Enfeild Royal Clinic Guide to Everyday Aesthetic Confidence

Health |

2026-06-29 11:08:56

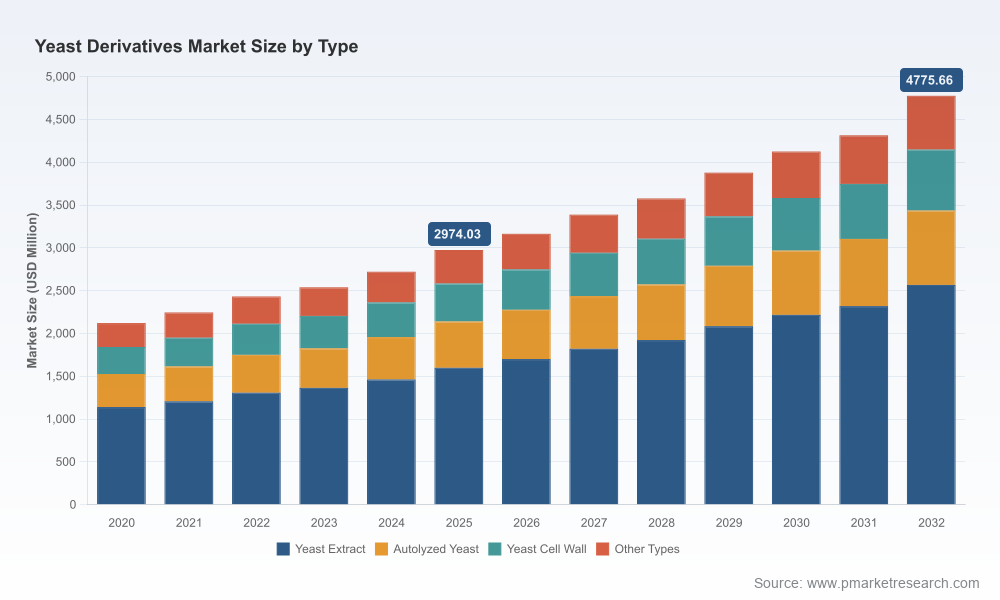

PW Consulting’s new market brief on the Worldwide Yeast Derivatives Market synthesizes proprietary modelling, primary interviews, and competitive intelligence into a concise decision toolkit for 2026. The sector has moved from a niche ingredient class to a supply chain focal point: global revenues rose from approximately USD 2.12 billion in 2020 to USD 2.97 billion in 2025 (base year), and our forecast model—built for corporate strategy teams—tracks a compound annual growth rate (CAGR) of 7.0% across 2026–2032, taking the market to roughly USD 4.78 billion by 2032. For executives weighing investments, M&A, capacity planning or procurement strategies in 2026, this brief highlights the levers that truly move value without disclosing the segment-level tables reserved for report subscribers.

Worldwide Yeast Derivatives Market

Timing: 2026 is the inflection point where premiumization of natural flavor solutions and the rising requirements of animal and human nutrition converge with a wave of capacity and ownership changes among leading producers.

Worldwide Yeast Derivatives Market

Risk vs. Opportunity: The market is growing steadily, yet exposure to feedstock volatility and evolving regulatory expectations means that commercial upside depends on operational and commercial agility.

Worldwide Yeast Derivatives Market

Actionability: The analysis is tailored to deliver immediately implementable actions—procurement hedges, M&A screeners, and production optimization playbooks—rather than high-level narrative alone.

Integrated market model: A calibrated, scenario‑driven forecast (2026–2032) with upside/downside pathways based on feedstock pricing, end‑market adoption rates and regulatory shifts.

Commercial due‑diligence kit: Buyer/seller scorecards, supply chain risk maps, and a standardised integration checklist for acquisitions in yeast-derived savory ingredients, specialty extracts and functional fractions.

Procurement & cost sensitivity tools: A molasses‑price shock model and cost pass‑through calculator to quantify margin exposure and identify hedging or vertical integration thresholds.

Go‑to‑market playbooks: Segmented strategies for brand owners, ingredient suppliers and contract manufacturers that align product positioning, pricing and regulatory documentation to buyer procurement cycles.

Competitive intelligence dossiers: Profiles and strategic scorecards for leading players, including capabilities, expansion plans and likely M&A ambitions—structured for quick executive readouts.

Demand drivers: Food and beverage manufacturers continue to pursue clean‑label, natural umami and savory solutions that reduce reliance on sodium and artificial enhancers. Concurrently, demand from animal nutrition and biotech/nutraceutical applications is supporting steady volume growth and premiumization of functional yeast fractions.

Supply constraints and feedstock sensitivity: Molasses remains the predominant upstream feedstock for large swathes of derivative production. Price and composition variability materially affect production cost and throughput: in Q3 2025, molasses prices in the United States reached approximately USD 295 per metric ton, and seasonal availability continues to create cost and operational variability.

