Foam Airplanes Boom: Fuel Savings Inspire Toy and Hobby Hits

Other |

2026-02-02 10:05:29

PW Consulting’s latest market research — the Worldwide Dry Electrostatic Precipitator (ESP) Market report, base year 2025 — delivers a concise, execution-oriented view of where the industry stands as firms plan capital, retrofit and MRO strategies in 2026. The market has expanded steadily from approximately USD 3.12 billion in 2020 to roughly USD 3.80 billion in 2025 and is forecast to grow at a compound annual growth rate of 4.12% across the 2026–2032 horizon. Our modelling projects continued momentum into the early 2030s before a moderate normalization of demand drivers toward the end of the forecast period.

Worldwide Dry Electrostatic Precipitator Market

This briefing is intentionally selective: it highlights the strategic implications and decision levers that corporate and project leaders must internalize for 2026, while preserving detailed segment-level tables and vendor scorecards for readers who access the full report.

Worldwide Dry Electrostatic Precipitator Market

Compliance-driven capex: Tightening emissions rules in mature markets and updated particulate standards are converting regulatory compliance into an immediate capital-program priority for power, cement and heavy industry operators.

Worldwide Dry Electrostatic Precipitator Market

Retrofit vs. greenfield calculus: A growing share of investments will be allocated to upgrades of existing precipitators rather than full replacement, changing supplier selection criteria and project timelines.

Supply-chain pressure points: Raw-material dynamics for critical components and component-level pricing volatility are reshaping procurement windows and contractor risk share.

Concentration and supplier strategy: The market exhibits mid-level concentration; a small group of global vendors capture a meaningful share of revenue, which influences negotiation dynamics, technology bundling and after-sales expectations.

From an investment perspective the most important takeaway is not simply that the market is growing — it is how growth and volatility are distributed across time and technology choices. The overall market value rose from approximately USD 3.12 billion in 2020 to about USD 3.80 billion in 2025. Our forecast shows an ascent through the late 2020s, with market values peaking in the early 2030s before a modest correction. With an expected CAGR of 4.12% for the 2026–2032 period, capital planners should expect steady, predictable demand for ESP equipment and services, but with pockets of accelerated activity tied to regulation-driven retrofit waves and commodity-driven component bottlenecks.

For procurement and treasury teams, the implication is twofold: align multi-year budget envelopes to a predictable growth baseline, and build flexible contracting to capture periods of accelerated spend when regulatory deadlines or plant modernization windows converge.

Regulatory momentum: Stringent emission limits in several jurisdictions are already pushing operators to targets that require high-efficiency particulate removal. Specific standards now require precipitators to reliably remove ultra-fine particulates to meet health-based benchmarks—this has immediate implications for the technical performance requirements of new ESP solutions, and for necessitating performance guarantees in supplier contracts.

Material and component pressures: The supply chain for high-voltage transformer cores and specialized electrode materials has tightened. For example, alloy shortages have driven meaningful price pressure on transformer cores, exerting upward pressure on lead times and capex assumptions. Buyers should assume that certain specialized materials will command premium pricing and limited availability in 2026 unless they secure committed supply.

Technology evolution: Vendors are differentiating through systems that reduce pressure drop, increase fine-particle capture and integrate digital monitoring for predictive maintenance. AI-assisted cleaning algorithms and integrated controls are transitioning from proof-of-concept to commercial offerings, changing the value proposition from capital equipment to ongoing service and performance optimization.

Operational priorities: Plant managers are prioritizing reliability and ease of maintenance. Solutions that minimize downtime during rapping/cleaning cycles, reduce inspection frequency and allow staged upgrades are seeing higher interest from operations teams faced with tight production schedules.

PW Consulting designed the report as a playbook for executives who must translate market intelligence into investment decisions. The full report includes (selectively summarized here):

Market sizing and modeled trajectories (2020–2032) with base-year consolidation and scenario variants for regulatory and commodity stress tests.

Regulatory impact matrices mapping emissions thresholds to likely retrofit waves and compliance timeframes across major jurisdictions.

Supply-chain risk heatmaps that identify critical component vulnerability and suggest mitigation options (sourcing strategies, inventory buffers, contract terms).

Vendor selection frameworks and a procurement checklist designed to de-risk technical and commercial performance guarantees, including recommended KPIs and warranty constructs.

Cost-to-own models and capex/opex comparison templates for retrofit versus replacement decisions, including sensitivity analyses for commodity price shocks and labor-cost variation.

Implementation roadmaps with prioritized actions for 12, 24 and 36-month horizons — covering technical audits, tender timing, financing structures and stakeholder alignment.

