Post-Consumer Recycled Plastics Market Trends and Growth Analysis with Forecast by Segments

Other |

2026-07-16 13:06:56

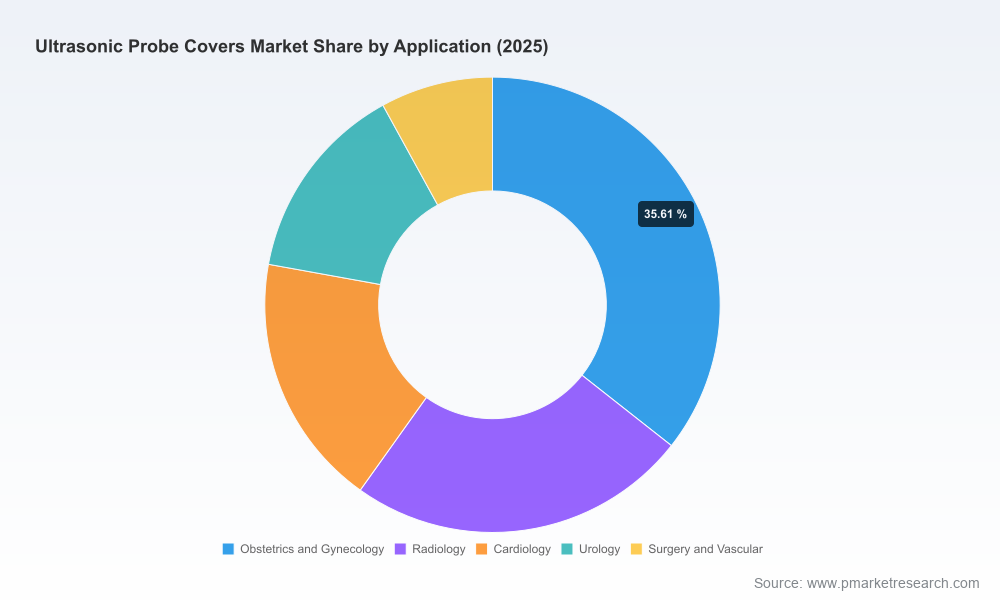

As healthcare systems prioritize infection prevention, and ultrasound use broadens across ambulatory and point-of-care settings, the market for ultrasonic probe covers is entering a phase of structurally higher demand and strategic reorientation. PW Consulting’s new market study — based on a 2025 base year and a full forecast to 2032 — finds the market valued at roughly USD 230 million in 2025 and projected to expand at a compound annual growth rate of 6.5% through 2032, approaching an estimated USD 357 million by the end of the forecast horizon. For executives planning capital allocation, product development, and commercial strategies in 2026, this report crystallizes the operational levers and competitive plays that matter most.

Worldwide Ultrasonic Probe Covers Market

Regulation and compliance are converging with clinical practice. Sterile probe covers face differing regulatory pathways — ranging from Class I exemptions to Class II devices requiring 510(k) clearance in jurisdictions such as the United States — and sterile products must conform to ISO packaging and sterilization standards. Manufacturers that front-load regulatory readiness will shorten commercialization timelines and reduce recall risk.

Worldwide Ultrasonic Probe Covers Market

Infection control remains non-negotiable. Public health guidance increasingly favors disposable covers for endocavitary and intracavity examinations; this has translated into higher procedural adoption and a willingness among some health systems to pay a premium for demonstrable infection-risk mitigation.

Worldwide Ultrasonic Probe Covers Market

Procurement dynamics are tightening. There is no dedicated HCPCS code for probe covers in major reimbursement systems; cover costs are commonly absorbed within ultrasound procedure codes. That reality drives price sensitivity and pressures suppliers to build compelling total-cost-of-ownership arguments for clinical buyers.

Material and manufacturing inputs are shifting. Demand for latex-free formulations and high-clarity films is driving technical differentiation — affecting supplier sourcing, sterilization choices, and unit economics.

Material innovation as a competitive axis. Medical-grade polyurethane and polyethylene films (and other latex-free alternatives) are now table stakes for clarity and biocompatibility. Suppliers able to combine material performance with efficient sterilization (EO, gamma, or alternative methods) command better hospital adoption.

Single-use economics vs. sustainability pressures. Hospitals evaluate disposables not only on per-unit price but on workflow time-savings and infection-avoidance value. Simultaneously, sustainability agendas and procurement policies are elevating the importance of recyclability, reduced packaging volumes, and sterilization footprint.

Channel and OEM partnerships. Integration with ultrasound OEMs and embedding probes/cover bundles into purchasing frameworks accelerates uptake. Companies that can supply validated, OEM-compatible solutions with compatible adhesives/fixtures shorten buyer evaluation cycles.

Supply chain resilience. Geopolitical shifts, raw material price volatility, and sterilization-capacity constraints require multi-sourcing strategies and strategic inventory management to prevent interruptions in clinical supply.

