Worldwide SSD Memory Card Market — Strategic Briefing for 2026 Decisions

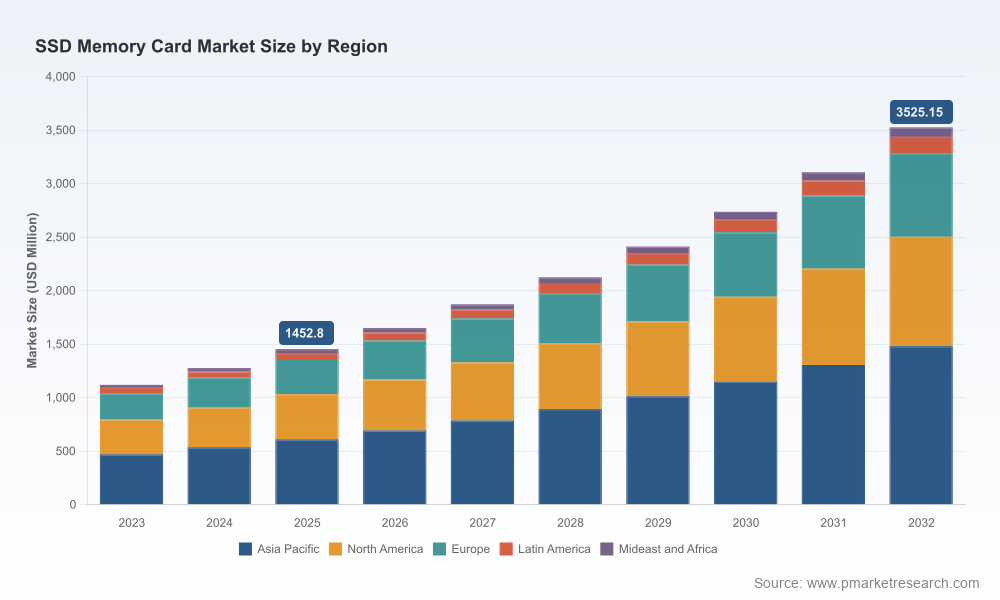

PW Consulting’s latest market study — the Worldwide SSD Memory Card Market (base year 2025; historical window 2020–2025; forecast 2026–2032) — provides a decision-grade synthesis for executives who must act during a period of accelerating demand, price volatility, and geopolitical friction. At the macro level the market scales from an estimated USD 1,452.8 Million in 2025 to an expected USD 3,525.15 Million by 2032, growing at a 13.52% CAGR over the forecast period. The 2026 inflection year is particularly decisive: our baseline projection for 2026 (USD 1,648.93 Million) captures the first full-year effects of AI-driven NAND reallocation, emerging removable-card standards, and strategic supply-chain localization efforts.

Worldwide SSD Memory Card Market

Why this report matters for 2026 strategic choices

- Time-compressed capital allocation: 2026 will require faster-than-normal decisions on fab capacity, long-term NAND commitments, and product prioritization due to short-term supply shocks.

- Procurement under volatility: NAND contract and wafer-price behavior in late 2025–early 2026 changes the economics of product SKUs and channel margins. Procurement frameworks must be rebuilt around hedging, indexed contracting, and capacity options.

- Technology and standard selection: Mainstreaming of high-performance removable standards alters product roadmaps and OEM go-to-market windows — firms that align early with platform owners capture premium placements.

- Regulatory and geopolitical contingency: Export controls and tariff risk are now first-order strategic variables for manufacturing footprint and partner selection.

Report contents — what executives will use the morning after

This study is intentionally practical. Beyond forecasting topline growth, it is organized to support executable decisions in 2026 with tools and outputs you can operationalize immediately:

Worldwide SSD Memory Card Market

- Proprietary market model (top-down & bottom-up hybrid) calibrated to 2020–2025 history and scenario-based forecasts to 2032 — available in modular form for client sensitivity testing.

- Driver decomposition showing how AI infrastructure demand, consumer refresh cycles, gaming device rollouts, and professional imaging workflows each contribute to addressable demand.

- Supply-side mapping that traces NAND sourcing, controller availability, assembly/test capacity, and key choke points across geographies — with supplier risk scores and time-to-recover estimates for common disruption scenarios.

- Commercial playbooks: product portfolio prioritization, channel segmentation, pricing levers, and launch timing techniques tuned for 2026 dynamics.

- Transaction-ready diligence packs for M&A, JV, and strategic investment — including valuation sensitivity to NAND-price spikes and regulatory shock scenarios.

- Operational guidance: inventory policies, contract templates (indexed and option-based), dual-sourcing blueprints, and a supply-insurance decision matrix.

- Competitive benchmarking and company profiles, plus a high-level concentration analysis (CR3 ≈ 58.4%; CR5 ≈ 76.5%), to inform partner selection and negotiation posture.

