Experts Predict Industrial Refrigeration Equipment Will Transform Market Dynamics by 2035

Other |

2026-05-18 08:56:31

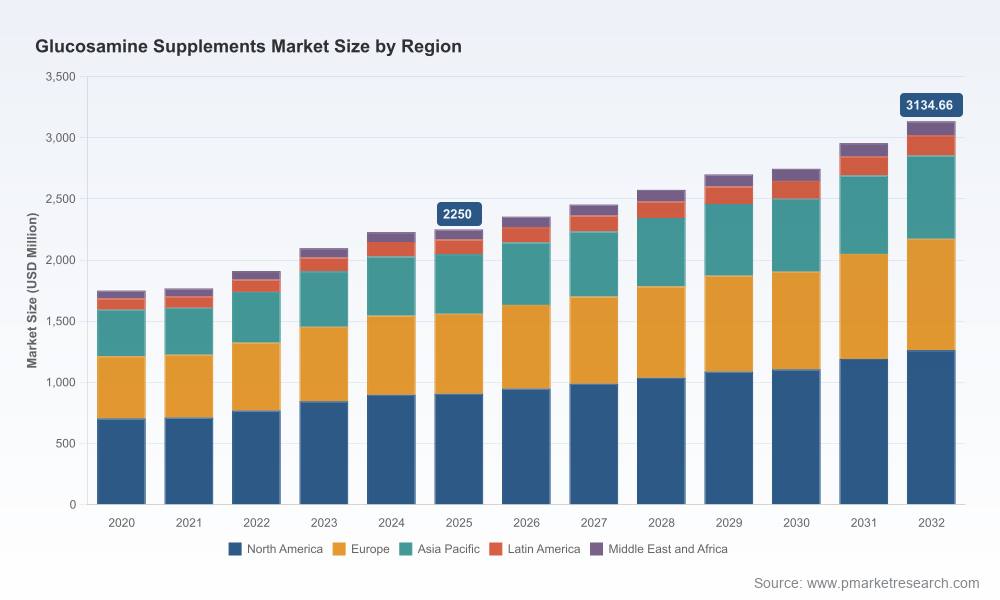

PW Consulting’s latest market intelligence brief on the Worldwide Glucosamine Supplements Market synthesizes a six-year historical view (2020–2025) with a rigorous forecast through 2032. The global market, which PW’s modelling pegs in the mid‑billions in 2025 (USD, revenue unit: Million), is projected to expand at a compound annual growth rate (CAGR) of approximately 4.85% across the 2026–2032 forecast window. This briefing highlights the practical implications and strategic choices executives should be prioritising as they formalise 2026 plans — while reserving the full, proprietary segment and regional detail for the complete report.

Worldwide Glucosamine Supplements Market

Established demand drivers: Demographic ageing, rising consumer self-care, and persistent prevalence of osteoarthritis have sustained baseline demand for glucosamine products globally, supporting stable expansion despite episodic pricing and raw‑material volatility.

Worldwide Glucosamine Supplements Market

Growth trajectory: Our scenario modelling reflects a steady expansion path underpinned by product line extensions (combination products, enhanced bioavailability formats) and distribution evolution (direct‑to‑consumer, e‑commerce marketplaces, club retail). The 4.85% CAGR to 2032 encapsulates both conservative and upside frameworks that executives should test in 2026 planning cycles.

Worldwide Glucosamine Supplements Market

Market structure: The sector displays moderate concentration (CR3 ≈ 28.5%; CR5 ≈ 35.2%), indicating room for both scale-driven incumbents and differentiated challengers. Competitive dynamics are thus shaped by brand trust, supply reliability and price positioning rather than pure oligopolistic control.

Validated sizing to stress-test budgets: The report’s validated top‑line sizing and clear growth assumptions let finance teams stress‑test 2026 revenue plans against multiple demand and cost scenarios.

Portfolio prioritisation framework: We offer an operational decision tree to identify which SKUs to invest in (e.g., premium formulations, vegetarian variants, combination products) versus which to rationalise — useful for SKU optimisation cycles scheduled in 1H 2026.

Go‑to‑market readiness: Our channel‑level demand model and e‑commerce elasticity tests help commercial teams allocate promotional spend between digital acquisition, retail displays, and value‑pack club channels for maximal 2026 ROI.

Supply‑chain playbook: With raw material sourcing cited as a major cost driver, the report includes tactical hedging and supplier‑diversification approaches for procurement leaders facing 2026 contract renewals.

Market sizing & forecasts (2020–2032) with multiple scenarios and sensitivity tables to quickly adapt plans when input assumptions change.

Commercial playbooks: SKU rationalisation matrices, trade promotion optimisation heuristics, and DTC conversion funnels tuned to glucosamine consumer cohorts.

Supply‑chain risk register and mitigation templates addressing shellfish‑derived supply dependence and opportunities in fungal/vegetarian alternatives.

Regulatory & reimbursement bulletin: Practical checklists for label claims, manufacturing compliance (GMP), and market entry constraints across major jurisdictions.

Consumer insights: Segment personas, purchase drivers (including the high penetration among older adults self‑managing knee osteoarthritis), and evidence‑communication playbooks for advertising and medical affairs teams.