The market is moderately concentrated: the top three global suppliers control roughly two in five dollars of the market, and the top five approach three in five. This concentration reflects incumbent advantages in regulatory track records, distribution networks, and validated clinical compatibility. Key competitors, and the strategic signals they send, include:

CIVCO Medical Solutions (Coralville, IA, USA) — Strong breadth across sterile and non-sterile disposables and established channel relationships. Recent exhibition activity at major radiology forums underscores a push to strengthen sterile endocavity offerings and clinical visibility; expect continued emphasis on portfolio breadth and clinical validation to defend accounts.

Parker Laboratories (Fairfield, NJ, USA) — Known for gel-free, low-profile designs (Incognito line). Parker favors infection-control differentiation and usability gains that reduce setup time — a credible route to premium pricing in high-volume environments.

Kentec Medical (Bicester, UK) — EU-regulation-focused supplier with MDR compliance and established endocavity sheaths. Its strength lies in meeting stringent regional regulatory requirements and servicing global markets through certification-driven trust.

Sunray Medical (Edison, NJ, USA) — FDA-cleared product range and attention to imaging clarity. Sunray’s pathway centers on medical-grade assurance and targeted clinical claims to win hospital procurement committees.

ImaX Medical (Montreal, Canada) — Focused on high-clarity disposable solutions for specialized probes (including TEE). Niche clarity-led differentiation attracts imaging-first customers and OEM collaborations.

Across these players, common strategic moves include: regulatory capture (preparing 510(k) dossiers for sterile SKUs), strengthening sterilization partnerships, expanding OEM compatibility statements, and investing in clinical data demonstrating infection-control outcomes. New entrants should anticipate a high bar on validated claims and distribution depth.

Regulatory and quality assurance: Prioritize ISO 11607 packaging validation and select sterilization modalities aligned with scale. Build capacity for regulatory submissions (510(k) where applicable) before product launch to avoid commercialization delays.

Value-based commercial models: Move beyond unit price competition by quantifying procedure-level savings (reduced turnover time, infection avoidance) and packaging those savings into clinical tender responses and KOL-supported value dossiers.

Manufacturing footprint decisions: Balance near-shore capacity for critical sterile SKUs with offshore cost advantages for commoditized lines. Layer buffer inventory and multi-sourcing agreements for key polymer films and sterilization slots.

Portfolio segmentation: Offer a tiered portfolio (economy, clinical-optimized, premium diagnostic-grade) to capture multiple buyer value propositions while ensuring regulatory equivalence for sterile tiers.

Commercial partnerships and channels: Lock in OEM compatibility test results and co-marketing arrangements; explore bundled offerings with ultrasound OEMs and distributers to reduce friction in hospital adoption.

M&A and inorganic play: Given moderate concentration, acquisitive plays — particularly for regional sterile-manufacturing capacity or proprietary materials — can accelerate market access and margin expansion.

This preview captures the strategic contours; the full report provides the operational depth that executive teams use to make 2026 decisions. Key deliverables include:

Detailed market sizing and seven-year forecasts with scenario analyses and sensitivity testing tuned to raw-material and sterilization-capacity shocks.

Full segmentation by region, material type, application and channel — accompanied by growth drivers and buyer personas for each segment.

Competitive benchmarking with capability maps, commercialization timelines, and validated clinical claims analysis for leading companies.

Regulatory pathway and reimbursement mapping — practical checklists for 510(k) readiness, ISO compliance, and procurement bidding strategies.

Supply-chain heatmaps, supplier scorecards for polymer films and sterilization partners, and recommended mitigation plans for single-source risks.

Commercial playbooks: pricing matrix templates, tender-response decks, and a buyer ROI calculator to support hospital procurement conversations.

M&A and investment case models with valuation scenarios tailored to product mix, regulatory status, and geographic reach.

Rapid diligence and go-to-market sprints: From validation of clinical claims to field pilots with leading hospitals, we run 8–12 week sprints that compress risk and accelerate revenue realization.

Regulatory readiness programs: Tailored support for 510(k) submissions, ISO packaging qualifications, and sterilization validation plans — reducing time-to-market and regulatory friction.

M&A advisory and integration planning: Target screening, commercial synergy modeling, and post-close integration blueprints that protect margins and preserve market access.

Commercial toolkit deployment: Custom pricing calculators, tender-response templates, and clinical economics dossiers built for procurement committees.

For manufacturers and investors targeting the ultrasonic probe covers space, 2026 demands a dual focus: operational resilience and clinical differentiation. The market is growing at a sustainable mid-single-digit CAGR, creating opportunities for premium positioning while leaving room for consolidation. Companies that secure regulatory certainty, invest in high-clarity, latex-free materials, and align commercial models with hospital value metrics will outperform peers. PW Consulting’s full report provides the granular segmentation, company-level benchmarking, and executable playbooks required to convert these trends into competitive advantage. For access to the complete dataset, downloadable appendices, and bespoke advisory engagements, visit the report page or contact PW Consulting’s healthcare strategy team.

For detailed analysis of this topic, please visit the official page:Worldwide Ultrasonic Probe Covers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com