Robotic Arm market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-25 13:50:10

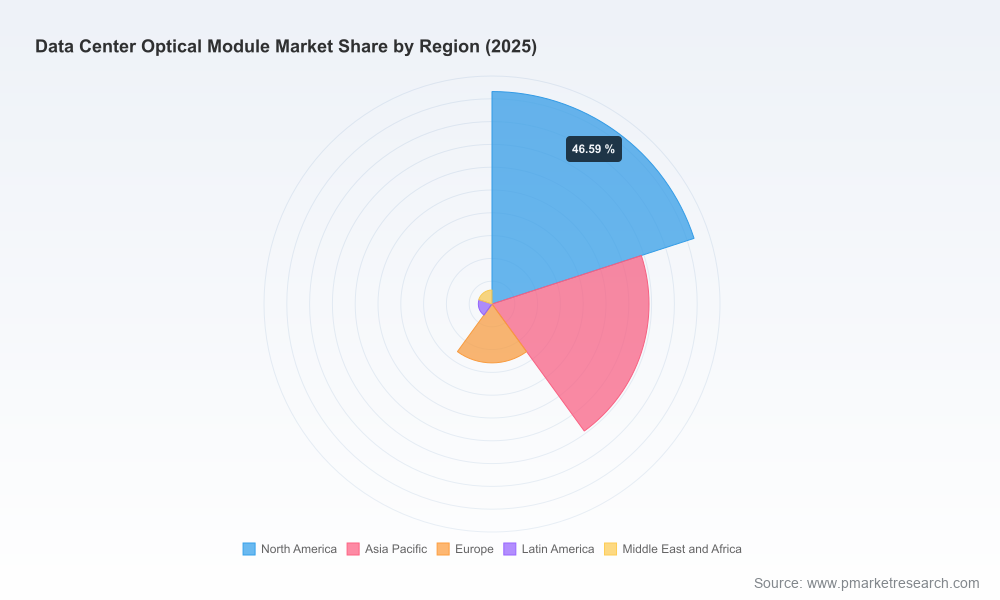

PW Consulting today publishes its latest market intelligence: the Worldwide Data Center Optical Module Market report, covering historical performance (2020–2025) and a detailed forecast for 2026–2032. The market has transitioned from a strong recovery phase into a sustained expansion driven by hyperscale cloud buildouts, AI training clusters, and next‑generation pluggable optics. Our analysis shows the market expanding from approximately USD 7.5 billion in 2020 to about USD 16.5 billion in 2025, with an expected compounding trajectory through the forecast window (2026–2032) at a compound annual growth rate (CAGR) of 16.48%. By 2032 the market opportunity is measured in the tens of billions of dollars — a scale that requires deliberate strategy from suppliers, buyers, and investors alike.

Worldwide Data Center Optical Module Market

Time‑sensitive capital allocation: With rising adoption of 800G and higher‑rate pluggables and the emergence of 1.6T class DSPs, procurement and fab investment decisions made in 2026 will disproportionately influence cost structure and time‑to‑market through 2028–2030.

Worldwide Data Center Optical Module Market

Supply‑chain resilience: Our primary research details chokepoints across photonics, substrates, and test capacity that can create multi‑quarter lead times. Organizations that front‑load diversification and contractual capacity agreements in 2026 stand to avoid premium rush pricing as adoption accelerates.

Worldwide Data Center Optical Module Market

Product roadmap alignment: The shift toward higher lane speeds, coherent pluggables for longer reach, and new form factors (to support PCIe 6.0 and denser AI interconnects) requires coordinated roadmaps across DSP, lasers, and module vendors. The report provides an actionable framework to prioritize engineering and interoperability investments.

Regulatory and sovereign risk mitigation: Trade controls and data‑sovereignty legislation are already influencing where and how infrastructure is procured. Decision‑makers need scenario playbooks for export‑restricted technologies and localized sourcing strategies — included in our scenario suite.

End‑to‑end market model: longitudinal sizing from 2020–2025 and a granular forecast for 2026–2032. The model is built to be stress‑tested under alternative scenarios (demand shocks, component constraints, energy cost shocks).

Technology roadmaps and readiness: assessment of pluggable interfaces, lane‑rate evolution, coherent pluggable adoption, and the timeline for 1.6T commercial sampling and ramp.

Supply‑chain heat map: supplier concentration, single‑sourcing risks, test and validation bottlenecks, and critical component lead‑time matrices with mitigation playbooks.

Vendor scorecards and go‑to‑market playbooks: comparative analysis of manufacturing scale, vertical integration, IP position, channel strength, and hyperscaler customer exposure — formatted for procurement negotiation and M&A due diligence.

Commercial scenarios and TCO (total cost of ownership) models: side‑by‑side cases for hyperscale, enterprise, and colocation deployments incorporating energy, real estate, and optical module spend.

Practical appendices: test method templates, RFQ checklists for long‑lead components, and recommended milestones for module qualification cycles.

