Global Fluorite Market Growing at 4.3% CAGR Through 2032

Other |

2026-06-24 12:41:35

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I am pleased to introduce our latest market research brief on the Pet Calming Food market — an increasingly strategic segment for petcare brands, ingredient suppliers, and retail channel operators. This executive overview highlights the practical, decision‑grade intelligence contained in our full report and explains why 2026 is a pivotal planning year for firms that want to convert category momentum into durable commercial advantage.

Pet Calming Food Market

The Pet Calming Food market has evolved from a niche supplement category into a mainstream part of many petcare portfolios. PW Consulting’s baseline assessment (base year 2025) quantifies the market at a notable scale, and our forecast models—built on historical performance from 2020–2025—project a sustained compound annual growth rate (CAGR) of approximately 7.95% across the 2026–2032 horizon. Under our central scenario, the market continues to expand meaningfully through the plan window, creating discrete opportunities for premiumization, channel innovation, and ingredient differentiation.

Pet Calming Food Market

For corporate strategy teams, this trajectory implies a dual mandate for 2026: (1) act quickly to capture share in high-growth niches, and (2) invest in capabilities—regulatory, manufacturing, and clinical substantiation—that will protect value as the category becomes more competitive and more scrutinized by regulators and consumers alike.

Pet Calming Food Market

Every element of the report is designed to be implementable within a 12–18 month business planning cycle — from R&D brief to retail listing — and includes templates and KPIs to operationalize decisions at the business-unit level.

The market today is populated by a mix of multinational incumbents, purpose‑built brands, and new entrants that blend nutraceutical science with modern CPG playbooks. Concentration metrics suggest a moderately fragmented market: the top three players account for under one‑third of market share, and the top five approach but do not exceed a plurality threshold. This structure creates tactical room for challenger brands to scale rapidly while presenting incumbents with opportunities to consolidate through product extension and acquisition.

Recent activity—new product launches and retail rollouts—shows both incumbent and challenger strategies in play: agility in product innovation from smaller brands, and scaled distribution moves from larger firms. Firms that can combine clinical validation with rapid retail penetration will have an edge.

Regulatory clarity and documented quality are accelerating from niche preference to mainstream purchase drivers. In the U.S., pet supplements are generally regulated as food under AAFCO and FDA guidance, which constrains disease‑treatment claims and elevates labeling precision. At the same time, third‑party quality signals—such as the NASC Quality Seal—are increasingly valuable for both consumer trust and retail acceptance.

2025–2026 industry events illustrate the stakes: voluntary recalls and contamination incidents have real commercial costs and can shift retail listing dynamics overnight. Brands must therefore prioritize supplier audits, lot‑level traceability, and clear adverse‑event protocols as core risk mitigation investments.

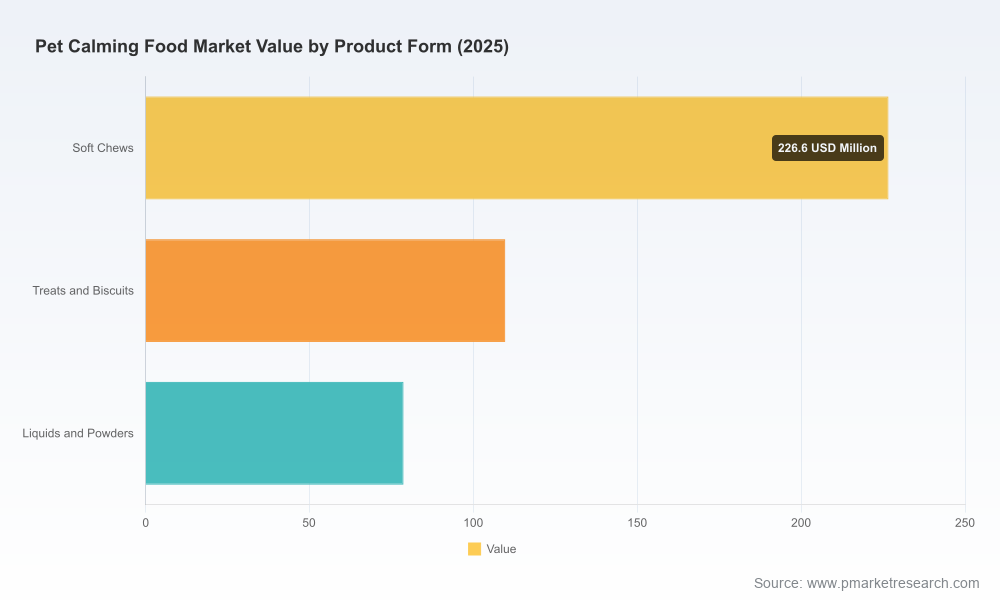

Product innovation in 2026 will cluster around three axes: ingredient differentiation (e.g., L‑theanine, L‑tryptophan, branded adaptogens), delivery format (soft chews, treats, liquids/powders), and species‑specific dosing. Consumer acceptance favors formats that simplify administration, and the intersection of palatability and scientifically supported ingredients will determine conversion and repeat purchase.

Raw material dependencies — for both botanical extracts and specialty actives — introduce sourcing risk and margin sensitivity. Manufacturers that invest in long‑term supplier partnerships, contract manufacturing flexibility, and ingredient validation will be positioned to sustain premium pricing as the market matures.

The fastest paths to scale differ by strategy:

Our report includes actionable decision trees for allocating SKUs across these channels, and breakpoint analyses that show when it makes sense to invest in exclusive SKUs, co‑branded clinic programs, or DTC subscription incentives.

Our full report provides the detailed market models, segmentation matrices, and tactical templates that corporate strategy, R&D, and commercial teams need to execute in 2026. To protect the proprietary value of our client work, this release intentionally omits granular segmentation figures and certain competitive line‑by‑line metrics; those details are exclusive to the full report and accompanying datasets.

If your leadership team is preparing a 2026 strategic plan, PW Consulting can support scenario modeling, M&A target diligence, go‑to‑market design, and clinical proof‑of‑concept programs that accelerate time‑to‑shelf. We also offer rapid workshops to translate the report’s evidence into 90‑day execution plans for product launches, retailer negotiations, and supply‑chain stabilization.

The Pet Calming Food market is no longer an experimental adjunct to pet nutrition — it is a strategic growth category that rewards scientific rigor, supply reliability, and channel fluency. Companies that combine those capabilities with consumer-centric product design in 2026 will not only capture share; they will define the standards of quality and trust that shape the category for the next decade.

For access to the full dataset, scenario outputs, and the complete strategic playbook, visit our official report page and request the executive package from PW Consulting.

For detailed analysis of this topic, please visit the official page:Pet Calming Food Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com