Why Accreditation Matters for Judo Schools

Other |

2026-03-24 13:27:23

As legacy vehicle repair models collide with the accelerating complexity of modern automotive architectures, corporate leaders face a simple fact: 2026 is the inflection year for translating capital, capability, and partnerships into defensible growth. PW Consulting’s latest Worldwide Car Body Repair Market study — anchored on a 2025 base year and projecting through 2032 — frames that inflection. The global market, approximately USD 206,020 Million in 2025, is forecast to expand at a compound annual growth rate (CAGR) of 3.55% through 2032, reaching roughly USD 263,010 Million under a central scenario. This report is designed to convert those macro signals into boardroom-ready choices for operators, suppliers, insurers, and investors.

Worldwide Car Body Repair Market

Vehicle complexity is increasing. The growing prevalence of high-strength steels, mixed-material structures (aluminum, composites), and electrified powertrains materially raises repair severity, tooling requirements, and technician training needs.

Worldwide Car Body Repair Market

Regulatory and OEM demands are tightening. EV-specific safety protocols (e.g., high-voltage isolation) and mandatory ADAS recalibration requirements are shifting certification and facility upgrade priorities for credible collision centers.

Worldwide Car Body Repair Market

Supply-side pressure is real. Refinish materials and paint inputs rose meaningfully in early 2025; labor cost and certification premiums are also creating margin pressure that makes operational efficiency a strategic imperative.

Digital and business-model disruption are accelerating. Mobile repairs, express/SMART programs, advanced diagnostics, and AI-assisted estimating are moving from “nice-to-have” to sources of sustainable competitive advantage.

Prioritize capability investments where repair complexity compounds cost: multi-material tooling, certified EV-safe workstations, and ADAS calibration suites. These are no longer boutique upgrades — they are minimum requirements for OEM-aligned volume work.

Design workforce strategies that balance higher hourly rates with productivity-enhancing technologies and modular skill ladders. In the U.S., for example, average hourly labor rates can range from roughly USD 120 to USD 160 depending on region and certification, making productivity an urgent focus.

Re-price and re-contract around materials inflation. Paints and materials saw price increases in early 2025; successful operators adopted dynamic surcharge mechanisms and supplier partnerships to protect margins.

Treat parts sourcing and right-to-repair developments as strategic levers. Evolving state-level laws and OEM repair mandates change the calculus on aftermarket vs. OEM parts and on investments in recycled-parts networks.

Use M&A selectively to secure capabilities and scale: acquisitions that add mobile services, regional market density, or specialized EV/ADAS expertise deliver faster ROI than bolt-on tuck-ins that only add footprint.

Actionable market sizing and forecasting model (2020–2032) with scenario toggles to stress-test EV adoption, materials inflation, and regulatory shifts.

Operator playbooks: capital planning templates for facility upgrades; productivity levers tied to technician certifications; and mobile vs. fixed-site ROI calculators.

Supplier and procurement playbook: cost-to-serve models, negotiation frameworks for refinish suppliers, and bundled procurement options that preserve quality while dampening input volatility.

M&A and partnership decision frameworks: strategic fit matrices, integration checklists, and a prioritized pipeline of target archetypes (mobile specialists, regional MSOs, parts recyclers).

Digital adoption roadmap: phased deployments for AI-assisted estimating, claims integrations, shop-floor automation, and customer-facing scheduling platforms designed to improve throughput and conversion.

Regulatory and certification tracker: a living annex of EV safety protocols, ADAS recalibration requirements, and right-to-repair changes that materially affect operational compliance and insurer relationships.

Benchmark dashboards and KPIs for revenue per bay, average repair cycle time, parts-turn, and certification mix — intended for immediate use in boardroom reviews and investor diligence.

