Worldwide Smart Antimicrobial Surface Market: Strategic Briefing for 2026 Decision-Makers

Executive snapshot

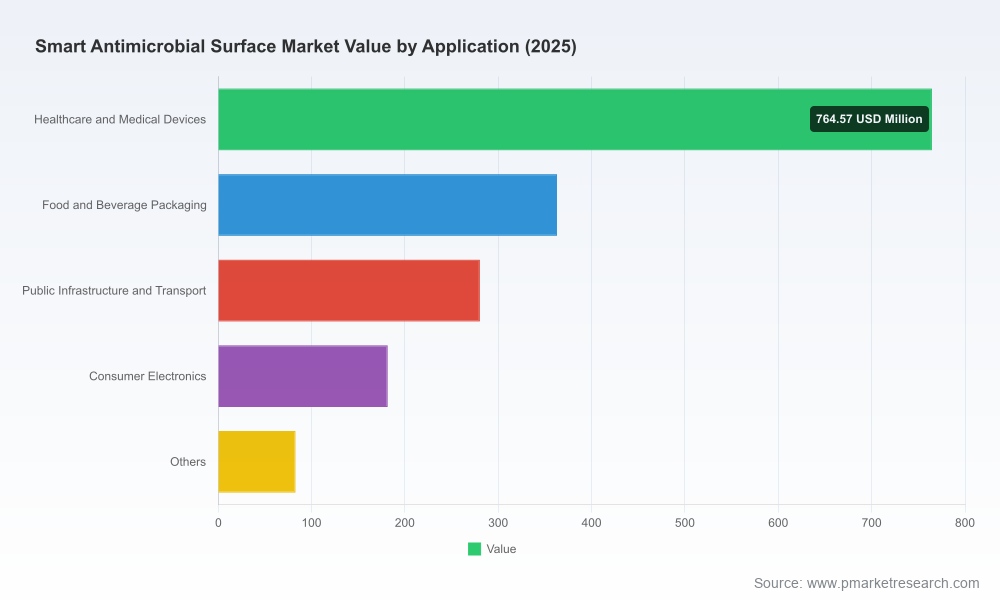

PW Consulting’s latest market study, Worldwide Smart Antimicrobial Surface Market (base year 2025), positions this sector as one of the high-growth adjacent markets for medtech, advanced materials, and critical infrastructure suppliers in the second half of this decade. Following a recovery and acceleration phase from 2020–2025, the global market reached an estimated USD 1,672.4 Million in 2025 and is projected to expand at a 12.0% CAGR through a detailed 2026–2032 forecast horizon. By the end of our forecast the market reaches a materially larger scale, signaling sustained commercialisation and diffusion across healthcare, packaging, transport and consumer electronics ecosystems.

Worldwide Smart Antimicrobial Surface Market

Why 2026 is a strategic inflection point

Although antimicrobial surface technologies have been developing for years, 2026 is where enabling conditions converge: product performance validation, regulatory clarity, scaled manufacturing upgrades, and procurement willingness among institutional buyers. Our analysis highlights three simultaneous forces shaping near-term outcomes:

Worldwide Smart Antimicrobial Surface Market

- Regulatory classification and pathways are maturing: novel non-leaching, surface-active and covalently bound nanosurface approaches are now being evaluated under distinct regulatory constructs, which materially change time-to-market and evidence requirements for device makers and OEMs.

- Supply-side consolidation and technology diversification: leading platform providers are combining coatings chemistry, automated application equipment and in-line quality systems to lower unit costs and mitigate scale-up risk—creating winner-takes-advantage dynamics in some product corridors.

- Customer procurement sophistication: hospitals, device OEMs and institutional specifiers increasingly demand lifecycle evidence (durability, biocompatibility, cleaning compatibility) rather than single-point lab efficacy metrics—shifting commercial value from claims to verifiable outcomes.

What our report delivers to corporate leaders

This study is deliberately operational. Beyond market sizing and a 2026–2032 forecast, PW Consulting’s report provides a toolkit that executives can immediately apply to investment, product development and go-to-market planning:

Worldwide Smart Antimicrobial Surface Market

- Commercial playbooks for five distinct customer archetypes (large hospital systems, device OEM procurement, packaging integrators, transport authorities, consumer brands) with tailored value propositions and pilot design templates;

- A vendor evaluation framework that scores suppliers across technical maturity, regulatory readiness, GMP-capable manufacturing, claims defensibility and service delivery (coating application, inspection, warranty);

- Capital deployment models that quantify CapEx/Opex trade-offs for insourced coating lines versus toll-coating and contract manufacturing partners;

- Regulatory and clinical evidence roadmaps that map ISO 10993 requirements, biocidal product registration triggers, and submission strategies to reduce clinical trial burden and accelerate reimbursement discussions;

- IP and competitive landscaping including threat matrices for material-science substitutes (metal-based vs polymeric vs bio-based), and scenarios for licensing, joint development or acquisition;

- Procurement case files and savings calculators that demonstrate total cost of ownership benefits when antimicrobial surfaces are specified as part of broader infection-prevention bundles.

Competitive landscape — who to watch and why

The market today is neither monopolistic nor atomised: concentration metrics indicate a mid-range level of aggregation among the top players, leaving room for both platform leaders and niche specialists. Our competitor profiles combine product-level differentiation, regulatory milestones and recent strategic moves to help buyers and investors prioritise partners.

- HeiQ Materials AG — Switzerland (production in Germany): HeiQ’s SANPURE silver-based coatings are positioned as high-efficacy, transparent surface treatments suitable for high-touch hospital infrastructure and medical tools. Their focus on biocompatibility and abrasion resistance aligns them with institutional procurement that prioritises durability and cleaning compatibility.

