Top Local Business Listing Sites to Maximize Your Local Visibility

Other |

2026-07-14 07:29:20

PW Consulting’s latest market research — the Worldwide Rhodium(III) Iodide Market Report (base year 2025, forecast 2026–2032) — provides a rigorous, commercially focused lens into a niche but strategically crucial segment of the precious-group metals chemicals landscape. As we enter 2026, companies that trade, manufacture, use or finance catalytic and specialty chemical supply chains face an environment shaped by acute raw-material tightness, concentrated supply, and accelerating end-market technical demand. This synthesis explains why our report is an essential planning tool for executives preparing budgets, sourcing strategies, and R&D roadmaps for 2026 and beyond.

Worldwide Rhodium(III) Iodide Market

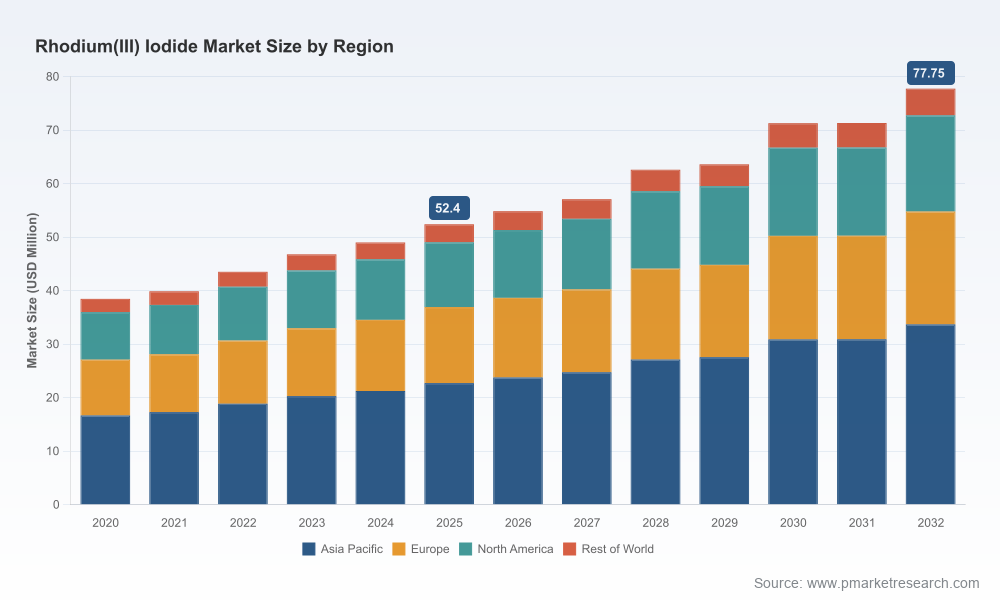

The Rhodium(III) iodide market has exhibited steady compound growth over the past half-decade and continues to expand through the forecast window. From a measured base in 2020, the market reached a substantive level by 2025 and is projected to continue growing at a compound annual growth rate of approximately 5.8% through 2032. The detailed time-series in our report converts that CAGR into actionable scenarios — a conservative, base and upside forecast — enabling procurement, treasury and strategy teams to stress-test capital plans against price and availability shocks.

Worldwide Rhodium(III) Iodide Market

Two simple inferences follow. First, the market is large enough that incremental shifts in demand (for example, from a single large downstream carbonylation plant or a new research program scaling to production) materially affect sourcing dynamics. Second, steady growth combined with price volatility in the underlying metal layer elevates the value of forward-looking supply strategies; buyers with early sight of mid-term demand curves will have a decisive negotiating edge.

Worldwide Rhodium(III) Iodide Market

Rhodium(III) iodide is not an isolated commodity — its economics are implicitly tied to the rhodium metal market and to the structure of PGM refining and recycling. In early 2026, market observations showed exceptionally high rhodium prices and continued volatility, reflecting tight primary mining supply and robust recovery from catalytic converters. Secondary sources — notably automotive catalyst recycling — currently account for a significant share of available rhodium supply, tempering but not eliminating systemic exposure to geopolitical or operational disruptions in primary production.

For commercial teams, the implications are clear: spot-price exposure for RhI3 raw material is elevated, and inventories that once lay dormant can become urgent strategic assets. Our report models multi-scenario raw-material trajectories and links them to product-level margin sensitivity; it also quantifies the breakpoints at which buyers should accelerate hedging or long-term contracting.

Rhodium compounds, including Rhodium(III) iodide, are subject to standard chemical safety and handling regimes. Importantly, certain safety data sheets list hazard classifications that require enhanced controls in handling and worker protection. These regulatory factors are not peripheral: they translate directly into capex and operating expenditure choices for anyone planning larger-scale use or production, from ventilation and containment investment to training, insurance and permitting timelines.

The market is concentrated at the supplier level — our competitive overlay indicates the top three producers capture the lion’s share of supply, with an even larger proportion controlled by the top five. For buyers, this concentration produces both risk and leverage: when a limited set of suppliers dominates, single-source disruptions can cascade through supply chains, but strategic partnerships and volume commitments can secure preferential access to constrained material.

The commercial universe for Rhodium(III) iodide combines specialty materials houses, legacy PGM refineries, and scientific reagent suppliers. Key players included in our competitive assessment are established global PGM integrators and a cohort of specialised chemical providers supplying both hydrated and anhydrous forms, in high-purity and nanoscale presentations for advanced applications. Our company-level dossiers profile:

For executives contemplating supplier selection, our benchmarking framework goes beyond price-per-kilogram. We analyze lifecycle costs, return-on-capex for supplier qualification, and the time-to-production metrics that determine whether a supplier can realistically support a rapid scale-up or complex qualification regimen.

Rhodium(III) iodide sits at the intersection of catalytic chemistry and advanced materials research. Its primary commercial gravity remains in catalytic processes where rhodium is used as an active center for high-value transformations; an expanding frontier is the use of fine-grade and nanoscale formulations in specialty synthesis and laboratory R&D.

Our report traces how incremental technical advances — in ligand design, supported homogeneous catalysts, and process integration — can multiply demand in pockets of the market. We do not disclose proprietary segment-level volumes in this summary, but the full report maps where technical substitution pressure may emerge and where first-mover advantages are available for licensors and catalyst formulators.

Executives reading this report should expect clear, executable guidance across five decision domains:

Each element in our playbook is supported by quantified thresholds and worksheets designed for rapid adaptation. These templates are particularly helpful for supply chain and finance teams that must translate scenario outputs into capital and working-capital requirements within tight budget cycles.

The full report includes:

These deliverables are built to be used directly in board packs, investment memos, and sourcing negotiations; they are deliberately practical rather than purely descriptive.

Three converging realities make timely access to our report especially valuable in 2026:

In short, the report is not a passive reference: it is a decision toolkit designed to be actionable in 2026 planning cycles.

This briefing is intended to demonstrate the depth and practical orientation of PW Consulting’s analysis while steering you to the full report for the granular inputs that operational teams require. The executive summary here outlines the strategic contours and the decision levers that matter for 2026. The complete report contains the granular forecast tables, supplier-level KPIs, and the interactive models you will need to operationalize these insights.

Contact PW Consulting to access the full Worldwide Rhodium(III) Iodide Market Report and the accompanying decision-support templates — we will provide the data and workshop support necessary to convert insight into a 2026 action plan.

For detailed analysis of this topic, please visit the official page:Worldwide Rhodium(III) Iodide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com