Capacity and reshaping of supply: Strategic moves throughout 2024–2025, including acquisitions and greenfield capacity additions, have re‑balanced global supply in several product families. These actions heighten the importance of fit-for-purpose capacity planning when committing to long‑lead CAPEX in 2026.

Regulation and quality assurance: Yeast extracts maintain Generally Recognized as Safe (GRAS) status in the U.S., and Saccharomyces‑based products commonly operate under European Qualified Presumption of Safety (QPS) frameworks. However, compliance complexity—particularly for high‑purity extracts and novel functional fractions—requires investment in documentation and traceability to support cross‑border sales.

The market exhibits moderate concentration: the top three firms account for a significant share of global capacity, while the top five consolidate a larger but not dominant proportion—leaving room for regional specialists and technology‑focused challengers. Recent strategic moves illustrate the shape of competition:

Lesaffre: Continued inorganic growth to reinforce savory and specialty portfolios. Their acquisition of a controlling stake in an established savory ingredient business in mid‑2025 enhances downstream application reach and product breadth.

Angel Yeast: Aggressive scale and product innovation—new flavor variant launches and initiation of trial production at a large specialty plant signal a two‑pronged strategy of volume growth plus application‑led premium products.

Lallemand, ABF Ingredients (Ohly), DSM‑Firmenich and Kerry: These players combine deep application know‑how (flavor, nutrition, fermentation tech) with global distribution—positioned to capture value from formulation shifts by large food and beverage customers.

Mid‑sized specialists (Leiber, Alltech, Chr. Hansen, AB Mauri, Pakmaya): These firms hold technical advantages in specific niches—brewers’ yeast derivatives, animal nutrition, probiotic adjuncts—and are attractive targets for platform acquirers or for regional consolidation plays.

Acquisitions and consolidation have already reallocated meaningful capacity into fewer strategic owners, changing negotiation dynamics for large buyers and creating scale advantages in R&D and distribution.

Product innovations targeting natural flavors and differentiated sensory profiles reflect a shift from commodity supply to co‑development partnerships between ingredient suppliers and food formulators.

Capacity ramps and trial productions for specialty lines indicate that 2026 will be a year of commercialization: decisions made now on off‑take, co‑investment and channel alignment will determine whether new capacity achieves premium pricing or becomes volume‑driven.

Hedge feedstock exposure proactively: Adopt a tiered procurement strategy combining short‑term spot flexibility with mid‑term indexed contracts; model margin impacts under ±20–30% molasses swings using stress scenarios.

Prioritise capability‑led M&A: Target assets that bring differentiated functional fractions, proprietary processing know‑how or direct customer co‑development relationships rather than volume alone.

Fast‑track regulatory and QA readiness: For companies expanding into high‑purity extracts or novel end markets (nutraceuticals, pharma), allocate program funding to traceability, dossiers and targeted toxicology workstreams to accelerate market entry.

Commercialise premiumization: Develop value‑based pricing and application trials with key customers to capture formulation premiums, particularly where yeast derivatives replace less‑desirable additives or enable sodium reduction.

Invest in capability clustering: Co‑locate R&D with production and analytical labs where possible—this shortens product development cycles and reduces scale‑up risk for specialty fractions.

Prepare an integration playbook: If pursuing M&A, use a standardised checklist covering production harmonisation, regulatory transfer, customer retention clauses and feedstock contracts to reduce deal execution risk.

We built this brief as a strategic "first‑mile" asset for executives. The full PW Consulting Worldwide Yeast Derivatives Market report provides the granular inputs that operational teams require to turn strategy into cashflow: an interactive forecast model with downloadable scenarios, supplier scorecards and negotiation levers, an M&A target screening matrix, and a regulatory/QA map keyed to product families. Importantly, the full report also contains the segment‑level detail and regional breakdowns that corporate development and procurement teams will need for contract sizing and site selection.

For leaders evaluating commitments in 2026—whether that means capacity CAPEX, a bolt‑on acquisition, or a strategic supply agreement—this brief outlines the directional risks and opportunities. The complete dataset, financial models and client‑ready deliverables that underpin these conclusions are available in the full report on our website.

The yeast derivatives market is maturing from fragmented commodity supply to a more differentiated landscape where product innovation, regulatory readiness and supply chain resilience determine winners. With steady mid‑single‑digit growth at the market level and concentrated pockets of strategic scale, 2026 is a pivotal year for companies to decide whether to lead, follow, or niche. PW Consulting’s report equips decision‑makers with the scenarios, commercial tools and competitive insights necessary to pursue the right posture—and to convert market growth into sustainable margin expansion.

For detailed analysis of this topic, please visit the official page:Worldwide Yeast Derivatives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com