- Covalon Technologies Ltd. — Canada: Covalon has concentrated on medical device coatings with bespoke adhesive and dual-antimicrobial silicone solutions. Their strengths are custom device-level integration and established relationships in vascular access and wound care supply chains.

- Hydromer, Inc. — USA (Concord, NC): Hydromer’s portfolio emphasises hydrophilic, thromboresistant and antimicrobial integrations. Recent expansion into automated high-speed coating and UV cure equipment signals a push towards vertically integrated supply for device OEMs seeking scale and process control.

- Specialty Coating Systems (SCS) — USA (Indianapolis, IN): SCS’s conformal parylene-based microRESIST technologies serve implantable and non-implantable device segments where high log reductions and biocompatibility are prerequisites. Their materials expertise supports applications where long-term device compatibility matters.

- BioInteractions Ltd. — United Kingdom (Reading): With non-leaching, contact-kill TridAnt systems, BioInteractions is positioning permanent surface-active coatings for long-term implants and devices—an attractive profile for companies seeking durable antimicrobial performance without systemic release concerns.

- Orthobond Corporation — USA (Princeton, NJ): Orthobond’s OSTAGUARD covalently bound nanosurface (quaternary ammonium-based) recently moved from regulatory clearance to initial commercial delivery, creating an early-adopter reference case for spinal implants and other rigid metallic devices.

- SurModics, Inc. — USA: SurModics brings integrated device coatings with infection-resistance attributes and a track record in hydrophilic and drug-delivery coatings—relevant for companies seeking multifunctional surface engineering.

- Parx Materials N.V. — Netherlands (Rotterdam): Parx’s biocide-free Passive Action Polymer Technology (zinc-based) targets polymeric components and textiles, appealing to manufacturers prioritising non-leaching, compliance-friendly approaches for consumer and medical applications.

Recent industry moves and regulatory dynamics shaping 2026 playbooks

Our fieldwork and primary-source monitoring captured important near-term events that materially affect competitive positioning and adoption timelines:

- Manufacturing scale-ups and equipment investments — for example, a leading hydrophilic coating supplier announced expanded automated coating and UV-cure capabilities to support higher throughput for medical device customers. Expect capacity availability and process control to become decisive negotiation levers in 2026.

- Commercial rollouts following regulatory precedents — an FDA De Novo classification for a covalently bonded antimicrobial nanosurface (rigid metallic implants) set a new procedural reference that will influence submission strategies and claims language across applicants.

- Product introductions emphasising zero-release, contact-kill chemistries and surface-active systems—these developments reduce regulatory friction in certain jurisdictions compared with releasing biocides, but they require robust biocompatibility packages and long-term durability evidence.

Strategic implications for corporate decision-makers

For executives planning 2026 investments, the implications are actionable and time-sensitive. PW Consulting recommends prioritising four concurrent agendas:

- Portfolio-level differentiation: Decide whether your company competes on platform breadth (covering multiple surfaces and substrates) or depth (specialised, high-value device coatings). Each path requires different R&D pacing and sales channel investments.

- Manufacturing and supply-chain resilience: Given the projected market growth and rapid adoption in regulated channels, securing scalable, quality-controlled coating capacity (either by in-house capital projects or long-term toll agreements) should be an immediate procurement objective.

- Regulatory and claims strategy integration: Align product development with ISO 10993 requirements and anticipate biocidal registration triggers in key geographies. For many players, demonstrating non-leaching mechanisms and clear clinical utility will materially shorten commercial cycles.

- Evidence-based commercial pilots: Structure pilots to deliver measurable outcomes—reduction in contamination events, maintenance cost offsets, and device longevity improvements—so buyers can model total cost of ownership. Avoid pilots that only replicate in-vitro efficacy data; buyers want impact in situ.

Risk factors and mitigation

Our scenario analysis identifies three principal risks for entrants and incumbents:

- Regulatory reinterpretation or disparate regional requirements that fragment claims and force multiple registration tracks. Mitigation: modular evidence dossiers and harmonised clinical endpoints.

- Material-substitute competition (e.g., polymeric passive action vs metal-based active surfaces) driving price pressure in commoditised applications. Mitigation: move up the value chain through lifecycle services and demonstrable outcomes.

- Quality and durability failures in fielded installations (cleaning compatibility, abrasion) that undermine buyer confidence. Mitigation: invest in standardised wear and cleaning testing within contractual warranties.

How PW Consulting’s research helps you act in 2026

Our report is designed as a practical decision-support package. It fuses quantitative forecasts (historical series 2020–2025 and a robust 2026–2032 projection at a 12.0% CAGR) with qualitative playbooks, supplier scorecards, regulatory roadmaps and executable pilot templates. For leaders contemplating M&A, licensing, or manufacturing scale-up, the report’s integrated valuation models and risk-adjusted scenario outputs are particularly valuable.

Get the full intelligence

This briefing purposefully highlights strategic signals while reserving the granular segmentation and proprietary vendor scoring that drive transaction-level decisions. For access to the full dataset (detailed market tables, regional and application splits, CR-level concentration matrices, supplier scorecards and downloadable pilot templates), please consult the report landing page where PW Consulting hosts the complete Worldwide Smart Antimicrobial Surface Market study and bespoke advisory services.

PW Consulting stands ready to support board-level briefings, vendor selection processes and tailored go-to-market workshops informed by the report’s findings. Contact our Strategic Advisory team to schedule a confidential briefing and to explore tailored scenario modelling for your organisation.

For detailed analysis of this topic, please visit the official page:Worldwide Smart Antimicrobial Surface Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com