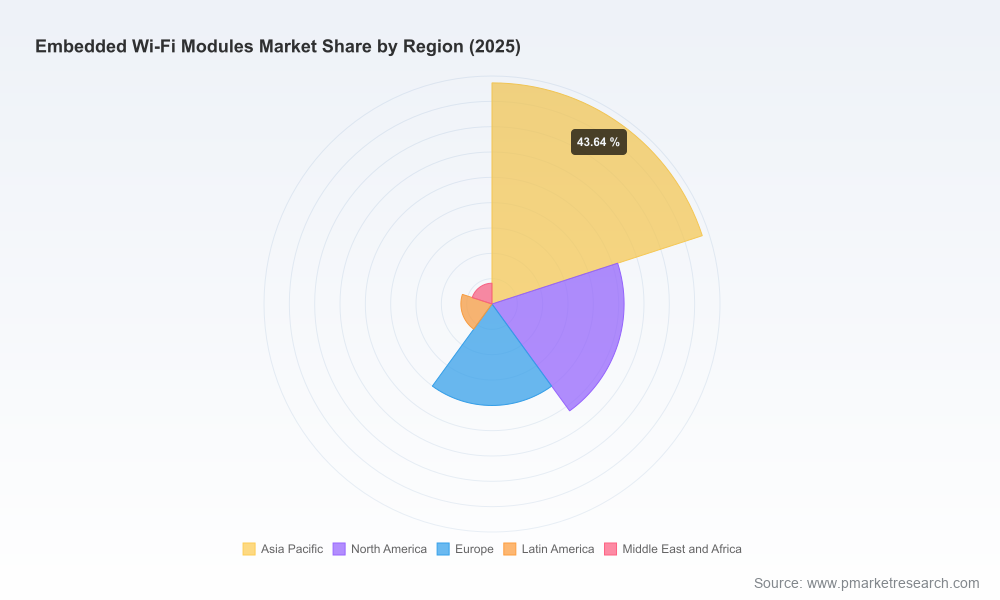

PW Consulting: Embedded Wi‑Fi Modules Market Poised to Surge at a 13.59% CAGR Through 2032