Competitive playbook: Company profiles, go‑to‑market benchmarking, and M&A watchlists, plus an annex of recent product launches, certifications and clinical evidence developments.

The market is anchored by well‑known dietary supplement brands, regional leaders and value‑focused private‑label players. Key firms analysed in the report include:

NOW Foods (Bloomingdale, IL, USA; https://www.nowfoods.com) — a scale manufacturer with broad formulations and a recent product upgrade integrating collagen‑based components. NOW’s strength lies in manufacturing breadth and portfolio depth, making it a bellwether for pricing and channel trends.

Nature’s Bounty (Ronkonkoma, NY, USA; https://www.naturesbounty.com) — a household brand that recently secured third‑party certification, reinforcing its quality positioning; a useful comparator for premiumisation strategies tied to certification and trust signals.

Doctor’s Best (Irvine, CA, USA; https://www.drbvitamins.com) — targeted at differentiated formulations (e.g., specific sulfate/optimum blends) and vegetarian capsule formats, reflecting a profitable niche play for ingredient innovation.

Jarrow Formulas (Los Angeles, CA, USA; https://jarrow.com) and Thorne Research (Summerville, SC, USA; https://www.thorne.com) — science‑forward brands using combinatorial formulas and clinical evidence to defend price premia; Thorne’s recent clinical publication underscores the value of investing in independent studies.

Pure Encapsulations, Kirkland Signature (Costco), GNC, Swanson, Nutricost, Blackmores and Nature Made — these players illustrate the breadth of positioning from value and club retail to regionally strong formulators and USP‑verified offerings. Their tactics inform scenarios around private‑label competition and retail partnership strategies.

Across these players, recent actions to monitor include product launches that bundle glucosamine with collagen and MSM, third‑party certifications that reduce consumer friction, clinical evidence publications that enable stronger structure/function communications, and regional distribution expansions.

Cost drivers: Primary sourcing from shellfish exoskeletons remains a dominant input source and drives a material share of production cost. Vegetarian, fungal‑sourced glucosamine offers strategic differentiation but at a premium cost — an important trade‑off for premium or clean‑label positioning.

Procurement levers for 2026: PW recommends multi‑supplier contracting, structured options for rotating between marine and fungal sources, and strategic inventory buffers ahead of planting seasonal volatility into supplier lead times.

Regulatory context: In core markets like the US, glucosamine sits within dietary supplement frameworks (DSHEA), which limits pre‑market scrutiny but requires strict GMP compliance. In the EU, historical EFSA positions constrain claim language and require conservative labeling approaches.

Reimbursement reality: Glucosamine is generally not reimbursed under major public drug programs, constraining price accessibility for some patient cohorts and reinforcing the importance of private‑pay consumer affordability strategies.

Evidence strategy: Given mixed regulatory positions on efficacy claims, investing selectively in peer‑reviewed clinical work or real‑world evidence campaigns (e.g., pragmatic studies, registries) yields outsized marketing and formulary value when used rigorously.

Scenario‑based portfolio investment: Use the report’s demand scenarios to rank SKU investments by expected margin contribution and strategic fit (premium vs. value). Prioritise a limited number of premium SKU launches supported by certification or clinical data to avoid diluting marketing spend.

Channel mix reallocation: Rebalance trade spend toward direct digital channels and subscription models while maintaining selective club/retail presence for high‑volume SKUs — test hybrid pricing in Q1–Q2 2026.

Procurement rewiring: Implement supplier diversification pilots for vegetarian glucosamine and negotiate flexible pricing collars with key marine suppliers ahead of 2026 contract renewals.

Evidence & claims roadmap: For brands seeking premium positioning, plan one clinical or real‑world evidence study with publication objectives in 2026 to underpin improved label and OOH (out‑of‑home) messaging in key campaigns.

M&A & partnerships: For incumbent players seeking growth, bolt‑on acquisitions of regional leaders or contract manufacturers with vegetarian sourcing capabilities offer rapid capability acquisition without long lead times.

In line with our ‘trailer’ approach, this preview conveys the strategic signals and actionable recommendations derived from the full analysis while withholding the granular regional, type and application revenue splits and SKU‑level unit economics. These detailed tables and proprietary segmentation models are available exclusively in the full report and interactive dashboard to ensure clients receive the complete evidence base needed for board‑level decisions.

PW Consulting’s Worldwide Glucosamine Supplements Market report is designed as a working tool for commercial, procurement and corporate strategy teams preparing 2026 budgets and three‑year plans. For immediate access to the full dataset (regional and application splits, SKU economics, supplier scorecards, and the interactive scenario modeller), contact your PW account executive or visit our report page. Clients can also commission a short briefing workshop (virtual or on‑site) where our analysts will walk through the model and adapt scenarios to your specific P&L and operational constraints.

Prepared by PW Consulting — Senior Strategic Advisor & Chief Industry Analyst, Supplements Practice. Our methodology blends triangulated market sizing, primary supplier and retailer interviews, clinical evidence review, and bespoke demand modelling to deliver practical, decision‑ready insight for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Glucosamine Supplements Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com