Worldwide Cooling Mattress Topper Market — Strategic Outlook for 2026 Decision‑Makers

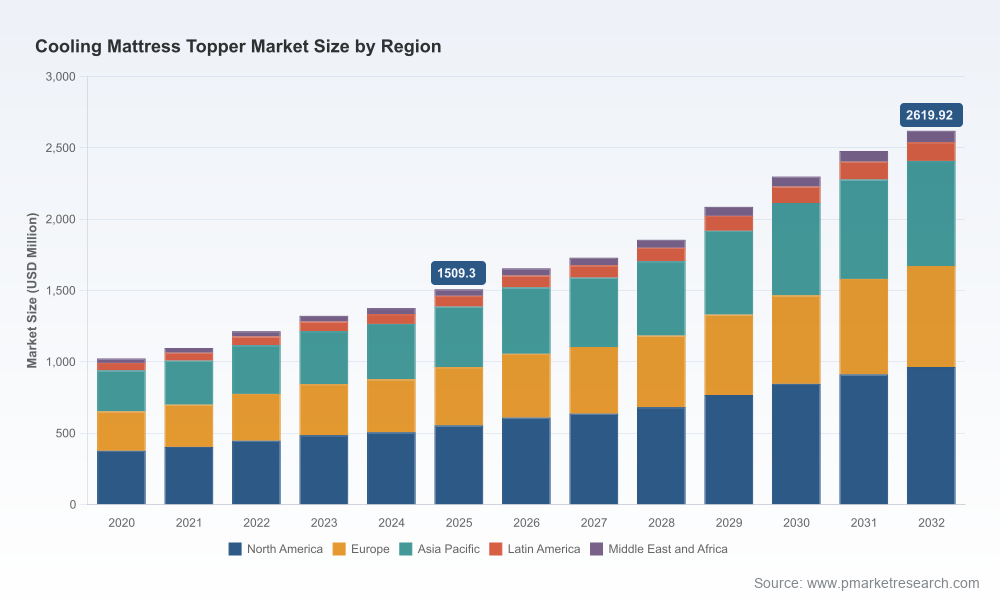

PW Consulting’s latest market study on the Worldwide Cooling Mattress Topper Market provides a decision‑ready synthesis for senior executives, product strategists, investors and M&A teams preparing for 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the analysis quantifies a clear expansion: the global market grew from roughly USD 1.02 billion in 2020 to USD 1.51 billion in 2025 and is projected to reach approximately USD 2.62 billion by 2032, reflecting a compound annual growth rate (CAGR) of 8.16%. These headline dynamics create a practical planning envelope for capex, portfolio prioritisation, channel investment and partnership strategies over the next 18 months.

Worldwide Cooling Mattress Topper Market

Why this report matters for 2026 decisions

- Translate growth into prioritized investments: which technologies, channels and product formats will deliver disproportionate returns in a market growing at ~8% annually.

- Mitigate execution risk: operational checklists and supplier risk maps to protect launch timelines from raw‑material and certification delays.

- Inform M&A and partnership playbooks: identify capability gaps that are best filled by acquisition versus in‑house development.

- Support commercial rollouts: go‑to‑market blueprints for D2C, wholesale and retail partners that align with evolving consumer purchase behaviours.

Market trajectory at a glance

The cooling mattress topper category has transitioned from a niche add‑on to a mainstream performance layer across household and hospitality channels. Our historical sizing shows steady adoption through 2020–2025, with revenue increasing from about USD 1.02 billion to USD 1.51 billion. The forecast projects continued acceleration through 2032, reaching approximately USD 2.62 billion — a trajectory driven by broader consumer focus on sleep quality, rising thermal comfort expectations, and incremental product innovation in both passive and active cooling technologies.

Worldwide Cooling Mattress Topper Market

Two structural features are particularly relevant to 2026 planning. First, the market remains fragmented (the three‑firm and five‑firm concentration ratios are low), which keeps strategic doors open for aggressive challengers and focused consolidators alike. Second, innovation is multi‑modal: incumbents advance passive cooling formulations (e.g., gel and phase‑change chemistries) while smaller specialists push hybrid and active systems that enable stronger differentiation.

Worldwide Cooling Mattress Topper Market

What the report delivers — practical, executable intelligence

- Primary demand model: a granular market sizing and forecast engine (2020–2032) with scenario switches for product adoption curves, channel mix shifts and price elasticity.

- Commercial playbooks: SKU rationalization frameworks, value‑tiering guidance, and channel launch templates tailored to D2C, specialty retail and mass channels.

- Product innovation matrix: technology evaluations (materials, thermal management approaches, active systems), relative cost curves, and IP/partnering roadmaps.

- Supply‑chain and supplier risk map: tier‑1 and tier‑2 supplier profiles, single‑sourcing exposure indices, and mitigation options for raw‑material volatility.

- Regulatory and certification tracker: compliance checklists (including common certifications) and a timeline for achieving market access across major jurisdictions.

- Competitive scanner and M&A pipeline: target archetypes, valuation benchmarks and integration playbooks for tuck‑ins and capability buys.

