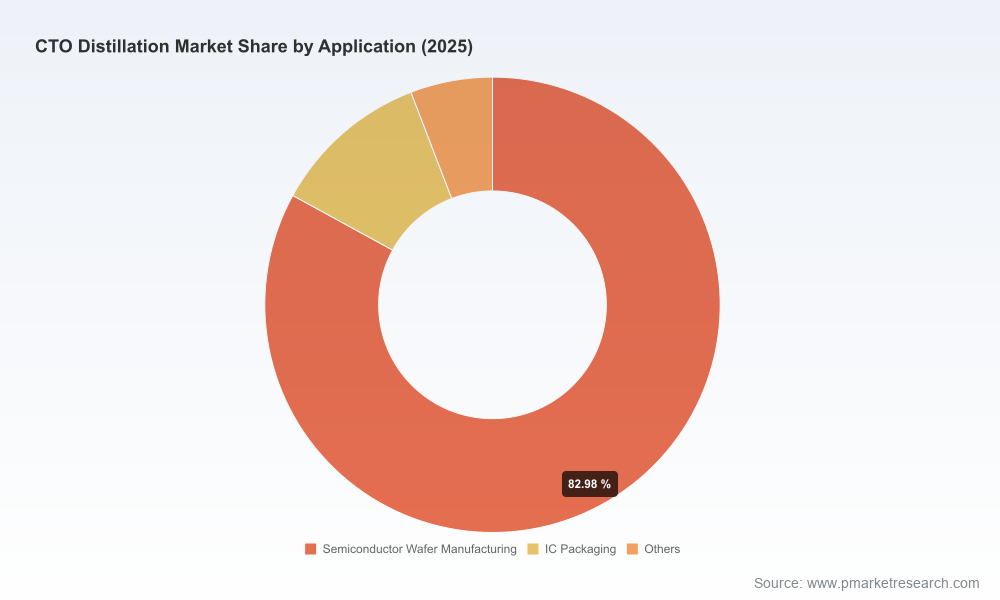

PW Consulting: CTO Distillation Market Poised for 5.6% CAGR to USD 344.8M by 2032

Technology |

2026-07-12 07:04:49

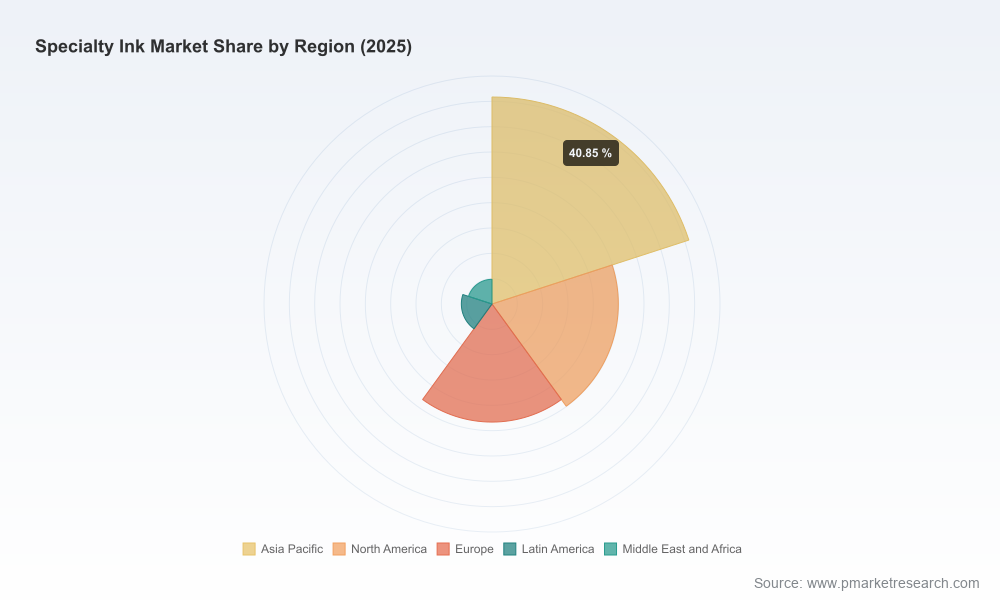

PW Consulting’s newest market intelligence brief on the Worldwide Specialty Ink Market provides executives and functional leaders with the forward-looking context they need to make high-stakes strategic decisions in 2026. Anchored on a 2025 base year and a robust historical review covering 2020–2025, the report maps out the market’s trajectory through a 2026–2032 forecast window. Our core forecast shows the global specialty ink market expanding at a compound annual growth rate (CAGR) of 5.24%, rising from roughly USD 3.51 billion in 2020 to approximately USD 4.52 billion in 2025 and targeting about USD 6.47 billion by 2032.