Other |

2026-07-07 06:19:41

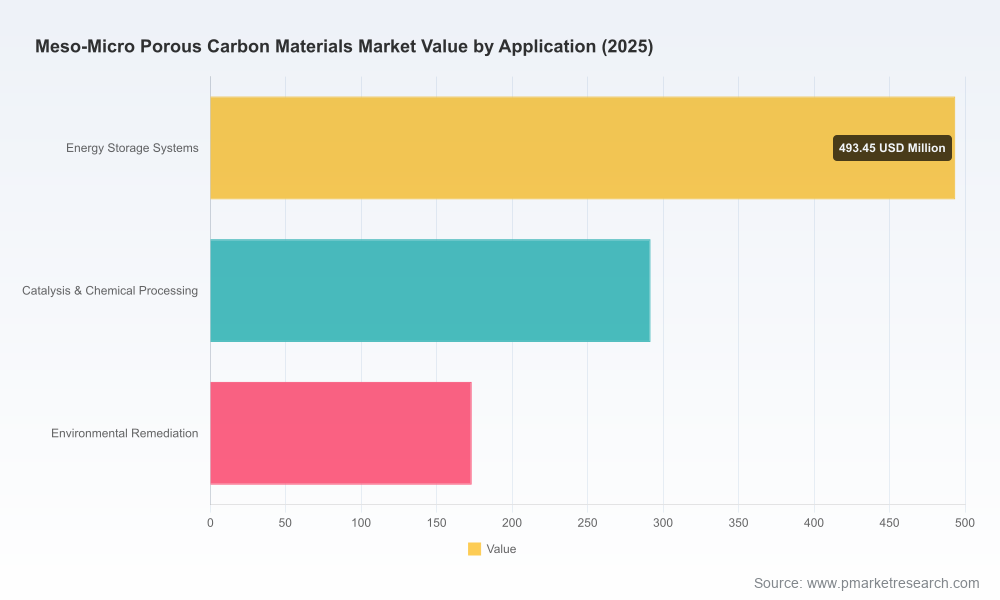

PW Consulting’s latest market study on Worldwide Meso‑Micro Porous Carbon Materials sets a clear strategic frame for executives preparing capital allocation, supply‑chain, and technology roadmaps in 2026. The sector that produced roughly USD 958 million in revenue in the 2025 base year has shown a sustained acceleration since 2020 and is forecast to nearly double by the end of the 2032 horizon under a compound annual growth rate of approximately 9.9%. This growth is being driven by simultaneous demand pull from advanced energy storage systems, higher‑performance adsorption for water and air treatment, and expanding industrial uses in catalysis and chemical processing.

Worldwide Meso-Micro Porous Carbon Materials Market

Regulatory inflection and investment timing. Strengthened regulatory frameworks for water contaminants and air emissions in key markets are converting long‑tail procurement cycles into near‑term tender pipelines. For many corporate buyers and suppliers, 2026 is the year to re‑align capacity and product roadmaps to capture contracts that will stretch well into the next decade.

Worldwide Meso-Micro Porous Carbon Materials Market

Raw material volatility requires strategy. Feedstock availability and price volatility accelerated materially in 2025, forcing manufacturers to revisit procurement strategies, feedstock mix, and processing economics. Firms that act now to diversify sources or to lock in localised supplies will gain cost and lead‑time advantages.

Worldwide Meso-Micro Porous Carbon Materials Market

Technology bifurcation. The market is bifurcating into engineered mesoporous products with tightly controlled pore networks for high‑value energy and analytical uses, and higher‑volume activated porous carbons for bulk purification and remediation. Positioning between these two trajectories will dictate margin profiles and capital intensity.

Our modelling—rooted in a 2025 base year and projecting across a 2026–2032 forecast period—shows the industry expanding from under USD 1.0 billion in 2025 to a market size that approaches the USD 1.85 billion mark by 2032 if current trends persist. The implied mid‑single‑digit acceleration embedded in that trajectory corresponds to a near‑10% CAGR across the forecast window, underscoring a structurally attractive growth profile for both incumbent producers and new entrants focusing on specialty mesoporous chemistries.

Regulatory drivers: Tighter standards for persistent contaminants, alongside renewed scrutiny on air toxic emissions, are increasing technical specifications for adsorbents used in municipal and industrial treatment systems. This is creating a sustained, technology‑sensitive procurement stream that prizes performance metrics like adsorption kinetics, selectivity, and reactivation potential.

Supply chain and feedstock risk: The sector faces compressed raw‑material availability and price shock exposures that materially influence unit economics. In response, several players are accelerating strategies to secure domestic or alternative biomass feedstocks, invest in reactivation capabilities, and pursue backward integration where it supports margin protection.

Product and process innovation: Advances in ordered mesopore architectures and template synthesis are enabling performance gains in battery electrodes and membrane integrations. At the same time, scaled activated carbon processes continue to deliver improved BET surface areas and mesopore development that extend applicability into demanding environmental and pharmaceutical streams.

Market concentration: The sector shows moderate concentration at the top; our analysis indicates that the largest three firms command roughly four‑tenths of the market by revenue, while the top five capture closer to six‑tenths. That structure creates an environment where scale matters—particularly for large municipal contracts and reactivated carbon supply—yet differentiated technology can yield outsized returns in targeted niches.

Our report profiles the leading suppliers and synthesizes the strategic playbook each is following. A few themes emerge:

Scale and system integration (global incumbents). Established suppliers with integrated footprints are prioritising capacity expansions and domestic sourcing to mitigate trade and tariff risk and to service large infrastructure contracts. They are also buying or building reactivation capacity to extend product life cycles and to present circular value propositions to large water and utility customers.

Technology differentiation (specialist producers). Firms with proprietary mesopore architectures are leveraging partnerships with academic labs and system integrators to commercialise next‑generation electrodes, membranes, and catalytic supports. These players are less focused on volumetric share and more on performance leadership and intellectual property monetisation.

