

2026-06-30 11:37:54

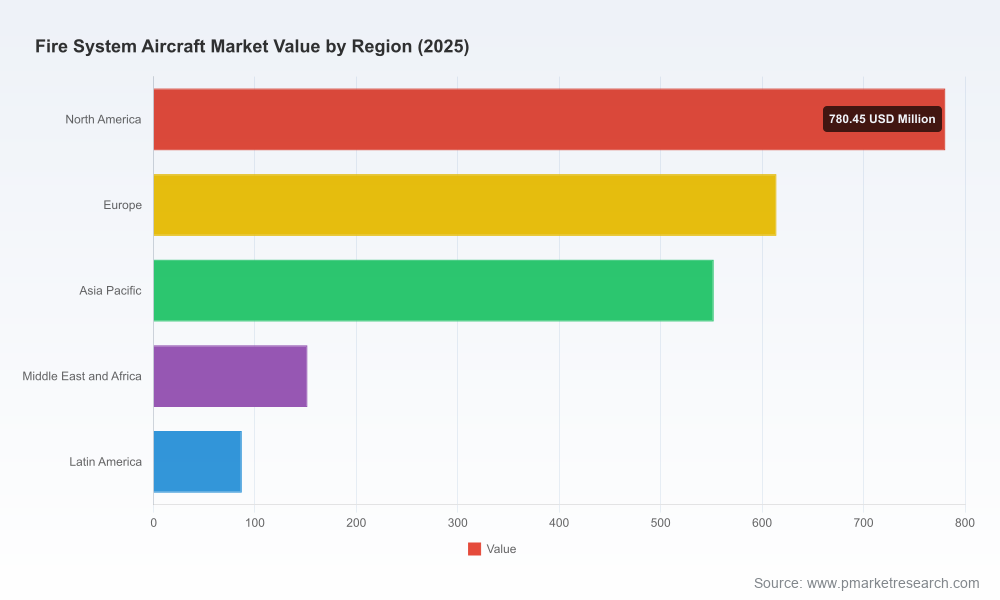

PW Consulting’s new market intelligence brief, based on a comprehensive base year of 2025 and a seven‑year forecast horizon to 2032, reframes the strategic calculus for aerospace OEMs, MROs, avionics suppliers, and fleet operators. The global aircraft fire‑system market has demonstrated steady expansion over the past half‑decade and is projected to continue growing at a steady mid‑single‑digit pace through 2032. Our proprietary model puts the market’s 2025 size firmly in the USD millions benchmark and forecasts a multi‑year rise that materializes into a materially larger addressable market by 2032 at a 4.85% CAGR (forecast period 2026–2032). For 2026 planning cycles, this trajectory translates into quantifiable demand levers across new‑build platforms, retrofit lifecycles, regulatory compliance projects, and next‑generation suppression technologies.

Worldwide Fire System Aircraft Market

Actionable timing: The convergence of regulatory deadlines, updated certification standards, and demonstrable growth in fire‑safety spend creates a narrow window in 2026 for firms to convert product development into revenue. Our report maps regulatory milestones against procurement cycles so leaders can prioritize capital and certification resources.

Worldwide Fire System Aircraft Market

Risk‑adjusted investment signals: The market’s mid‑single‑digit CAGR masks divergent sub‑trajectories by use case (in‑flight systems, cargo compartments, portable extinguishers, lithium‑battery mitigation). We translate those dynamics into risk‑adjusted project scoring to help boards and program managers choose where to commit R&D and manufacturing capacity.

Worldwide Fire System Aircraft Market

Competitive posture & concentration: the market exhibits moderate concentration (CR3 ~42.5%; CR5 ~58.3%), indicating a few large incumbents retain meaningful share while room persists for differentiated entrants and niche specialists. The brief provides a playbook for competing against incumbents, partnering with them, or occupying underserved niches.

Four structural forces will govern outcomes in 2026 and beyond: regulation, technological substitution, fleet modernization/retrofit cycles, and raw‑material & supply‑chain constraints.

Regulatory acceleration. Regulatory agencies in the US and Europe tightened timelines for halon phase‑out and issued targeted guidance on portable extinguishers and installed systems. These mandates are not theoretical: they drive mandatory retrofit programs, certification programs for halon alternatives, and supplier qualification exercises. Our analysis quantifies the likely timing and cadence of retrofit windows relative to aircraft maintenance checks so operators can align inspections, STC (Supplemental Type Certificate) schedules, and procurement.

Halon replacement & agent transition. The shift to fluorine‑free foams and clean agents (e.g., Novec‑class chemistries and engineered blends) is now irreversible. Suppliers able to demonstrate field‑proven performance, weight/volume parity, and streamlined certification pathways will capture premium pricing and aftermarket annuities. We identify technology readiness levels across candidate agents and the certification hurdles most likely to extend time‑to‑market.

Lithium‑ion battery fire mitigation. Updated airworthiness standards and new SAE powerplant fire protection guidance make lithium battery containment and suppression a primary design driver for cargo and electronics bays. This creates R&D demand for hybrid mitigation approaches that combine detection, active suppression, and thermal management—opportunities for multi‑disciplinary solution providers.

Supply chain and energetic components. The availability of high‑pressure vessels, pyrotechnic cartridges, and other energetic components influences both OEM lead times and retrofit feasibility. Our vendor risk matrix isolates single‑source dependencies and suggests mitigation strategies, from dual‑sourcing to vertical integration or long‑term purchase agreements.

