Worldwide Blood Thinning Drugs Market 2026: Strategic Imperatives from PW Consulting

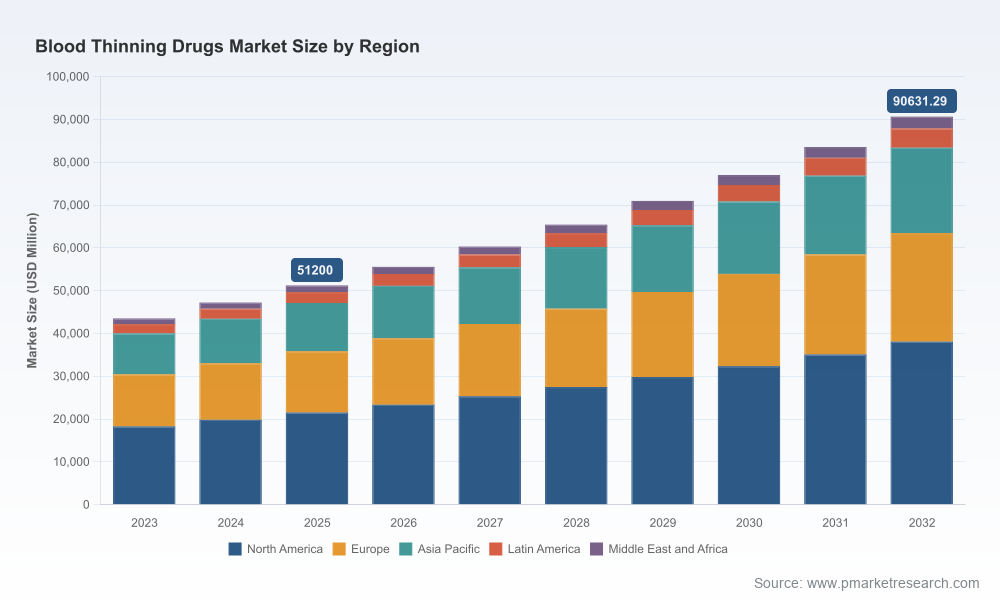

PW Consulting today publishes its new market intelligence briefing accompanying the Worldwide Blood Thinning Drugs Market report (base year 2025; forecast 2026–2032). Built on five years of historical analysis and forward-looking scenario modeling, the study shows the market continuing to expand at a compound annual growth rate (CAGR) of 8.5% through 2032, rising from an estimated USD 51,200 Million in 2025 toward a projected market size approaching USD 90,632 Million by 2032. For executives making decisions in 2026, the report is designed as an operational roadmap: it translates macro momentum into practical playbooks that preserve value through patent cliffs, regulatory shocks, and shifting clinical practice.

Worldwide Blood Thinning Drugs Market

Why this report matters for 2026 decisions

- Timing matters: 2026 will be a pivotal year across the anticoagulation value chain. Patent expiries and accelerating generic approvals change the rules of engagement for market incumbents and challengers alike. Our analysis converts calendar events into quantified risk and opportunity scenarios so leadership teams can prioritize actions with three- to twelve‑month execution horizons.

- Concentration and competitive dynamics: The market remains concentrated among a small number of global innovators and an increasingly capable cohort of generics and contract manufacturers. A high degree of concentration creates both barriers and focal points for regulatory, pricing and partnership strategies; the report lays out strategic levers that matter under both consolidated and fragmented outcomes.

- Regulatory and safety disruptions: Recent regulatory actions and product withdrawals are not one-off headlines; they re-shape clinical guidance, payer behavior, and stewardship protocols. Our scenario models embed the likelihood and impact of safety-related market adjustments, helping clinical affairs and market access teams prepare contingency responses.

- Supply-chain fragility: Manufacturing of heparin and low molecular weight heparins depends on biologically-sourced inputs. Supply continuity, vertical integration, and geopolitical sourcing risks are material to margins and access—areas covered in actionable mitigation frameworks within the report.

What’s inside the PW Consulting briefing (operational highlights)

- Robust top-down market sizing and trend decomposition (2020–2025 historical base; 2026–2032 forecast), including multiple growth scenarios calibrated to adoption curves, pricing erosion, and reimbursement shifts.

- Scenario playbooks tied to near-term triggers—patent expiries, generic approvals, safety withdrawals—quantifying revenue, margin, and volume impacts under conservative, base, and accelerated generic uptake cases.

- Competitive landscaping with strategic profiles of innovators, co-marketers, generics, and CDMOs—assessing defensive options, life‑cycle management, and M&A readiness for each player type.

- Product-level pricing and erosion models that support commercial planning and tender strategies without revealing proprietary split-level datapoints in this summary.

- Supply chain risk maps and mitigation templates focused on biologic raw materials, single-source dependencies, and manufacturing capacity constraints.