Feedstock and sustainability plays (niche champions). Suppliers focused on coconut shell, pine, or agricultural residue feedstocks are emphasising traceability and lower carbon footprints—an increasingly important procurement filter for ESG‑driven buyers.

Recent industry moves illustrate these archetypes: leading global manufacturers are expanding reactivation and domestic production capacity to address municipal water and contaminant treatment demand; technology corporations are formalising research partnerships to scale mesoporous electrode constructs for advanced battery chemistries; and several players have announced pilot projects converting non‑fossil biomass into pore‑engineered carbon feedstocks.

The report is intentionally designed as an operational playbook for 2026 decision cycles. Key deliverables include:

High‑fidelity market model and scenario suite — base and stress forecasts for 2026–2032 that quantify upside from accelerated regulatory adoption and downside from prolonged feedstock constraints (note: segment‑level figures and full scenario matrices are reserved for the full report).

Commercial due diligence templates — supplier scorecards, contract negotiation checklists, and unit‑cost models that link feedstock inputs to finished‑product economics and margin sensitivity.

Supply‑chain playbook — mapping critical raw‑material dependencies, alternative sourcing routes, and inventory strategies to mitigate price shocks and delivery interruptions.

Technology and IP roadmap — comparative analysis of ordered mesopore vs activated routes, key levers to scale R&D outcomes into manufacturable products, and a patent landscaping module to prioritise partnership or licensing targets.

M&A and investment benchmarks — an actionable deal pipeline, valuation heuristics specific to porous carbon businesses, and case studies that show when to pursue capacity acquisitions versus greenfield builds.

Regulatory risk matrix — a decision‑ready analysis of current and pending rules (water contaminants, air toxics) and their procurement implications by customer segment, with recommended engagement strategies for regulators and large buyers.

For executives setting 2026 priorities, the report highlights a small set of high‑impact moves:

Hedge feedstock exposure. Secure multi‑source supply agreements, invest in reactivation assets where scale permits, and pilot biomass feedstock conversions to lower OPEX volatility and to create ESG differentiation.

Prioritise product segmentation. Define a clear product portfolio split between premium mesoporous engineered products and higher‑volume activated carbons; allocate R&D and commercial resources accordingly to avoid margin dilution.

Accelerate partnership models. Use co‑development agreements with research institutes and battery/system OEMs to de‑risk scale‑up of advanced carbon architectures and to shorten time‑to‑market for high‑value applications.

Target capacity localisation. Where tender pipelines are driven by regulatory procurement, establish or acquire domestic production to avoid tariff and logistics exposure, and to win specification‑sensitive contracts.

Operationalise circularity. Develop reactivation and recycling offers as service layers to create recurring revenue and to strengthen retention among large municipal and industrial clients.

Refine M&A criteria. Prioritise targets that either (a) add locked‑in feedstock access, (b) offer proprietary pore architectures with clear scale pathways, or (c) bring validated, contracted channels into regulated end markets.

Beyond forecasting, the report’s value is practical and immediate: it converts macro trends into executable initiatives with timelines, cost‑benchmarks, and KPI dashboards customisable by executive function (commercial, operations, R&D, and corporate development). Whether the objective is to bid for large municipal water contracts, to partner in next‑generation energy storage, or to rationalise a global supply footprint, the report provides the decision support tools to act with confidence in 2026.

This public preview outlines the strategic context and the levers executives must consider. The full Worldwide Meso‑Micro Porous Carbon Materials Market report contains the proprietary modelling, segmented forecasts, company scorecards, supplier benchmarking, and executable playbooks referenced above. It also includes downloadable financial models and a prioritised list of M&A targets and R&D partners. We designed the deliverables to be directly usable in board‑level capital plans and procurement RFQs—so leadership teams can translate insight into action without delay.

For procurement leaders, corporate strategists, and investors preparing 2026 plans, the timing to act is now. Contact PW Consulting to access the full dataset, scenario models, and the tailored advisory services that convert market intelligence into measurable business outcomes.

For detailed analysis of this topic, please visit the official page:Worldwide Meso-Micro Porous Carbon Materials Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com