Worldwide Laser Direct Structuring (LDS) Grade Resin Market — Strategic Outlook for 2026 Decision-Makers

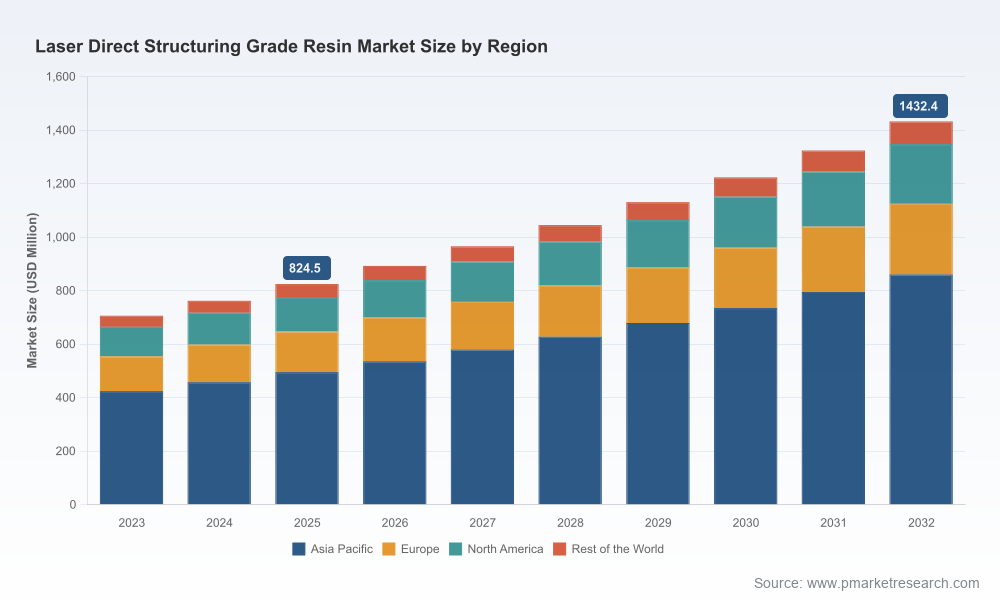

PW Consulting’s latest market research release offers a timely, practice-oriented briefing for executives and strategy teams active in molded interconnect devices (MID), 3D circuitry, and related verticals. With a 2025 base year and a detailed historical review (2020–2025) feeding a 2026–2032 forecast horizon, the report quantifies a market that continues to expand at a robust compound annual growth rate (CAGR) of 8.21%. Our market model—which reports in USD Million—places the industry on a clear growth trajectory from a mid-2020s base toward substantially higher absolute scale by the end of the forecast window. This bulletin summarizes the strategic value of the full report for decisions you must take in 2026 while intentionally withholding the granular proprietary splits reserved for subscribers and buyers of the full analysis.

Worldwide Laser Direct Structuring Grade Resin Market

Why 2026 Is a Pivotal Year for LDS Resin Strategy

Three converging dynamics make 2026 a turning point for companies exposed to LDS technologies: accelerating demand for compact, integrated antennas and interconnects in consumer electronics and 5G devices; stronger penetration of LDS-enabled components in automotive sensing and electrification architectures; and broadened material qualifications that expand the engineering envelope for high-performance applications. PW Consulting’s base-year synthesis and forward-looking scenarios show the market stepping into an expansionary phase, underpinned by consistent annual growth and rising commercial adoption across complex end-markets.

Worldwide Laser Direct Structuring Grade Resin Market

- Macro growth narrative: Our forecast model—anchored in comprehensive demand drivers and supply-side capacity assessments—projects sustained growth through 2032, with market size increasing materially from the 2025 base.

- Concentration and competitive structure: Market concentration indicators confirm a market led by a handful of established polymer and compound producers, producing both opportunities and competitive pressure for mid-tier innovators and regional players.

- Qualification-driven expansion: The role of LPKF and other process qualification frameworks is central—material approvals and certifications continue to be gatekeepers for automotive and medical-grade applications.

What the Report Delivers — Practical, Commercially Actionable Modules

PW Consulting’s full report is built for use, not just for reading. Key deliverables include:

Worldwide Laser Direct Structuring Grade Resin Market

- Transparent market sizing and a reproducible forecasting model (USD Million, 2026–2032) with scenario-based sensitivities to raw material price shocks and demand deltas in automotive and consumer electronics.

- Supply chain mapping and supplier risk heatmaps—covering polymer base resins, organometallic activation additives, and metallization service providers—enabling procurement teams to prioritize dual-sourcing and strategic inventory decisions.

- Technology & qualification dossier detailing LPKF approval pathways, material readiness levels for PEEK, PPS, LCP and other engineering resins, and practical guidelines for co-development projects with OEMs and toolmakers.

- Commercial playbooks for pricing, channel selection, and regional go-to-market strategies—useful for resin compounders, converters, and assembly houses scaling MID services.

- Competitive landscaping with company profiles, capability matrices, partnership maps, and M&A target screening criteria to accelerate inorganic growth due diligence.

- CapEx and process investment templates for manufacturers evaluating laser structuring lines, metallization baths, and post-processing quality systems tailored to MID production volumes.

To preserve the intelligence edge of the report, the publication intentionally excludes public disclosure of the detailed regional/application split table and line-item commercial figures from this summary. Those precise segment-level datapoints and our interactive model are reserved for licensed users.

