Worldwide Furniture Installation and Relocation Service Market: Strategic Outlook for 2026 — Executive Preview

Overview — why this report matters to 2026 decision-makers

PW Consulting today releases a strategic executive preview of our forthcoming market research report on the Worldwide Furniture Installation and Relocation Service Market. Built on a 2025 base, the market demonstrates resilient expansion — with our top-line modelling showing growth from a global market size in 2025 to a projected opportunity exceeding USD 2.4 billion by 2032 at a compounded annual growth rate (CAGR) of 5.45% over the 2026–2032 forecast window. For corporate real estate leaders, service providers, private equity investors and strategic acquirers, the 2026 planning horizon presents both an inflection point and a narrow window to act.

Worldwide Furniture Installation and Relocation Service Market

Why 2026 is pivotal

Three forces are converging as organizations update their 2026 plans: structural demand shifts, operating-cost pressure on labor-intensive execution, and an accelerating platform/technology substitution of traditional operational models.

Worldwide Furniture Installation and Relocation Service Market

- Demand signals: Hybrid work, continued retail remodel cycles and the emergence of flexible-lease models are driving persistent needs for professional installation, takedown and relocation services across both enterprise and consumer markets.

- Cost and labor dynamics: In major markets, hourly wages for installers and movers are a material component of unit economics — for example, average hourly pay in the U.S. was reported at approximately USD 18.50 in 2024 — and employment for furniture movers is projected to grow modestly, near 5% over the coming decade, constraining upside capacity without productivity improvements.

- Regulatory and safety overlays: Occupational safety standards (e.g., OSHA 1910.176 on safe handling and storage) and local independent-contractor regulations (notably legal frameworks similar to California’s AB5) are forcing platform operators and intermediaries to reassess labor models, cost pass-throughs and compliance investments.

What the PW Consulting report delivers — practical intelligence not available in this release

This preview is intentionally high-level. The full PW Consulting Worldwide Furniture Installation and Relocation Service Market report is structured to be immediately operational for 2026 planning cycles. Key deliverables include:

Worldwide Furniture Installation and Relocation Service Market

- Top-down and bottom-up market sizing and validated forecasting through 2032, with scenario analysis that stresses demand, wage inflation and regulatory shocks.

- Service-level economics: standardized unit-cost models for installation, relocation, and asset decommissioning that isolate labor, logistics, inventory and overhead drivers to quantify margin levers.

- Commercial playbooks for go-to-market and pricing for different service models (asset-light marketplace, asset-heavy rental-plus-installation, franchise-based moving networks).

- Technology adoption roadmaps: recommended investments in workforce enablement, last-mile orchestration, and customer self-service tools — including an ROI timeline for automation and telematics adoption.

- Risk and compliance matrix covering occupational safety requirements, contractor classification regimes, and cross-border labor considerations.

- M&A and partnership heat map highlighting target archetypes, integration playbooks, and value-creation levers for scale and specialization.

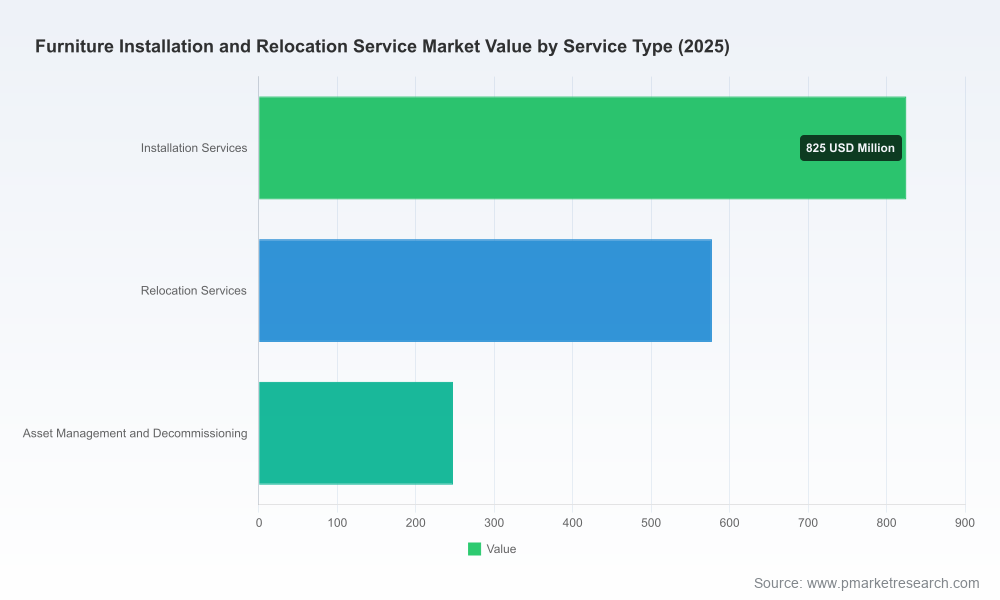

To preserve the strategic discovery experience for clients and readers, this press preview deliberately omits the granular regional, service-type and end-user splits that form the core of our proprietary modelling. Interested parties are invited to access the full dataset and interactive dashboards through our report portal.