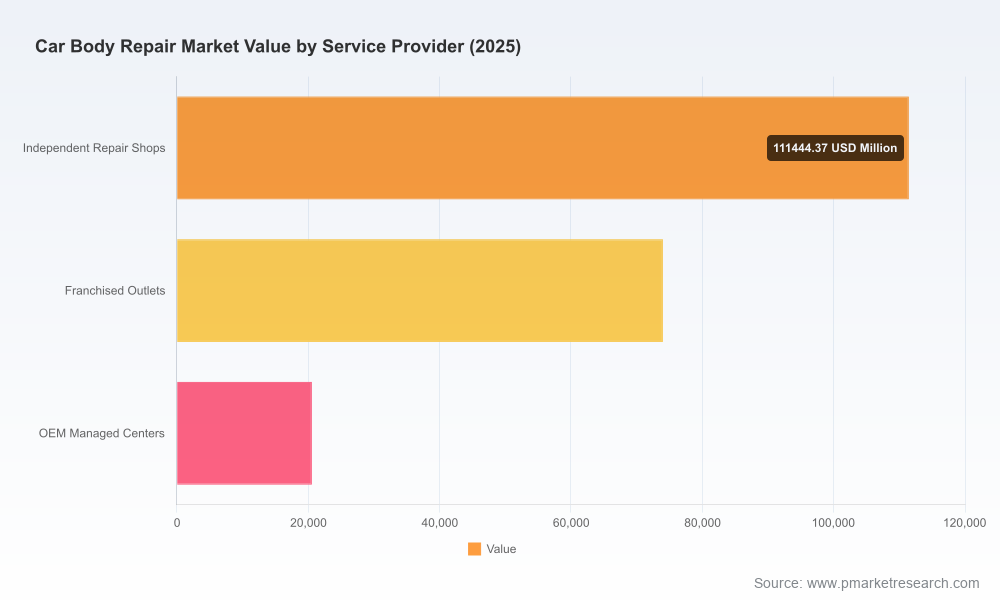

The competitive shape is a mosaic of scale-driven multi-shop operators (MSOs), specialized franchisors, global materials suppliers, parts distributors, and niche service providers. Key players illustrate the strategic vectors unfolding across the industry:

Caliber Collision — A capital- and acquisition-driven MSO model that is extending into mobile and fleet services. Its 2025 acquisition of a mobile provider signals a deliberate push into convenience-led service and off-site workstreams.

The Boyd Group Inc. (Gerber Collision & Glass) — Large-scale network operator with recent inorganic moves to expand capacity and leverage OEM certification as a differentiation mechanism. Their transactions underscore ongoing consolidation among MSOs.

Crash Champions and Classic Collision — Rapidly growing U.S. operators that emphasize ADAS calibration and advanced refinishing, demonstrating that technical differentiation can be as valuable as pure scale.

Fix Auto and CARSTAR — Franchise and network models that standardize quality and facilitate rapid roll-out of OEM-aligned protocols; franchisors are becoming preferred partners for insurers seeking consistency across claims volumes.

3M, PPG, Axalta, BASF, AkzoNobel — Global materials and coatings suppliers who control critical inputs and are simultaneously pursuing value-add services (color-matching technology, low-VOC systems) — making supplier relationships strategic, not transactional.

Dent Wizard and LKQ — Niche specialists: paintless dent repair and parts distribution respectively. Their roles in cost containment and parts availability are increasingly important in margin preservation strategies.

Recent market activity points to three converging trends: (1) MSO consolidation and capability acquisitions (notably mobile and fleet-oriented deals), (2) accelerated adoption of EV- and ADAS-focused certifications showcased at industry fora in 2026, and (3) supplier-driven price adjustments in refinish materials that are compressing short-term margins. Each trend has distinct strategic responses; our report maps those responses to executive timelines and investment thresholds.

Labor is both the largest operational cost and the hardest to scale. With U.S. hourly labor rates materially above historical norms and average collision job costs in the mid-thousands of dollars, step-change improvements in productivity yield outsized margin benefits.

Input inflation for paints and materials is not a one-off: early 2025 increases require renegotiated supplier terms, hedging where possible, and service redesigns that reduce refinish intensity when appropriate.

Regulation elevates compliance cost: OEM-mandated procedures for EVs and evolving right-to-repair rules create both risk and opportunity — shops that invest early in certification can win OEM-referred work and insurer preferred status.

Short-term (90–180 days): institute dynamic material surcharges, prioritize ADAS and EV certification for top-revenue locations, and deploy an estimating AI pilot to reduce cycle time variance.

Medium-term (6–12 months): convert a percentage of capacity to express/MOBILE offerings, solidify supplier contracts with volume discounts tied to quality metrics, and evaluate targeted acquisitions to fill technical capability gaps.

Long-term (12–36 months): redesign network footprints to cluster capabilities (EV centers, heavy-structure bays, express repair lanes), integrate digital claims workflows with major insurers, and establish continuous training academies to retain skilled labor.

The car body repair sector is no longer a low-margin, undifferentiated services market. It is an infrastructure play at the intersection of materials science, digital workflows, skilled labor economics, and regulatory compliance. PW Consulting’s Worldwide Car Body Repair Market study translates that convergence into executable roadmaps for 2026 and beyond: from immediate operational levers to multi-year capital strategies. This article offers a strategic preview — the full report contains the proprietary segmented datasets, company benchmarking matrices, scenario-modeled forecasts, and plug-and-play operational templates necessary to make high-confidence decisions in 2026.

For detailed segment breakdowns, provider-level benchmarking, downloadable toolkits, and the data model behind our GDP-linked scenarios, please access the complete report on the PW Consulting website.

For detailed analysis of this topic, please visit the official page:Worldwide Car Body Repair Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com