Worldwide N‑Methyl Diethanolamine (MDEA) Market — Strategic Outlook for 2026 Decision‑Makers

Introduction

As energy transition timelines, refining economics, and carbon‑management programs accelerate, N‑Methyl Diethanolamine (MDEA) has moved from a niche solvent to a core strategic material across gas treating, CCS pilots, and a growing set of industrial intermediates. PW Consulting’s new Worldwide N‑Methyl Diethanolamine (MDEA) Market report (base year 2025, historical window 2020–2025, forecast 2026–2032) quantifies this shift and converts it into an actionable playbook for executives making procurement, plant‑level, and M&A decisions in 2026.

Worldwide N-Methyl Diethanolamine (MDEA) Market

Market snapshot: scale, trajectory, and concentration

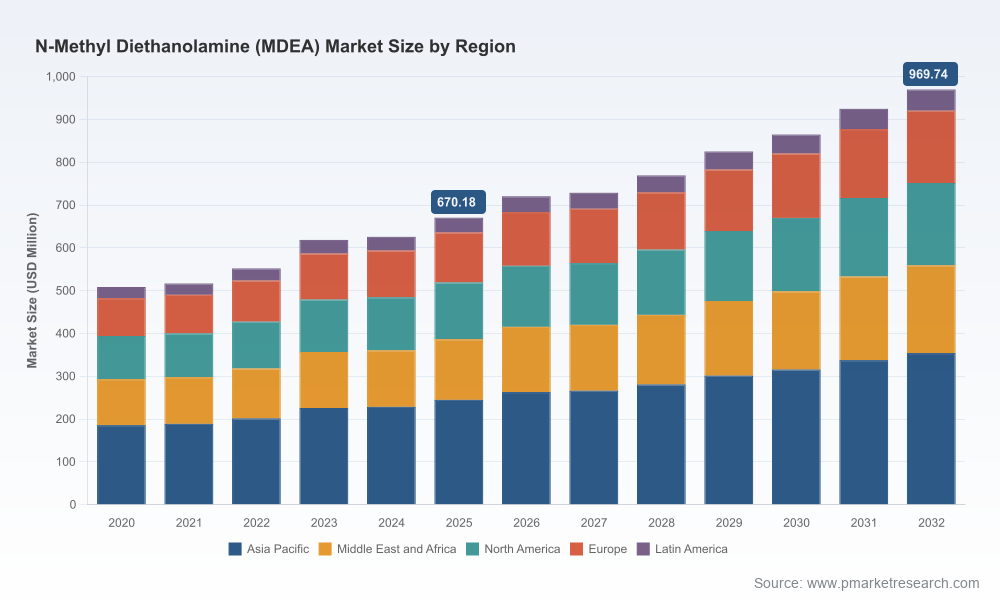

After steady expansion through the early 2020s, the MDEA market reached approximately USD 670.18 Million (revenue, base year 2025). Our forecast models project continued growth into the next decade, with the market entering 2026 at an estimated USD 720.21 Million and reaching roughly USD 969.74 Million by 2032. This trajectory corresponds to a compound annual growth rate (CAGR) of about 5.42% for the forecast period, reflecting durable demand drivers balanced against periodic feedstock and capacity volatility.

Worldwide N-Methyl Diethanolamine (MDEA) Market

Market concentration is meaningful but not prohibitive: the top three producers capture near‑majority share, with the top five increasing that share further. That marketplace structure creates zones of both competition and coordination — pricing and service differentiation will therefore be strategic levers for both incumbents and challengers in 2026.

Worldwide N-Methyl Diethanolamine (MDEA) Market

Why this matters for 2026 corporate decisions

- Procurement and cost exposure: Feedstock and intermediate price dynamics are already shaping MDEA economics. Ethoxylation of methylamine with ethylene oxide remains the core manufacturing route, and feedstock swings (illustrated by notable regional DEA price increases in 2025) materially impact supplier economics and negotiating posture. Buyers should reassess contract tenors, indexation clauses, and optionality strategies now, not later.

- Capacity and supply risk: Recent capacity additions and announced projects are changing regional supply balances. Where new large‑scale capacity comes online, negotiating leverage may improve; where capacity is constrained, short‑term spot tightness can yield rapid price moves. In 2026, decision‑makers must layer capacity‑aware sourcing and contingency plans into procurement processes.

- Product quality segmentation: High‑purity grades tailored for gas treating and CCS command differentiated value. Investment or partnerships that secure access to “GT‑grade” or accelerator‑compatible formulations (e.g., MDEA blends used in advanced capture solvents) will affect competitiveness in downstream services and projects.

- Regulatory compliance & CCS opportunity: MDEA’s technical profile — selective H2S removal and compatibility with CO2 capture boosters — makes it central to both near‑term compliance and longer‑term carbon management strategies. Capital allocation for low‑carbon projects or for retrofits in gas processing should explicitly model solvent supply scenarios.

What the report delivers — practical, decision‑ready intelligence

PW Consulting’s study is structured to convert market intelligence into executable choices for 2026. Highlights include:

- Top‑down demand forecasting by use case, with sensitivity bands driven by energy market scenarios and CCS adoption curves.

- Supply‑side analysis including plant‑level capacity, recent project timelines, and supplier risk scores mapped to logistics corridors.