- Market access and reimbursement playbooks that translate clinical evidence and real‑world data (RWD) strategies into payer negotiation tactics.

- Practical M&A and partnership checklists aimed at buyers and sellers evaluating strategic bets in generics, specialty injectables, diagnostics and reversal agents.

- Primary interview insights and a validated patent-expiry calendar that connects IP events to commercial timelines.

Competitive landscape — implications for incumbents and challengers

The sector is shaped by a mix of global innovators, co-marketing alliances, and a rising tide of generics and specialty manufacturers. Leading originator firms maintain positional advantages via brand recognition, clinical trial portfolios, and integrated commercialization networks. Co-marketing arrangements remain strategically important where shared franchises extend reach.

Worldwide Blood Thinning Drugs Market

- Innovators: With major branded therapies continuing to command clinical preference in many settings, originators must accelerate life-cycle management—new formulations, indication expansions backed by RWD, and differentiated safety messaging—to blunt rapid generic substitution.

- Generics and CDMOs: Firms producing generic tablets and injectable anticoagulants face attractive volume opportunities, but must manage price competition, tender dynamics, and payer-driven formulary shifts. Scale and supply reliability will be differentiators in hospital and outpatient channels.

- Diagnostics and integrated care players: Diagnostic providers and companies offering perioperative and monitoring solutions can unlock ancillary revenue streams as clinicians seek safer anticoagulation pathways post-regulatory safety events.

- Reversal agent ecosystem: The regulatory removal of certain reversal agents and constraints on alternatives create care delivery gaps; companies with reversal strategies—whether pharmaceutical or procedural—will be evaluated for formulary inclusion and risk management contracts.

PW Consulting’s competitive profiles synthesize strategy, pipeline, manufacturing posture, and partnership options for each major player, enabling executives to map likely moves by competitors and anticipate countermeasures without exposing proprietary share estimates in this summary.

Worldwide Blood Thinning Drugs Market

Near-term triggers and recommended tactical responses for 2026

- Patent cliff playbook: With European exclusivity expiries and other IP events occurring in 2026, innovators should deploy a three-track response: 1) commercial defenses (pricing, loyalty programs, differentiated claims), 2) legal and regulatory readiness, and 3) accelerated lifecycle data generation to sustain premium positioning. The report offers decision trees and timing matrices for each option.

- Generic entry scenarios: Rapid generic approvals compress pricing and market share. We provide erosion curves and revenue-at-risk models so CFOs can stress-test budgets and prioritize investment in high-return defensive initiatives.

- Safety-related market shocks: Regulatory withdrawals and post-market safety findings alter clinical guidelines and payer coverage. The briefing includes communication templates, formulary negotiation scripts, and alternative care pathways to preserve continuity of care and market share.

- Supply continuity and raw material diversification: For heparin-based product manufacturers, diversification of biological raw material sources, inventory strategies, and regional manufacturing redundancy are presented as prioritized capital allocation choices.

Practical recommendations by stakeholder

- Originator pharma: Prioritize high-value real-world studies now; lock in hospital and specialty clinic contracts; consider selective licensing or authorized generic strategies where absolute defense is infeasible.

- Generics/CDMOs: Invest in capacity flexibility and quality systems; build direct relationships with large hospital systems and government tenders; pursue vertical integration where traceability of biological inputs is required.

- Payers and providers: Reassess formulary design in light of reversal agent availability and evolving safety signals; leverage value-based contracts tied to adherence and monitored outcomes.

- Investors: Focus on targets that combine manufacturing scale with regulatory know-how and supply-chain control; diagnostics and digital adherence platforms present asymmetric upside as adjuncts to pharmaceutical risk.

How PW Consulting’s models convert insight into action

The report’s forecasting engine integrates epidemiology, prescribing patterns, lifecycle event calendars, price erosion models, and supply-side constraints. Users can simulate scenarios—fast generic uptake, delayed regulatory action, or supply disruption—and produce P&L and cash-flow implications for product portfolios. The output is not just trend charts: it is executable timelines and prioritized initiatives, with clear owner roles and resource estimates for the most impactful moves in 2026.

Conclusion — a pragmatic intelligence offering for a decisive year

As the market grows toward the forecasted USD 90,632 Million horizon by 2032 at an 8.5% CAGR, 2026 stands out as a year when tactical agility will determine whether organizations capture upside or succumb to downside erosion. PW Consulting’s Worldwide Blood Thinning Drugs Market report equips decision-makers with the scenario-tested playbooks, commercial models, and competitive assessments required to act with speed and confidence. This briefing provides the strategic contours; the full report contains the granular segmentation, downloadable financial models, and executable checklists that operational teams need to convert plans into measurable outcomes.

For access to the complete dataset, regional and product-level forecasts, and our proprietary decision-support tools, please consult the full report and accompanying model package.

For detailed analysis of this topic, please visit the official page:Worldwide Blood Thinning Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com