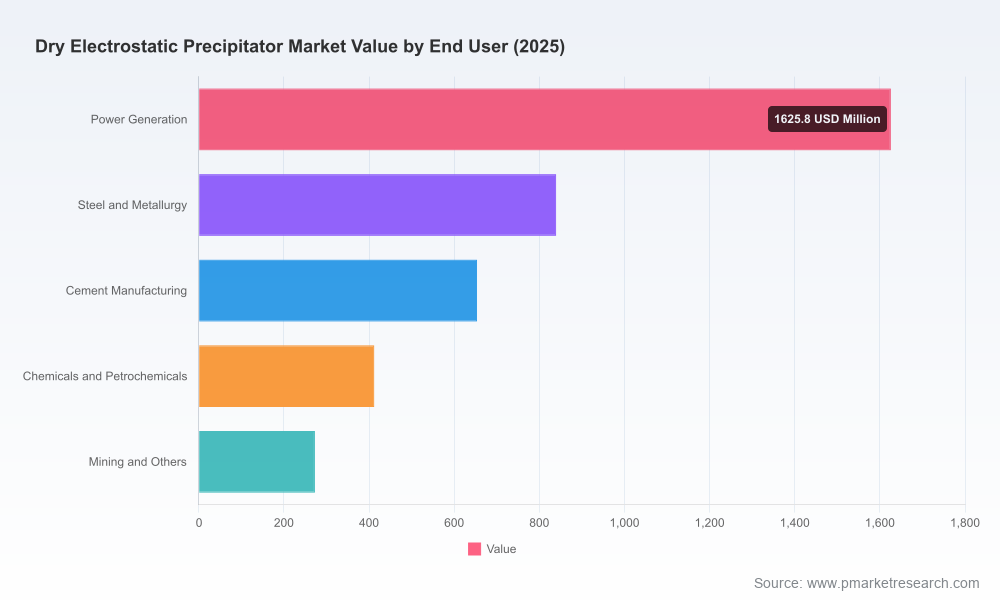

To preserve strategic value for report subscribers, detailed tables — including regional splits, end-user shares and configuration breakdowns — are provided only in the full dossier.

The industry shows moderate concentration: the largest three vendors hold a meaningful but not dominant share of the market, while the top five collectively control just under half of global revenues. This structure creates a supplier ecosystem where global primes coexist with highly specialized regional players. The competitive set we track includes established engineering leaders and manufacturers that combine process know-how with field-service networks. Notable vendors examined in the report include:

Babcock & Wilcox (USA) — modular dry ESPs for power and cement applications; strong field deployment experience and modular solutions tailored for PM compliance upgrades.

GE Power (General Electric) (USA) — systems targeted at boilers and waste-to-energy plants emphasizing low pressure drop and emission compliance across complex fuel mixes.

Hitachi Zosen (Japan) — solutions for steel and incineration contexts, focused on robust electrode design suited to harsh operating regimes.

Mitsubishi Heavy Industries (Japan) — advanced high-voltage solutions and transformers tuned for fine-particle capture in large-scale thermal plants.

Sumitomo Heavy Industries (Japan) — equipment for non-ferrous smelting and glass manufacturing with an emphasis on energy-efficient cleaning mechanisms.

FLSmidth (Denmark) — high-temperature and abrasion-resistant systems for cement and minerals processing; active in product innovation and digital service demonstrations.

Dürr AG (Germany) — compact precipitators for discrete industrial lines like automotive painting, with tight integration into process controls.

Recent vendor activity underscores a mixed pattern of project execution and product development: deliveries to cement and steel facilities remain strong, while trade-show debuts and award-winning contracts point to increasing product differentiation around digital controls and cleaning optimization.

Prioritize compliance windows: Identify facilities with impending emissions deadlines and sequence projects to reduce exposure to accelerated supplier lead times.

Lock in component supply where feasible: Negotiate multi-year supply or off-take agreements for critical materials and consider staged payments to secure capacity.

Adopt a hybrid procurement stance: Balance single-source relationships for integrated performance guarantees with competitive bids for commoditized elements to control costs.

Emphasize lifecycle value: Specify performance-based contracts that align vendor incentives with in-service particulate removal and energy consumption targets.

Invest in digital enablement: Prioritize systems with monitoring and predictive maintenance capabilities to reduce unplanned outages and O&M spend.

Prepare M&A and partnership playbooks: Companies seeking to scale service footprints or acquire niche tech should target vendors with complementary digital or field-service assets rather than purely equipment-led businesses.

The full PW Consulting report contains the models, vendor benchmarking matrices and procurement templates that strategic sourcing, plant engineering and finance teams need to execute in 2026. Subscribers gain access to downloadable tools including LCC models, compliance-scenario dashboards, and supplier negotiation playbooks that convert the market’s macro trajectory into executable project pipelines.

If your 2026 capital planning or compliance calendar includes ESP upgrades, retrofit projects or vendor selection, the intelligence in this report shortens the path from strategic intent to executed contracts while reducing downside risk from component scarcity and regulatory surprises.

For a full briefing, including the detailed segmentation, vendor scorecards and downloadable decision-support tools, access the complete Worldwide Dry Electrostatic Precipitator Market report via PW Consulting. The full report provides the granular tables and appendices required to finalize CAPEX submissions, tender packages and compliance roadmaps for 2026 execution.

For detailed analysis of this topic, please visit the official page:Worldwide Dry Electrostatic Precipitator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com