The Foundational Power and Scope of the Global Event Stream Processing Industry

Other |

2026-06-25 06:12:50

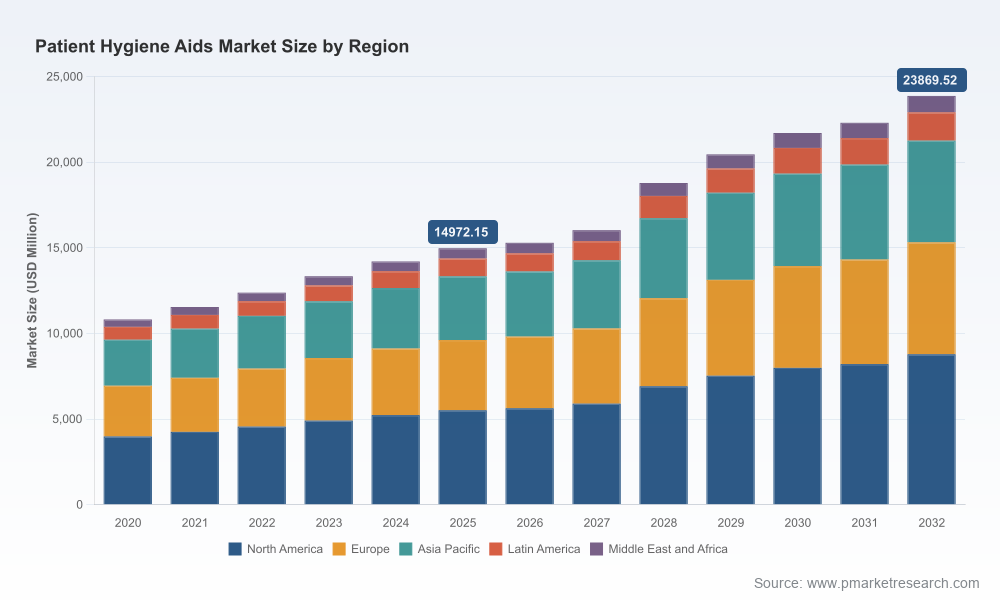

As healthcare systems adapt to tighter budgets, heightened infection‑prevention protocols, and shifting care delivery models, the Worldwide Patient Hygiene Aids market has become a strategic battleground for product innovation, procurement efficiency, and clinical outcomes. Our new market study (base year 2025; forecast 2026–2032) shows the market was valued at roughly USD 15.0 billion in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 6.89% through 2032, reaching an estimated USD 23.9 billion. For C-suite leaders, product managers, procurement heads, and investors planning 2026 moves, this report translates macro momentum into pragmatic, revenue‑and-risk oriented actions.

Worldwide Patient Hygiene Aids Market

Clinical and economic alignment: Patient hygiene aids are no longer a marginal consumable line — they are integral to infection prevention, pressure‑injury mitigation, and patient satisfaction metrics that influence reimbursements and reputation.

Worldwide Patient Hygiene Aids Market

Channel shifts and care settings: The rise of alternate care pathways and home‑based recovery increases demand for convenience‑oriented formats (e.g., no‑rinse washes, single‑use wipes), altering SKU priorities and distribution strategies.

Worldwide Patient Hygiene Aids Market

Regulatory and procurement headwinds: New device clearances and clarified regulatory expectations (notably for whole‑room UVC and similar hygiene adjuncts) are creating both barriers to entry and premiumization opportunities for compliant suppliers.

Consolidation pressure with room for innovation: The market shows meaningful concentration among established medical supply leaders, yet a broad set of mid‑tier and niche suppliers still capture a sizable share — creating an attractive M&A and partnership landscape for 2026.

This study is structured to convert market data into operational decisions. It includes:

Market sizing and trend maps: validated historical series (2020–2025) and scenario‑based forecasts for 2026–2032, integrating demand drivers such as aging demographics, acute care throughput, and long‑term care utilization.

Actionable segmentation: product‑type, end‑user, and regional segmentation with buyer archetypes and tactical playbooks for channel entry and SKU rationalization (granular split tables and model workbooks are available in the full report).

Competitive intelligence: company profiles, capability heat maps, go‑to‑market assessment, and an M&A heatmap identifying likely targets and acquirers.

Regulatory and clinical pathways: a practical roadmap for product clearance (including implications of recent regulatory clarifications), clinical evidence requirements, and protocols to accelerate hospital adoption.

Procurement and contracting tools: templated negotiation levers, supplier scorecards, and a cost‑to‑serve calculator designed to preserve margin while meeting facility KPIs.

Supply chain resilience checklist: supplier segmentation by risk, recommendations for dual‑sourcing critical substrates, and scenario planning for raw material volatility.

The marketplace blends global medical distributors, diversified healthcare conglomerates, and specialist hygiene brands. Understanding the relative strengths and gaps of incumbents is critical for market entry, partnership, and defense strategies.

Medline Industries — With a broad institutional reach and a full portfolio of patient hygiene consumables, Medline is built to serve hospital and long‑term care procurement cycles. Their strength lies in distribution scale and integrated supply agreements, making them a go‑to partner for facilities seeking single‑vendor simplification. Competitors should anticipate aggressive contract bids and bundled service offerings when engaging large health systems.