The market is neither fully fragmented nor completely consolidated. Our concentration metrics show that the top three vendors account for roughly 48% of market revenue, while the top five capture around 64% — a structure that favors scale players but leaves room for well‑positioned challengers.

InnoLight Technology (Zhongji Innolight) — A high‑volume supplier focused on 400G/800G and beyond, with deep hyperscaler relationships. Strengths: rapid product ramp, tight supply agreements with cloud customers. Watch for margin resilience as volumes scale and for geographic customer diversification strategies.

Coherent Corp. (formerly II‑VI/Finisar) — Broad portfolio across datacom transceivers and photonic components. Strengths: component breadth and systems experience in coherent optics; strategic for customers seeking integrated supply and roadmap stability.

Lumentum — Offers both datacom transceivers and coherent pluggables. Strengths: manufacturing depth and component IP. Competitive edge lies in cross‑selling photonic subsystems to large OEMs and DCI providers.

Eoptolink & Accelink — Chinese vendors aggressively participating in 800G and higher segments, with strong cloud customer traction. Their growth dynamics are important for price and volume forecasts in the mid‑term.

Broadcom & Marvell — Semiconductor and DSP leaders that set the underpinning performance and integration for next‑gen modules. Marvell’s recent expansion of a 1.6T DSP portfolio signals an inflection toward higher per‑port bandwidth in pluggables.

Cisco, AOI, Sumitomo, Fujitsu, Hisense — Each plays a differentiated role across systems integration, hyperscaler supply, and regional market coverage. AOI’s recent large order activity highlights demand pull from hyperscalers for single‑mode 800G solutions.

Applied Optoelectronics (AOI) announced a sizable order for 800G single‑mode transceivers to support AI workloads. Implication: hyperscalers continue to accelerate upgrades on AI‑optimized interconnects — companies that can meet hyperscaler qualification cycles at scale will capture outsized share.

Marvell expanded its 1.6T optical DSP family with advanced process nodes. Implication: 1.6T pluggables are moving from R&D to sampling and early production; hardware vendors and carriers should prepare interoperability testing and procurement roadmaps now.

Kyocera and Semtech showcased form‑factor and analog front‑end advances (PCIe 6.0‑enabled modules, 224 Gbps/lane TIAs). Implication: incremental power efficiency and lane‑rate increases will influence rack‑level thermal design and module selection criteria.

Product launches from contract manufacturers signal competitive intensification at the high end; vendors that combine silicon‑software co‑design with manufacturing scale will define the next wave of cost/performance benchmarks.

Operational economics and policy are shaping procurement and deployment decisions. Electricity can represent roughly 40% of a large data center’s operating budget — an observation that changes the calculus on optics selection, since power/port directly translates to operating expense. Concurrently, utility companies in key markets are planning multi‑trillion dollar grid modernization programs to support data center electrification, while national regulators are rolling out export controls on advanced semiconductors relevant to AI training infrastructures.

From a demand perspective, U.S. data center electricity consumption reached levels that now command congressional attention, with projections showing a steep rise over the next few years. Data sovereignty laws and localization incentives are also redirecting buildouts and port sourcing decisions. The report includes scenario analyses that quantify the P&L impact of these factors and offers practical hedges for buyers and suppliers.

For hyperscalers: prioritize multi‑vendor qualification, align long‑lead commitments with roadmap ramps for 1.6T and coherent pluggables, and negotiate capacity guarantees tied to phased volume milestones.

For network OEMs and system integrators: accelerate DSP integration strategies, co‑develop thermal and validation suites with module suppliers, and protect time‑to‑market with prioritized engineering lanes for customers deploying AI clusters.

For component and chip suppliers: invest selectively in process nodes and packaging ecosystems that support the 1.6T migration, and explore supply agreements that offset single‑customer concentration risks.

For colo and enterprise buyers: adopt a staged upgrade path—balance immediate needs for higher density with longer‑term TCO sensitivity to energy and cooling costs; use our TCO templates to compare vendor offers.

This release highlights the strategic thrusts that will determine winners and losers between 2026 and 2032. PW Consulting’s full report contains the granular segment tables, vendor scorecards, region‑and‑protocol forecasts, and downloadable financial models that underpin the findings summarized here. To preserve the utility of that decision‑grade intelligence for subscribing executives, segmented percentages and vendor share tables are reserved for the full report and data workbook.

For procurement leaders, engineering heads, corporate development teams, and investors preparing decisions in 2026, the report is designed to be an operational tool — not just analysis. It includes executable RFQ templates, supplier‑risk playbooks, and scenario Monte Carlo outputs you can plug directly into capital planning cycles.

PW Consulting’s Worldwide Data Center Optical Module Market report is published with updates to our forecast and vendor assessments through April 2026. Contact PW Consulting to request a briefing, sample chapter, or to license the data workbook needed to inform your 2026 strategy.

For detailed analysis of this topic, please visit the official page:Worldwide Data Center Optical Module Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com