Worldwide Rod Capacitive Level Gauge Market — Strategic Outlook for 2026 Decision-Making

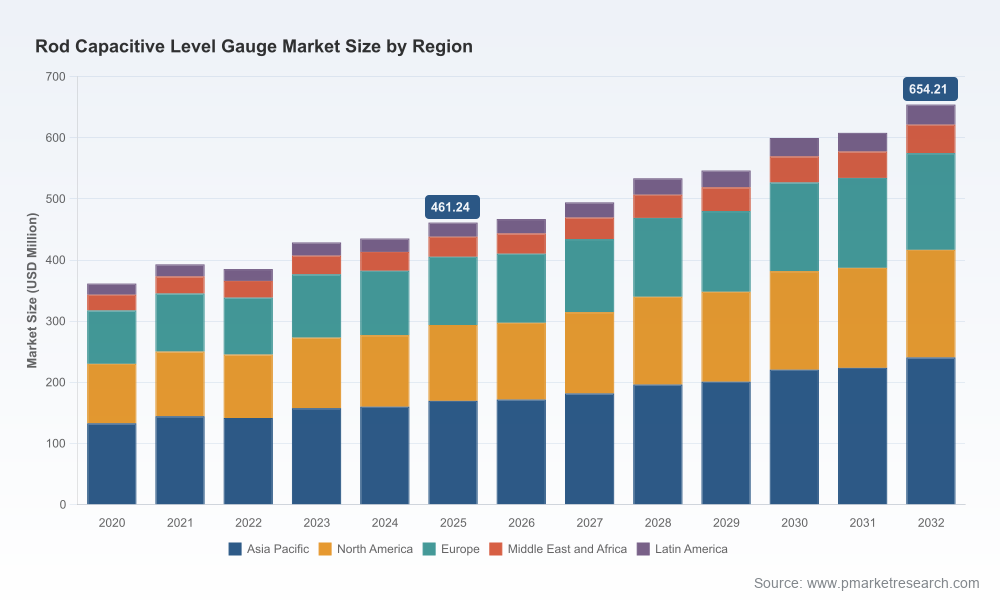

PW Consulting’s latest market research, "Worldwide Rod Capacitive Level Gauge Market," delivers a focused, actionable intelligence package designed to inform executive decisions in 2026. The market has shown steady recovery and expansion after mid-decade fluctuations; global revenues rose through 2020–2025 and the industry is projected to continue expanding at a compound annual growth rate (CAGR) of 5.12% through our forecast horizon. In monetary terms, the market reached approximately USD 461.24 Million in 2025 and is forecast to approach roughly USD 654.21 Million by 2032. These headline metrics are the starting point for a practical playbook that we synthesize below — enough to validate trends and strategic choices, while reserving granular segmentation and proprietary models for readers of the full report.

Worldwide Rod Capacitive Level Gauge Market

Why this report matters for 2026 strategic choices

- Timing: 2026 is the inflection year for procurement cycles across several capital-intensive end markets. Organizations finalizing mid-term budgets will need to reconcile capital discipline with urgency to modernize sensing assets.

- Signal vs. noise: Our analysis filters macro pressures (inflationary input costs, labor trends) and sector-specific dynamics (for example, hospital capex contraction and rising operating expenses in healthcare) into pragmatic implications for level-sensor vendors and buyers.

- Actionability: Beyond forecasting, the study maps vendor positioning, product differentiation, channel economics, and prioritized use cases that yield the fastest ROI for industrial and process applications.

Market trajectory and strategic implications

The rod capacitive level gauge market’s steady CAGR masks heterogeneous dynamics across materials, probe architectures, and service models. After a dip and recovery in the early 2020s, total market value expanded as industrial automation and process-instrument replacement cycles resumed. Our baseline shows a market approaching half a billion dollars in 2025, with measured expansion projected through 2032 driven by upgrades in processing facilities, retrofit demand, and continued adoption in both traditional heavy industries and adjacent sectors that are digitizing measurement points.

Worldwide Rod Capacitive Level Gauge Market

Strategically, three implications stand out for executives planning 2026 moves:

Worldwide Rod Capacitive Level Gauge Market

- Prioritize product modularity and materials engineering. Buyers are increasingly selecting solutions that minimize maintenance while extending mean time between failures (MTBF), particularly in corrosive or hygienic environments.

- Differentiate on services and total cost of ownership. As unit-price competition intensifies, bundled services (commissioning, digital calibration, remote diagnostics) and predictable service contracts become deciding factors for procurement committees.

- Balance geographic reach with channel resilience. While growth pockets persist, political-economic volatility and supply-chain constraints mean localized inventory and service capabilities can be decisive for mid-market accounts.

What the report contains — an operational syllabus for 2026

This report is designed as a practical decision-support tool for corporate strategy, commercial planning, and M&A scouting. Highlights include:

- Robust market-sizing and trend decomposition — historical performance (2020–2025), 2026 base-year calibration, and a seven-year forecast (2026–2032) under alternative scenarios.

- Adoption frameworks and buyer personas — granular profiles of procurement owners in process industries, food & beverage, pharmaceuticals, and water & wastewater, plus recommended messaging per persona.

- Technology and product matrix — comparative evaluation of probe types, insulation materials, electronics (analog vs. smart transmitters), and integration patterns with plant control systems.

- Commercial playbooks — pricing levers, channel models (direct, distributor, OEM partnerships), and contract structures that improve win rates for 2026 tenders.