The ecosystem is populated by global aerospace prime suppliers, specialty OEMs, and niche agents & service providers. Each class of player has a distinct path to capture value in 2026:

Full‑system integrators (e.g., large aerospace suppliers): These incumbents leverage deep certification experience and wide platform access to win system‑level contracts. Their advantages lie in scale, established supplier relationships, and multi‑platform footprints. However, incumbency brings legacy halon‑based product portfolios that require rapid but risk‑managed transitions.

Specialist OEMs and MRO‑facing suppliers: Companies with modular, retrofit‑friendly designs will exploit the near‑term retrofit wave. Their agility allows faster qualification for specific cargo or APU zones and effective aftersales monetization. They must, however, secure production capacity and supply of alternative agents to scale.

Component & agent specialists: Firms focused on extinguishing agents, cartridges, and foam concentrates occupy a leverage point: control of the agent roadmap gives negotiating power across OEMs and operators. These players will be central to the halon‑replacement supply chain and regulatory compliance programs.

Our report profiles leading firms across these archetypes—cataloguing strategic strengths such as product breadth, certification track record, platform approvals, and recent product initiatives—and assesses how those attributes will affect competitive advantage in 2026 procurement cycles.

Product innovation ahead of regulation: Several suppliers introduced halon‑replacement portable extinguishers and certified agent blends in late 2024–2025. These launches indicate supplier readiness to meet imminent regulatory deadlines and create a differentiated offering for fleets that must demonstrate compliance quickly.

Standards & enforcement tightening: Industry standards bodies issued updated guidance for powerplant and compartment protection, complementing regulatory deadlines on halon usage. Expect certification timelines to become the gating factor—firms that internalize new standards and pre‑engineer compliance paths will shorten time‑to‑market.

Material substitution pressure: The acceleration toward fluorine‑free foams and clean agents is compressing supplier roadmaps; candidates vary on environmental profile, firefighting performance, and compatibility with existing distribution systems. Procurement teams should prioritize supplier testing data and end‑to‑end lifecycle impact analysis over headline agent claims.

PW Consulting’s Worldwide Fire System Aircraft Market report is deliberately operational. It does not stop at high‑level trends: it arms executives with planning instruments designed for real decisions in 2026.

Scenario‑based demand models tied to maintenance cycles and regulatory compliance windows, enabling CFOs to stress‑test CapEx and cash flow outcomes under conservative and aggressive retrofit assumptions.

Supplier‑selection scorecards that weight certification velocity, technology fit, scale, and supply‑chain resilience—useful for sourcing, procurement, and partnership teams.

Certification & compliance playbooks that map the sequence of testing, STC preparation, and agency engagement required for rapid approval of halon alternatives and battery‑fire mitigation solutions.

M&A and partnership heuristics for acquiring niche capabilities (agent technology, energetic components, or retrofit engineering) versus in‑house development—complete with relative valuation sensitivities and deal structures matched to different risk appetites.

Aftermarket monetization templates that convert one‑time retrofit contracts into recurring revenue through service agreements, consumables supply, and installation training.

Prioritize certification velocity. Capitalize on early approvals for halon alternatives to secure installer pipelines and long‑term consumables contracts. Time‑to‑certification will be a leading predictor of 2026 backlog conversion.

Lock downstream supply. Negotiate multi‑year supply agreements for alternative agents and energetic components now—spot shortages and single‑source dependencies can derail retrofit programs mid‑cycle.

Design for retrofit. For OEMs and retrofit specialists, modular and weight‑efficient system designs that minimize aircraft downtime will win operator preference. Retrofit readiness must be quantified in maintenance‑window hours.

Target niche defensibility. New entrants should focus on high‑value compartments and novel mitigation for lithium‑ion risks where incumbents have thinner footprints.

Monetize services. Create bundled offerings that combine equipment, certification support, and long‑term consumable supply—operators are willing to accept premium pricing for simplified compliance and reduced administrative overhead.

PW Consulting’s report is structured to support board‑level strategy sessions, annual budgeting, and program roadmaps. For senior executives preparing 2026 initiatives, the most immediate uses are: (1) to align R&D and certification resources against the report’s timeline scenarios; (2) to prioritize shortlist suppliers using our vendor scorecards; and (3) to build contingency plans for agent supply and energetic component sourcing.

In compliance with our “trailer” approach, this release highlights the strategic implications and the high‑level metrics that merit executive attention while reserving segmented forecasts, granular regional and application splits, and detailed company benchmarking for the full report. Those deeper datasets and the interactive tools that accompany them are available on the report page—essential for teams that must convert 2026 strategy into executable programs with measurable ROI.

The aircraft fire systems market is transitioning from compliance‑driven retrofit activity into a sustained modernization cycle influenced by environmental policy, battery electrification, and the steady expansion of global air traffic. The next 12–18 months will separate firms that merely react to regulation from those that proactively shape requirements and capture post‑compliance upside. PW Consulting’s Worldwide Fire System Aircraft Market report provides the timeline, scenario analytics, and tactical playbooks to make that distinction. For executives preparing to commit resources in 2026, the question is not whether to act but how quickly and in which strategic lanes to invest.

For detailed analysis of this topic, please visit the official page:Worldwide Fire System Aircraft Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com