Competitive landscape — strategic implications for market participants

The market is a mix of vertically integrated memory manufacturers, controller specialists, and branded integrators. Our competitive chapter synthesizes publicly available profiles with proprietary channel intelligence to highlight how different archetypes should approach 2026:

Worldwide SSD Memory Card Market

- Integrated NAND/SSD leaders (examples include Samsung Electronics and SK hynix) are positioned to control unit economics via wafer ownership and internalized supply. Their near-term strategic moves focus on capacity allocation decisions that favor high-margin enterprise and AI workloads.

- Major memory houses with strong technology IP (examples include Micron and Kioxia) combine NAND roadmaps with targeted channel programs to protect professional and enterprise placements; their commercial tactics emphasize firmware and system-level differentiation.

- Branded storage players and distributors (examples include Western Digital / SanDisk, Kingston, ADATA, Transcend) compete on product breadth, channel reach, and customer trust. Recent developments underscore this dynamic: SanDisk disclosed a major product portfolio refresh and rebranding in early 2026, while standards bodies confirmed broader mainstream adoption of high-performance removable standards.

- Controller and firmware specialists (examples include Phison and Silicon Motion) are critical enablers: they are the leverage points smaller brands use to accelerate feature parity and time-to-market without deep NAND investments.

Collectively, the competitive environment favors firms that can combine technical differentiation (controller/firmware + durability + performance), secured NAND supply, and distribution agility.

Near-term headwinds and tailwinds to factor into 2026 planning

- Raw-material-driven margin stress: multiple industry datapoints from late 2025 indicate dramatic NAND price swings. Reports of steep wafer-cost increases for some suppliers and quarters showing 50%+ moves in contract pricing for NAND and enterprise SSDs mean cost pass-through and hedging need to be embedded in commercial agreements.

- Demand reallocation to AI/high-bandwidth compute: AI-related capacity demand has triggered short-term supply bottlenecks as wafer capacity is shifted toward HBM and high-layer NAND production, compressing supply available for removable storage products.

- Standards adoption and platform wins: confirmation that SD Express and related standards are becoming mainstream in certain gaming and consumer device segments accelerates the timetable for product qualification and OEM certification.

- Regulatory and trade risk: ongoing export controls on advanced equipment and the specter of tariffs have already pushed meaningful localization decisions. Firms must evaluate near-term reshoring vs. long-term cost trade-offs.

Tactical playbook for executives making 2026 choices

- Secure supply with layered contracting: combine short-term indexed purchases with long-term offtake and option contracts tied to capacity milestones to balance cost and availability.

- Prioritize product SKUs by margin volatility: protect high-margin, strategically important SKUs for enterprise and professional segments while rationalizing lower-margin consumer SKUs when NAND supply is constrained.

- Invest selectively in controller/firmware IP: owning or partnering for controller stacks reduces dependency on third-party windows and increases pricing power.

- Accelerate standards-aligned partnerships: joint engineering agreements with device OEMs that have adopted SD Express or CFexpress-related specifications secure placement and premium pricing.

- Implement scenario-based finance stress tests: run P&L and cash-flow models across NAND-price, tariff, and capacity-allocation scenarios to set trigger points for capex, pricing, and inventory moves.

- Design a dual-footprint manufacturing strategy: diversify assembly/test and packaging footprints to mitigate export-control and tariff exposure while evaluating cost offsets from localization incentives.

- Explore bolt-on and capability M&A: acquire controller expertise, firmware teams, or regional logistics assets to buy time and margin during supply-driven market tightness.

How PW Consulting supports your 2026 execution

We deploy a combination of market modeling, supplier diligence, and negotiation support tailored for storage-sector executives. Typical engagements for 2026 include:

- Custom scenario models that let procurement and finance teams stress-test portfolios against NAND price swings and capacity reallocation cases.

- Supplier risk audits and alternative-sourcing roadmaps designed to deliver “time-to-recover” improvements measurable in weeks.

- Commercial playbooks for product launches optimized for standards adoption cycles and OEM certification windows.

- M&A advisory for acquiring firmware/controller capabilities or regional manufacturing assets with integrated valuation adjustments for supply shocks and regulatory risk.

Our report provides the context and tools to convert market forecasts into executable 90‑, 180‑ and 360‑day plans. Because the competitive and policy environment is changing quickly, the full report includes the complete segmentation matrices, regional and application splits, detailed company-level revenue estimates, and downloadable model files — all gated on our report landing page to preserve the integrity and usability of the underlying datasets.

To learn how these insights apply to your portfolio or to commission a tailored scenario model for 2026, access the full report and contact options on our website.

— Senior Strategic Consultant & Chief Industry Analyst, PW Consulting

For detailed analysis of this topic, please visit the official page:Worldwide SSD Memory Card Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com