What Advances Are Strengthening the Pediatric Growth Hormone Deficiency Market?

Networking |

2026-07-03 08:46:44

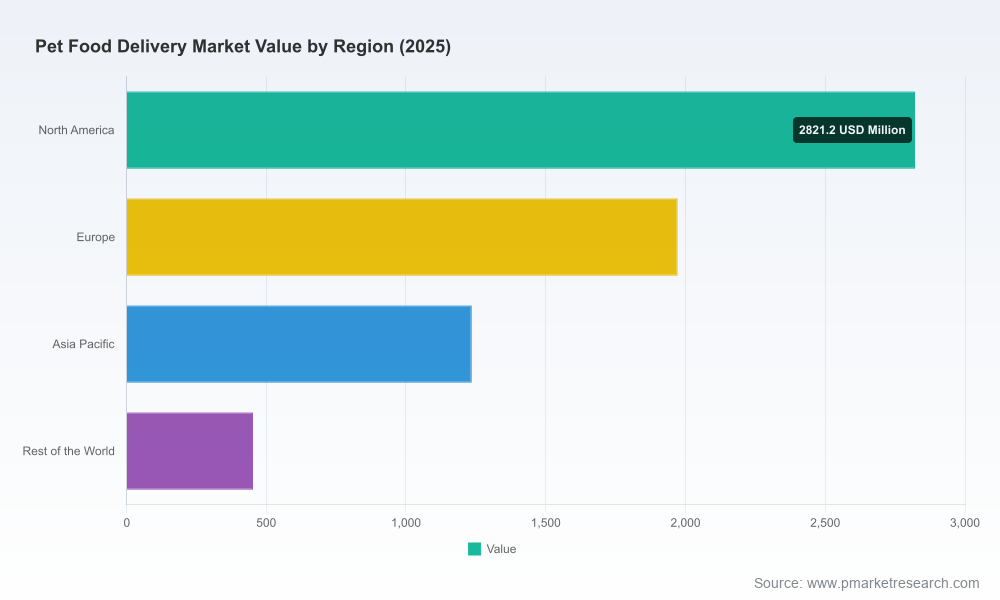

PW Consulting’s newly released market study—anchored on 2025 as the base year and projecting through 2032—translates the rapid evolution of pet food delivery into a set of concrete, high‑impact decisions that executives must take in 2026. The sector has more than doubled in scale over the past half‑decade and is set to continue expanding at a robust compound annual growth rate of approximately 10.51% through the forecast window. This report is designed as an operational playbook for leaders seeking to convert macro momentum into defensible commercial advantage—without exposing every granular datapoint in this summary.

Worldwide Pet Food Delivery Market

Acceleration from adoption to expectation: Consumer preference for convenience, recurring delivery, and tailored nutrition has shifted from early adoption to household expectation. Subscription models and same‑day fulfillment are becoming baseline service levels for premium segments.

Worldwide Pet Food Delivery Market

Channel conflation: Pure‑play DTC brands, legacy pet retailers, grocery‑delivery aggregators and marketplaces are each redefining how pet food is acquired. Winners will master hybrid models that combine brand differentiation with scale logistics.

Worldwide Pet Food Delivery Market

Fresh and premium nutrition is crossing an inflection point: Fresh, customized and refrigerated offerings are moving from niche to mainstream, forcing operators to grapple with cold‑chain investments, alternate packaging, and perishable logistics economics.

Regulatory and supply‑chain headwinds: Recent regulatory updates in major markets and elevated raw material cost signals mean 2026 planning must embed compliance and procurement strategies up front.

From the start of the decade to 2025 the market experienced sustained expansion, and our base/forecast modeling shows continuing robust growth into the early 2030s. At a projected CAGR of roughly 10.5% in the forecast period, the market offers durable runway for new entrants and incumbents that can achieve operational scale and margin discipline. For 2026 decision makers this implies a three‑part operational priority: accelerate recurring revenue levers (subscriptions and retention), invest selectively in fulfillment and cold‑chain capacity, and harden supply‑chain and pricing strategies against commodity volatility.

Labeling and nutritional compliance: Updated labeling requirements in major regulatory jurisdictions now extend explicitly to products sold through delivery channels; compliance is non‑negotiable and integrates into packaging, digital product pages and subscription communications.

Nutrient standards: Recent updates to national nutrient profile guidance require reformulation or additional lab validations for certain product categories; companies should budget for validation and potential reformulation cycles.

Raw material dynamics: Commodity inputs remain a source of margin pressure—recent market data shows corn and other bulk feed commodities at elevated but variable price points. Companies that do not embed procurement hedging, multi‑sourcing and value engineering will see margin erosion when consumer price elasticity is tested.

Trade and tariff exposure: Tariff regimes affecting cross‑border ingredient flows continue to shape sourcing economics; nearshoring and regional supplier development may be a strategic response for scale players.

The study is intentionally practical: beyond market sizing and a high‑level narrative, it provides the operational frameworks that strategy, commercial, supply‑chain and M&A teams will use in 2026. Highlights include:

Forecasting toolkit and scenario models calibrated to subscription penetration, fresh‑food adoption curves and fulfillment cost bands—designed to be plugged into commercial planning cycles.