- Cost‑to‑make models that embed feedstock price benchmarks (methylamine, ethylene oxide, ammonia, methanol) for a reference plant scale, enabling unit‑cost simulation under alternative raw material trajectories.

- Commercial playbooks for buyers and suppliers — from short‑term spot management to medium‑term tolling and joint‑venture options — with term sheet templates and negotiation levers tailored to different buyer sizes and geographies.

- Scenario‑based regulatory and technology assessments including solvent formulation roadmaps for low‑carbon capture (e.g., MDEA + accelerators) and implications for product purity and logistics.

- Competitive benchmarking and M&A screening — qualitative profiles of active producers, recent strategic moves, and an acquisition target shortlist with preliminary valuation bands (full data available in the report appendix).

Competitive landscape — how incumbent strategies shape 2026 choices

The market features a set of established global producers and several regional specialists. Leading multinationals emphasize integrated chemistry platforms and specialty formulations; regional players focus on cost‑competitive supply and proximity to local gas processing hubs.

- Global integrators: Firms with broad chemical portfolios and global feedstock integration have strategic advantages in stabilizing supply and investing in high‑purity grades for gas treating and CCS. Their recent moves include world‑scale capacity investments and targeted premium product positioning.

- Specialty formulators: Several players differentiate through proprietary MDEA formulations for deep CO2 removal or selective H2S removal. These formulations, combined with service contracts, raise switching costs for large industrial customers.

- Regional manufacturers: Cost‑competitive local producers supply volume into regional value chains where logistics and regulatory alignment favor shorter supply loops.

Notable recent industry signals that should inform 2026 plans:

- A major European chemical producer completed a large new alkyl ethanolamines plant in 2024, materially adding global capacity and altering supplier dynamics for alkyl amines.

- A leading North American specialty chemical company implemented a price increase for a flagship MDEA product in early 2026, reflecting either input cost pressure or tightening capacity utilization — a signal buyers should treat as an early warning for broader price risk.

- An announced greenfield licensing and build project in South Asia (mid‑scale) will add future optionality and underscores the role of regional new entrants in moderating price spikes.

Raw‑material, cost drivers and production economics

MDEA production economics are sensitive to a narrow set of upstream inputs. Ethylene oxide and methylamine are central to the ethoxylation route; other macro inputs such as methanol and ammonia matter for integrated chemical manufacturing cost stacks. Our reference‑plant cost models (anchored to an industry standard capacity assumption) allow users to test unit cost under alternate feedstock and energy price scenarios — a crucial capability for capital budgeting and buy/sell decisions in 2026.

Regional feedstock price movements through 2025 show meaningful divergence that has already affected regional cost differentials. Buyers should incorporate regional feedstock indices into contract clauses, and producers should evaluate hedging or forward procurement strategies to stabilize margins.

Regulation, technology and the CCS axis

MDEA is not just a conventional amine solvent; it is a strategic asset for decarbonization pathways. Its use in selective H2S removal remains foundational for gas processing and refining, and its formulations — including blends with piperazine accelerators — make it relevant for several CCS pilot and commercial capture solutions. Regulation pushing reduced greenhouse emissions and stricter gas quality specs will increase demand volatility and create premium product niches. Companies aligning product development and sales efforts with CCS and low‑carbon roadmaps will capture disproportionate long‑term value.

Actionable playbook for executives — prioritized moves for 2026

- Immediate (0–6 months): Reassess procurement contracts to include feedstock indexation, flexible delivery windows, and optionality to rebalance as new capacity comes online. Run supplier stress tests incorporating announced capacity additions and regional feedstock shocks.

- Near term (6–18 months): Secure access to high‑purity grades via long‑term agreements or tolling arrangements if your portfolio relies on gas‑treating performance. Launch pilot agreements with specialty formulators to qualify solvents for CCS/CO2 capture projects.

- Medium term (18–36 months): Consider strategic investments — minority stakes, JV capacity, or downstream service integration — to internalize supply security and create differentiated offerings tied to carbon management services.

- Cross‑cutting governance: Integrate solvent supply scenarios into enterprise risk management, and create a cross‑functional steering committee (procurement, operations, project development, regulatory) to monitor market signals and trigger pre‑defined playbooks.

Why PW Consulting’s report is a strategic asset for 2026

This report is explicitly engineered to move beyond descriptive market commentary. It combines rigorous bottom‑up modelling, plant‑level supply intelligence, and commercial playbooks so that CFOs, procurement heads, plant managers, and corporate development teams can convert market trajectories into concrete decisions. The study’s datasets and scenario engines enable you to stress‑test capital projects, price risk, and supplier strategies under credible 2026 market conditions.

Next steps — where to get the full intelligence

The deliverables summarized above are intentionally high‑level in this release to highlight strategic implications while reserving the granular segment tables, plant‑by‑plant capacity schedules, and downloadable cost models for report subscribers. For teams that need to underwrite contracts, allocate capital, or run M&A diligence in 2026, accessing the full report and accompanying dataset is the fastest way to translate the trends and scenarios described here into executable plans.

Contact PW Consulting’s Chemicals & Energy practice to request the full Worldwide N‑Methyl Diethanolamine (MDEA) Market report, obtain customised scenario runs for your asset base, or commission a tailored supplier risk assessment ahead of contract negotiations in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide N-Methyl Diethanolamine (MDEA) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com