Stryker Corporation (Sage brand) — Stryker’s clinical positioning emphasizes standardized cleansing systems and no‑rinse bath cloths engineered to reduce cross‑contamination risk. Their value proposition is clinical standardization and measurable skin‑integrity outcomes, which can command premium pricing where facilities prioritize quality metrics over unit cost.

3M Company — 3M contributes antiseptic and skin care adjuncts that integrate into infection prevention protocols. Their R&D and clinical trial expertise enable evidence‑led product introductions that appeal to infection control leadership and procurement committees focused on total cost of care.

BD (Becton, Dickinson and Company) — BD leverages its procedural and clinical footprint to cross‑sell hygiene consumables into facilities already buying disposables and skin prep products, creating sticky procurement relationships.

Paul Hartmann AG & Molnlycke Health Care — European specialists with strong clinical hygiene credentials. Their advantage is in tailored institutional solutions and expertise in incontinence and skin‑care product design that aligns with nursing workflows.

Kimberly‑Clark, Coloplast, Cardinal Health — These firms bring scale, established channels, and branded clinical hygiene lines that serve both acute and post‑acute settings. Their incumbency in hospital supply chains allows rapid roll‑out of new SKUs once clinical evidence and contracting are aligned.

Ecolab — Positioned at the intersection of environmental hygiene and patient cleansing, Ecolab’s strength is holistic hygiene solutions that combine environmental systems with patient‑facing products, appealing to infection prevention teams seeking integrated programs.

CleanLife Products (No‑Rinse) — A category specialist with focused innovations for bed‑bound patients. Smaller specialists like CleanLife represent acquisition targets for larger players seeking to accelerate entry into no‑rinse and sensitive‑skin segments.

Overall, market concentration is meaningful but leaves ample opportunity: leading players capture a substantial share collectively, yet the landscape remains open to differentiation through clinical evidence, bundled services, and channel specialization.

Regulatory clarity on adjunct hygiene technologies: Recent regulatory decisions requiring 510(k) clearance for whole‑room UVC devices underscore the need for compliant clinical validation and clear go‑to‑market plans for firms marketing disinfection adjuncts. Companies should budget for regulatory timelines and early clinical endpoints to de‑risk adoption cycles.

Product standards for no‑rinse formats: Rinse‑free bath cloths and no‑rinse washes are now routinely formulated to meet dermatologist testing, hypoallergenic and pH‑balanced claims. Manufacturers without validated skin‑safety data will face procurement scrutiny from clinical buyers.

Reimbursement environment: Patient hygiene consumables are typically bundled within facility operating budgets or DRG payments rather than reimbursed as discrete items. This means value propositions must focus on total cost of care, staff time savings, and clinical outcome improvements rather than per‑unit price alone.

Prioritize clinical evidence generation: Invest in short‑cycle clinical studies showing reductions in HAI incidence, skin breakdown, or nursing time. Evidence accelerates formulary acceptance and enables premium positioning.

Design procurement‑friendly bundles: Create bundled service offers (product + training + usage tracking) to align with facility KPIs and justify higher ASPs.

Prepare regulatory pathways now: For entrants in the adjunct hygiene space (e.g., UVC or whole‑room systems), initiate 510(k) strategies and pre‑submission meetings to avoid launch delays.

Rationalize SKUs and simplify procurement: Use our cost‑to‑serve model to identify high‑impact SKUs for standardization across systems to reduce inventory complexity and drive scale efficiencies.

Pursue targeted M&A and partnerships: Buyers looking to fast‑track access to no‑rinse or sensitive‑skin portfolios should prioritize category specialists with clinical validation and clean manufacturing footprints.

Strengthen home care channels: Develop patient‑centric packaging, digital education, and retail‑friendly SKUs to capture growth as more care shifts outside acute settings.

Insulate supply chains: Dual‑source critical substrates, build safety stocks for high‑use consumables, and evaluate regional manufacturing to mitigate logistics cost pressures.

Our report is structured to move organizations from insight to implementable tactics. In addition to the research deliverable, PW Consulting offers tailored workshops that deploy the report’s models into client systems — e.g., SKU rationalization pilots, tender response playbooks, and M&A target due diligence packages.

We intentionally keep detailed segmentation, company market shares, pricing matrices, and downloadable forecast workbooks behind the full report to ensure decision‑grade accuracy and confidentiality. This release provides the strategic line‑of‑sight you need; the detailed, transaction‑ready models and appendices are available through the official report page.

If you are prioritizing procurement negotiations, product development, or M&A in 2026, start with a one‑week diagnostic using our hygiene‑aids playbook to identify 90‑day high‑impact moves.

To access the full dataset, granular segment tables, company scorecards, and our scenario modeling workbook, please visit the official report page or contact PW Consulting for a briefing and tailored engagement options.

Patient hygiene aids sit at the intersection of clinical necessity and procurement discipline. With the market on a steady growth trajectory and regulatory expectations crystallizing, companies that translate clinical evidence into procurement‑friendly commercial models will capture disproportionate share — and deliver measurable improvements in care quality. PW Consulting’s Worldwide Patient Hygiene Aids Market report equips leaders to make those choices with confidence in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Patient Hygiene Aids Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com