- Commercial KPI dashboards: unit economics, marketing ROI, and payback simulations for promotional and subscription models.

Competitive landscape — who to watch and how they are positioning

The category mixes established mattress brands, digitally native players and specialised cooling technology companies. Representative strategic profiles we include in the report:

- Tempur‑Pedic (Tempur Sealy International): leverages proprietary viscoelastic formulations and branded “cool‑to‑the‑touch” fabrics to defend premium shelf space.

- Saatva: positions premium natural and graphite‑enhanced memory foams to appeal to consumers seeking luxury materials with thermal benefits.

- Helix Sleep & Birch (by Helix): work across brand families to bring differentiated cover technologies and natural material credentials into the category.

- ViscoSoft, Brooklyn Bedding, Nolah and Bear Mattress: mid‑to‑premium players optimizing copper‑infusions and advanced fabrics for cost‑effective cooling performance.

- Eight Sleep, Sleep Number, Perfectly Snug and Sleepme (Chilipad): innovators in active cooling systems and app‑enabled temperature control — an adjacent layer of differentiation that raises switching costs when integrated with sleep ecosystems.

- Purple Innovation and Therapedic: leverage core platform technologies (e.g., grid systems, gel foams) to extend into cooling topper SKUs.

- Breescape: a recent entrant that highlights how agile product launches can re‑shape category expectations — their SS26 Cooling Topper is a 2026 example of targeted innovation designed for “hot sleepers.”

Collectively, these players illustrate two competing strategic archetypes: breadth by incumbents defending via brand and retail reach; and depth by specialists exploiting thermal technology or platform integration to lock in consumers. Our concentration metrics confirm the category’s fragmentation, underscoring opportunity for well‑executed consolidation and for focused challengers to capture niche loyalty.

Material, regulatory and consumer dynamics shaping 2026

- Technology stack convergence: gel‑infused foams and phase‑change materials remain foundational for passive heat dissipation; simultaneously, hybrid models and active water‑circulation systems advance premium differentiation.

- Certification as a commercial moat: emissions and safety credentials (for example, low‑VOC certifications commonly applied to foam products) are increasingly non‑negotiable for large retail partners and hospitality customers.

- Consumer behaviour: heightened awareness of sleep quality and temperature regulation is pushing consideration sets toward performance layers rather than purely comfort upgrades — translating into higher willingness to pay for proven thermal benefits.

- Supply pressures: raw material cycles (polymers, speciality cooling fabrics, PCM compounds) and logistics constraints will drive near‑term cost volatility; strategic procurement and supplier diversification are essential.

- Sustainability lens: natural and recyclable materials, traceability and longevity claims are gaining purchase with premium consumers and institutional buyers.

Actionable strategic recommendations for 2026

The following are high‑priority moves for organisations intent on converting the market tailwinds into durable advantage:

- Product portfolio: adopt a tiered approach — conserve margin in core passive SKUs while funding a single high‑impact active or hybrid innovation to capture early‑adopter premiums.

- Channel mix: accelerate direct digital channels with a data‑driven customer acquisition engine; use specialty retail partnerships to scale discovery and mass retailers for penetration pricing strategies.

- Certification and quality: fast‑track industry certifications and publish third‑party thermal performance data to shorten the trust curve with consumers and retailers.

- Supply resilience: implement dual‑sourcing for critical raw materials, lock strategic pricing collars where possible, and localise production for high‑growth end markets to reduce lead‑time risk.

- M&A and partnerships: prioritise bolt‑on targets that fill technology gaps (active cooling, smart controls), supply continuity or channel access; use earn‑outs tied to SKU adoption to align incentives.

- Commercial metrics: deploy unit economics dashboards that link customer acquisition cost, average order value and lifetime value specifically for topper buyers — treat toppers as gateway products into mattress ecosystems.

- Sustainability & circularity: adopt materials disclosure and take‑back programs for premium positioning and to meet growing retail requirements.

How PW Consulting’s tools accelerate your 2026 decisions

Beyond analysis, the report includes configurable Excel and dashboard models that allow teams to run bespoke scenarios: change price points, swap channel mixes, stress raw‑material prices, and simulate acquisition versus build decisions for new cooling technologies. We also provide a competitive heatmap, supplier risk scores and an M&A target short‑list framework calibrated to IRR and time‑to‑synergy thresholds. These deliverables are designed to be plug‑and‑play for board decks, investment memoranda and product roadmaps.

Next steps — turning insight into execution

For executives preparing budgets, revising product roadmaps or evaluating acquisition targets in 2026, this report functions as both a strategy playbook and an execution toolkit. It surfaces where to invest, where to defend, and where to partner — without overcommitting scarce R&D and market development resources. The full dataset, proprietary subsegment shares and the interactive forecast engine are available in the complete report; we intentionally withhold granular subsegment percentages in this summary to preserve the analytic core for subscribers and licensees.

Contact PW Consulting to request the full report, access sample deliverables, or schedule a briefing tailored to your product, channel or M&A agenda for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Cooling Mattress Topper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com