Channel economics worksheets that map customer lifetime value to acquisition cost by channel (marketplace, DTC, retail pickup, grocery delivery), enabling payback and ROI optimization for 2026 CAC budgets.

Fulfillment and cold‑chain decision matrix showing the break‑even thresholds for regional refrigerated hubs, partner cold carriers, and in‑house delivery fleets.

Supplier risk and ingredient sourcing playbook including hedging options, quality assurance checkpoints, and a graded vendor‑diversification plan tailored to companies of different scale.

Regulatory compliance checklist and digital labeling guide that maps current regulatory requirements into product page, packaging and subscription communications tasks.

Go‑to‑market playbooks for four archetypes—incumbent omni‑retailers, pure‑play DTC brands, grocery/delivery aggregators, and consumer packaged goods firms entering direct channels—with prioritized tactical steps for the next 12 months.

Competitive intelligence dossiers and partnership scouting lists to accelerate M&A and JV diligence; the report synthesizes public moves and inferred strategic intent so buyers can act confidently.

The market is being actively reshaped by both large omnichannel retailers and specialist DTC operators. Our competitive analysis synthesizes recent developments and implied strategy for leaders and challengers.

Chewy—Established DTC retailer expanding into fresh and refrigerated delivery via strategic partnerships. This signals a broader pivot by high‑scale online specialists toward perishable categories and deeper partnerships with retail or venture units to solve last‑mile cold logistics.

Petco—Doubling down on subscription economics and service differentiation by expanding free‑delivery propositions for members, pressuring rivals on fulfillment cost and loyalty mechanics.

PetSmart—Leveraging brand and partner ecosystems to deliver fresh meal programs through autoship and select retailer collaborations, indicating that large retail chains will play offense with exclusive product assortments and logistics scale.

Instacart and grocery aggregators—Reinforcing the expectation of immediate replenishment; these players are most dangerous where pet food purchase frequency is highest, because they convert convenience into share of basket.

Amazon—Competing on speed and private label; for many players Amazon represents the pricing and logistics ceiling against which premium positioning must be measured.

Fresh DTC specialists (e.g., The Farmer’s Dog, Ollie, Nom Nom)—Investing in production capacity and direct relationships to own customer data and margins. Facility expansions by fresh‑food brands increase their ability to scale while preserving premium price points.

Map subscription economics to fulfillment tiers: build separate P&L arcs for dry, wet and fresh assortments and model logistics costs by service level (standard, same‑day, refrigerated).

Fast‑track packaging and compliance investments: label and digital metadata changes should be completed ahead of product rollouts to avoid time‑to‑market delays.

Invest in regional perishables capacity only where unit economics justify it; for most players, hybrid strategies combining contracted refrigerated carriers and micro‑fulfillment hubs will be optimal in 2026.

Embed procurement risk management: diversify ingredient suppliers, model commodity price pass‑through thresholds and establish hedging or forward‑buying programs where appropriate.

Push for retention as a primary growth lever: tighten subscription lifecycle orchestration (onboarding, personalization, churn flags) and integrate digital upsell/cross‑sell into monthly cadence.

Evaluate partnerships aggressively: retailers, meal‑kit operators and ready‑to‑scale pet brands are both customers and acquisition targets; partnership structures should prioritize data sharing and route‑to‑customer exclusivity where it creates durable advantage.

Our scenario toolbox offers three prioritized cases that should inform 2026 budgets and strategic options: a base case that assumes steady expansion in subscriptions and premiumization; an upside case where fresh and refrigerated adoption accelerates materially, compressing payback timelines for cold‑chain investments; and a downside case reflecting regulatory tightening or a commodity price shock—forcing temporary passthrough limits and margin contraction. Each scenario ties to discrete mitigation actions in procurement, pricing and capital allocation.

Executives who act early in 2026 will capture the dual opportunities of subscription lock‑in and category premiumization while the market structure remains sufficiently fragmented for bold moves to change competitive dynamics. PW Consulting’s study does more than map trends; it provides executable decision‑support tools—forecast models, channel P&Ls, supplier risk matrices and tactical playbooks—so that leadership teams can convert strategic intent into measurable outcomes during the 2026 budget year.

Senior executives: use the report’s scenario models to stress‑test 2026 revenue plans and supply‑chain investments.

Commercial teams: run the channel economics worksheets to reallocate marketing spend towards highest ROI acquisition and retention paths.

Operations and procurement: deploy the supplier risk playbook and evaluate cold‑chain options against eight pre‑defined economics thresholds in the report.

M&A teams: review the competitive dossiers and partnership candidate lists to accelerate diligences where scale or capability gaps exist.

This summary intentionally highlights the strategic contours and priority actions for 2026. For the full suite of models, detailed company profiles, granular regional and segment breakdowns, and downloadable decision‑support assets, visit PW Consulting’s report landing page and access the complete Worldwide Pet Food Delivery Market study—designed to be your operational guide through 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Pet Food Delivery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com