- Supply-chain sensitivity analysis — critical component sourcing, lead-time scenarios, and mitigation strategies to protect revenue during upstream shocks.

- Regulatory and compliance checklists — hygiene standards, hazardous-area certifications, and documentation practices that shorten procurement cycles in regulated industries.

- Strategic M&A and partnership map — target archetypes, valuation benchmarks, and integration pitfalls for scale and capability acquisitions.

Note: The report deliberately omits publishing core segment-level numeric shares in this press release to preserve the report’s premium value. Readers seeking the full segmentation tables, regional breakout, and application-level revenue splits should consult the complete study.

Competitive landscape — practical takeaways for partnerships and procurement

Our vendor analysis profiles all major incumbents and fast-moving challengers, evaluating product portfolios, differentiation, and go-to-market models. A few strategic observations:

- VEGA Grieshaber KG (Schiltach, Germany) — Strength in engineered probe variants and material science. The VEGACAL series demonstrates how incremental material and insulation innovations (PTFE, PE, FEP, ceramic options) preserve accuracy in aggressive chemistries and bulk solids. Strategic implication: VEGA’s engineering-led positioning suits clients prioritizing durability and reduced maintenance cycles.

- Endress+Hauser (Reinach, Switzerland) — Combines robust instrumentation with integrated measurement solutions. Products like the Liquicap series emphasize interface and build-up tolerance, supported by a global service and calibration network. Strategic implication: Endress+Hauser remains the default choice for blue-chip process plants seeking single-vendor accountability for sensing and process analytics.

- Siemens AG (Munich, Germany) — Leverages active-shield and industrial-grade transmitter platforms to appeal to automation-heavy sites. Siemens’ integration strength with control systems and automation suites offers compelling upside for brownfield digitalization projects.

- KOBOLD Instruments — Niche supplier with flexible probe lengths and a strong focus on chemical and pharmaceutical segments. Good fit for mid-market customers seeking cost-effective, application-specific probes.

- Dwyer Instruments / Omega Engineering — Positioned for diverse liquid and paste applications with pragmatic 4–20 mA output devices; often selected where functional simplicity and rapid delivery matter.

- NIVELCO Process Control Co. — Competitive momentum in North America following its 2026 product catalog release highlighting higher-sensitivity rod solutions. Strategic implication: NIVELCO is targeting both retrofit opportunities and greenfield projects where sensitivity and simplified inventory are key.

- Regional and specialty players (SenTec, BinMaster, UWT, Baumer, Balluff) — These vendors differentiate through customized probes, silo/bin-specific expertise, or compact form factors for OEM embedding. They are often attractive tuck-in targets or regional distributors’ preferred suppliers.

From a market structure perspective, concentration metrics indicate a moderately consolidated industry: the top three vendors do not dominate overwhelmingly (CR3 around 38.45%), while the top five account for a larger, but not monopolistic, share (CR5 approximately 54.12%). This configuration sustains competitive pricing and creates opportunities for midsize players to defend niches through faster innovation cycles or superior local services.

Vertical dynamics and cross-sector signals

Adoption patterns vary by end market. Water and wastewater, chemicals, food & beverage, oil & gas, and pharmaceuticals continue to be priority applications, each driven by distinct technical and regulatory requirements. Crucially, external sector-level shocks influence purchasing:

- Healthcare funding pressure: Recent industry data indicates many hospital systems expect constrained capital expenditure over the near term. Vendors relying heavily on healthcare sales should recalibrate sales cycles, stressing low-disruption retrofits and demonstrable near-term ROI.

- Rising operating costs: With operating expenses expanding in healthcare and other service sectors, buyers favor sensors that reduce labor and unplanned downtime — areas where smart diagnostics and remote monitoring deliver measurable value.

- Digitization tailwinds: Broader trends toward sensor integration with predictive maintenance and plant analytics underpin demand for transmitters that support HART, digital outputs, and edge connectivity.

Practical recommendations for 2026 planning

- Product roadmap: Accelerate development of field-upgradable firmware and remote-calibration features; prioritize material variants that lower life-cycle costs in corrosive and hygienic environments.

- Commercial strategy: Shift toward bundled service models and subscription-based maintenance offerings to smooth revenue and increase switching costs.

- Channel and inventory: Localize critical spares and certified service technicians in target regions to shorten procurement lead times and win specification-driven bids.

- M&A and partnerships: Evaluate regional specialists and sensor-integrator targets to broaden solution portfolios without diluting brand trust.

- Risk management: Hedge component concentration risk and formalize alternate supplier qualification to reduce disruption exposure.

Conclusion — what to do next

PW Consulting’s "Worldwide Rod Capacitive Level Gauge Market" report is engineered to convert market intelligence into executable plans for 2026. The market’s steady growth trajectory and the current competitive structure create attractive opportunities for vendors and buyers who can combine technical differentiation with service-driven business models. For procurement leaders, the study provides vendor scorecards and negotiation playbooks; for corporate strategy and M&A teams, it supplies target archetypes and valuation heuristics.

To access the complete dataset, full segmentation, and the tactical annex with negotiation templates and ROI calculators, please consult the full report. The release intentionally withholds detailed segmentation tables from this announcement to preserve the practical value of the study for licensed readers.

PW Consulting — strategic clarity for sensing markets entering their next decade of industrial digitization.

For detailed analysis of this topic, please visit the official page:Worldwide Rod Capacitive Level Gauge Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com