Competitive landscape — platforms, franchise networks and rental-integrated players

The market remains fragmented: our concentration analysis shows low-to-moderate consolidation, with the combined share of the top three and top five providers indicating a broadly distributed supply base rather than dominance by a small handful. That structure creates both competition and opportunity for scale-minded players.

Seven archetypal players illustrate current strategic models shaping the sector:

- TaskRabbit (San Francisco) — a platform matching local Taskers to assembly and installation work; its strength is marketplace liquidity and flexible labor sourcing.

- Handy (New York) — an on-demand platform focused on urban centers with an emphasis on standardizing indoor installation tasks and consumer convenience.

- Thumbtack (San Francisco) — a marketplace emphasizing discovery and contractor matching for professional installers and movers across a broad set of local trades.

- Angi (Denver) — a directory and booking service with an emphasis on vetted contractors and lead-gen monetization for installation and relocation services.

- CORT (Chantilly) — an integrated rental and delivery provider that bundles furniture rental, delivery, installation and return logistics for corporate and residential clients.

- Two Men and a Truck (Atlanta) — a national mover with deep franchise footprint and standardized processes for disassembly/reassembly and white-glove moves.

- Bellhop (Nashville) — a tech-enabled moving provider focused on customer experience and urban last-mile optimization.

Across these models we observe several competitive vectors: (1) platform vs. asset ownership, (2) standardized SKU-like service offerings vs. bespoke enterprise projects, and (3) direct-to-consumer speed vs. enterprise contract stability. Each vector implies different margin profiles and capital requirements; our report maps these trade-offs to recommended strategic moves for 2026.

Actionable implications for four stakeholder groups

- Service provider executives: Prioritize a two-track strategy — optimize core dispatch and labor productivity now (immediate ROI), and selectively invest in platform capabilities that lock in enterprise accounts (longer-term differentiation). Revisit contractor classification and payroll strategies in light of local laws to avoid retroactive liabilities.

- Corporate real estate and facilities managers: Move from procurement-by-job to outcomes-based contracting. Aggregated service agreements that cover installation, modular reconfiguration and decommissioning reduce total cost of occupancy and speed remodel cycles; insist on telematics and SLA transparency to manage compliance risk.

- Investors and M&A teams: Target asset-light marketplaces with proven ability to scale unit economics, or asset-heavy providers with unique last-mile advantages in dense urban nodes. Value creation is most visible where digital underwriting, pricing engines and repeat enterprise revenues intersect.

- Public-sector and regulatory affairs teams: Prepare for higher enforcement of safety and labor classification rules; proactive compliance programs and traceable training records will lower audit risk and operational disruption.

Key risks and recommended mitigations

- Labor cost inflation and supply-side constraints — mitigate with productivity investments, blended labor models and predictive demand smoothing.

- Regulatory shifts (contractor classification and safety standards) — adopt compliance-first labor frameworks, centralize legal monitoring and model the financial impact of reclassification scenarios in 2026 budgets.

- Platform liability and reputational exposure — implement standardized training, digital sign-off workflows and insurance uplift clauses in B2B contracts.

- Technology displacement risk — pilots for telematics and augmented-assist tools should be staged with clear success criteria tied to time-per-job and first-time-right metrics.

Why PW Consulting’s method gives you an edge in 2026

Our analysis combines top-down macro drivers with bottom-up field validation. Primary interviews with operator executives, franchise owners and enterprise buyers, combined with unit-cost validation from sampled operations, underpin our forecast and scenario planning. We also stress-test outcomes against regulatory and wage-shock scenarios — the same scenarios senior leaders should be stress-testing in 2026 budgets.

Next steps — how to use this intelligence

For executives drafting 2026 strategies: use the report’s outcome-based contracting playbook to run a 90-day pilot that reallocates 10–20% of ad-hoc spend into consolidated service agreements. For investors, use our M&A heat map to prioritize due diligence on ARPU growth levers and churn rate reduction through platform features. Operational leaders should prioritize three quick wins from the report: a validated unit-cost baseline, a contractor compliance checklist, and a prioritized technology roadmap tied to measurable productivity KPIs.

Accessing the full report

This preview is designed to surface high-impact insights while preserving the detailed datasets and segment-level intelligence that corporate decision-makers and paying clients require. The full report contains the granular regional, service-type and end-user breakdowns, interactive forecasting tools, and downloadable financial models that are intentionally excluded from this release. To obtain the comprehensive report, schedule a briefing with PW Consulting’s industry practice team or visit our publications portal for licensing and single-report purchase options.

PW Consulting remains available for tailored briefings, scenario workshops and M&A diligence support to help executive teams convert these insights into executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Worldwide Furniture Installation and Relocation Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com