Competitive Landscape — Who Matters and Why

The competitive picture is defined by established compounders, specialty resin suppliers, and progressive regional champions. PW Consulting’s strategic analysis focuses on capabilities that matter to customers and OEM partners—material performance in laser activation, plating adhesion, thermal/chemical resistance, and qualification history with leading laser equipment suppliers.

- RTP Company (United States) — Known for a broad LDS/MID compound portfolio including PC/ABS and reinforced PA grades tailored for plated MIDs. Their technical depth in compound development makes them a frequent partner for design-for-manufacture initiatives. (https://www.rtpcompany.com)

- Teijin Limited (Japan) — Offers low-dielectric PC grades optimized for LDS, which are relevant where signal integrity and plating deposition are critical. Their materials are often selected for demanding 3D circuitry implementations. (https://www.teijin-resin.com)

- Ensinger GmbH (Germany) — Supplier of high-performance PEEK LDS grades qualified for LPKF processes; their portfolio addresses MID applications requiring elevated thermal and chemical resilience. (https://www.ensingerplastics.com)

- Kingfa Sci. & Tech. Co., Ltd. (China) — A regional leader with an LDS series spanning PC/ABS and PC chemistries; Kingfa’s scale and product breadth support competitive pricing and local supply assurance in Asia. (https://www.kingfa.com)

- SABIC (Saudi Arabia) — Markets LDS-designed thermoplastic compounds focused on 3D-MID performance and activated surface metallization for antennas and interconnects. (https://www.sabic.com)

- DIC Corporation (Japan) — Recent material approvals expand their addressable market in automotive sensors; their PPS-based offering illustrates how new material qualifications are shifting the supplier landscape. (https://www.dic-global.com)

- Celanese Corporation (United States) — Known for high-performance LCP grades supporting intricate 3D circuitry—relevant in high-frequency and space-constrained designs. (https://www.celanese.com)

- Mitsubishi Engineering-Plastics (Japan) and LG Chem (South Korea) — Both provide LDS-compatible engineering plastics suited to automotive and electronics customers requiring integrated supply and local support. (https://www.m-ep.co.jp, https://www.lgchem.com)

Our competitive assessment emphasizes not only product fit but also supplier behaviors—lead times, qualification throughput, co-development willingness, and regional production footprint. Market concentration metrics show that the top three and top five players command a significant share of the market, which affects pricing power, supplier selection strategies, and the feasibility of long-term exclusive partnerships.

Regulatory & Technology Dynamics Shaping 2026 Choices

Two non-negotiable dynamics must be integrated into any 2026 strategy involving LDS resins:

- Qualification governance: LPKF and equivalent process approvals remain the industry’s de facto quality gates. Materials that secure those approvals accelerate OEM acceptance; conversely, the lack of qualification can materially delay product launches in regulated sectors such as automotive and medical devices.

- Materials innovation and supplier certification: Recent approvals of new PPS grades and expanded qualification of high-performance PEEK and LCP variants materially alter the technology map. This widens the material choice set while simultaneously raising requirements for thermal, chemical and plating reliability in end applications.

From a procurement and R&D standpoint, these dynamics translate into concrete imperatives: build qualification roadmaps aligned with key OEM timelines, preserve design flexibility by qualifying multiple material families, and create decision frameworks that balance initial material cost versus lifecycle performance and certification time.

How Leaders Should Use This Report in 2026

Executives, product leaders, and corporate development teams will extract immediate operational value from PW Consulting’s report in several ways:

- Prioritize R&D investments: Use our material readiness and qualification timelines to decide which chemistries to co-develop, and to allocate engineering resources to projects with the fastest commercial payback.

- Align procurement & supply resilience: Leverage our supplier risk maps to implement dual-sourcing, negotiate strategic offtake agreements, or invest in regional manufacturing capacity to reduce lead-time exposure.

- Commercial & pricing strategy: Calibrate pricing models using our demand scenarios and concentration insights to defend margins in contracting and to identify windows for premiumization tied to certified high-performance grades.

- M&A and partnership screening: Apply our capability matrices and acquisition candidate criteria to prioritize targets that fill portfolio gaps (e.g., specialized LCP or PPS expertise, localized compounding capacity, or plated MID service capabilities).

- CapEx decision support: Use our process investment templates to decide whether to scale in-house laser structuring capacity, enter into JV arrangements with service providers, or subcontract to specialist MID houses.

Recent Signals & Near-Term Triggers

Industry signals through late 2025 and early 2026 underscore accelerating commercialization and supply-side diversification. New product offerings targeted at automotive parts and high-volume manufacturing, along with LPKF approvals for alternate polymer families, are immediate triggers that will reshape procurement options and product roadmaps in 2026. PW Consulting’s report catalogs these developments and models their likely impact across multiple scenarios.

Next Steps — Where to Find the Full Intelligence

This executive briefing is a directional synthesis intended to inform board-level and operational decisions in 2026. The full PW Consulting report contains the proprietary segment-level datasets, interactive forecasting tools, and supplier scorecards that underpin the strategic recommendations summarized here. For teams preparing 2026 budgets, R&D plans, or M&A pipelines, access to those granular data and models is essential.

Contact PW Consulting or visit our report page to license the complete Worldwide Laser Direct Structuring Grade Resin Market study, obtain tailored briefings for your executive team, or commission a custom scenario analysis calibrated to your specific portfolio and regional exposure. The granular market splits, supplier-ranking matrices, and downloadable forecast model will enable you to convert the directional insights above into executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Worldwide Laser Direct Structuring Grade Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com