Worldwide Specialty Ink Market

For executive teams evaluating capital allocation, M&A targets, sourcing strategies, or new product launches, these forces combine to make 2026 a year in which timing and structural positioning matter more than tactical cost-cutting.

Worldwide Specialty Ink Market

PW Consulting’s Worldwide Specialty Ink Market report is designed for operators who need to act. Rather than reprinting elementary market statistics, the report provides a toolbox of actionable deliverables that translate market trends into executable strategies. Highlights include:

Worldwide Specialty Ink Market

We deliberately present narrative and scenario-based insight in the public summary to establish analytical confidence. The report itself contains the granular segmentation and proprietary forecasts central to commercial decision-making; we keep those in the full report to preserve client value and to encourage direct engagement with PW Consulting.

The specialty ink industry sits at a moderate concentration level: the three largest companies account for a meaningful share of global volumes, and the top five cumulatively command just over half of market revenue. This concentration creates both competitive stability and strategic vulnerability. Large players can scale reformulation and compliance programs quickly, but they also face structural challenges when raw-material shocks hit global procurement simultaneously.

Market participants to watch include global integrated producers and innovation-oriented specialists. Leading firms provide a diversified mix of packaging, digital, UV/LED-curable, and functional inks as part of a broader portfolio of coatings and chemical solutions. In recent months several headline moves have demonstrated the strategic playbook in action:

For procurement and corporate development teams, the immediate implication is clear: the balance of power is shifting toward suppliers who can demonstrate secure, compliant feedstock sourcing and rapid reformulation capabilities. For acquirers, the most valuable targets will be those with differentiated technology platforms or regulatory-compliant formulations that shorten a buyer’s path to market.

Based on our integrated market model and supplier assessments, we advise companies to prioritize a balanced set of tactical and strategic moves in 2026:

Procurement teams will find our supply-chain stress tests and supplier scorecards useful for redesigning contracts and inventory strategies. R&D leaders will benefit from the technology adoption timelines and reformulation cost curves to prioritize projects that deliver the fastest route to compliant revenue. Corporate development and private equity teams can use the report’s M&A heat maps and valuation sensitivities to calibrate bids and integration plans against realistic 2026–2028 scenarios.

We designed this report as a decision-support tool: it translates market dynamics into quantified strategic choices and tactical implementation checklists. The executive summary you’re reading now showcases the type of insight contained in the full deliverable; if your objective is to convert market intelligence into prioritized, executable initiatives for 2026, the full report contains the granular segmentation, supplier-level forecasting, and scenario-specific financials required for commitment.

To preserve the highest commercial value for subscribing clients, this public preview intentionally omits the proprietary micro-segmentation that drives investment and procurement decisions—specific regional and application-level revenue splits, SKU-level forecasted volumes, and our price-path scenarios for individual product types. These data are included in the full report and in our interactive modeling suite, where PW Consulting clients can test “what-if” scenarios (e.g., sudden pigment restriction, energy price shock, or accelerated regulatory adoption) and see direct P&L and free-cash-flow impacts under multiple assumptions.

2026 will be a year in which market positioning and execution quality determine winners and laggards. Whether your priority is protecting margins, accelerating a sustainability roadmap, or pursuing inorganic growth, PW Consulting’s Worldwide Specialty Ink Market report provides the evidence-based frameworks and scenario-tested recommendations needed to act confidently. For executive teams preparing budgets, negotiating supplier agreements, or sizing acquisition targets this year, the full report is an indispensable input to your deliberations.

Contact PW Consulting to access the complete report and the interactive forecast model, and to arrange a bespoke briefing that maps our findings directly onto your portfolio and strategic priorities.

For detailed analysis of this topic, please visit the official page:Worldwide Specialty Ink Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com