Limo Service Elevating Every Journey with Luxury, Comfort, and Reliability

Other |

2026-06-09 09:03:59

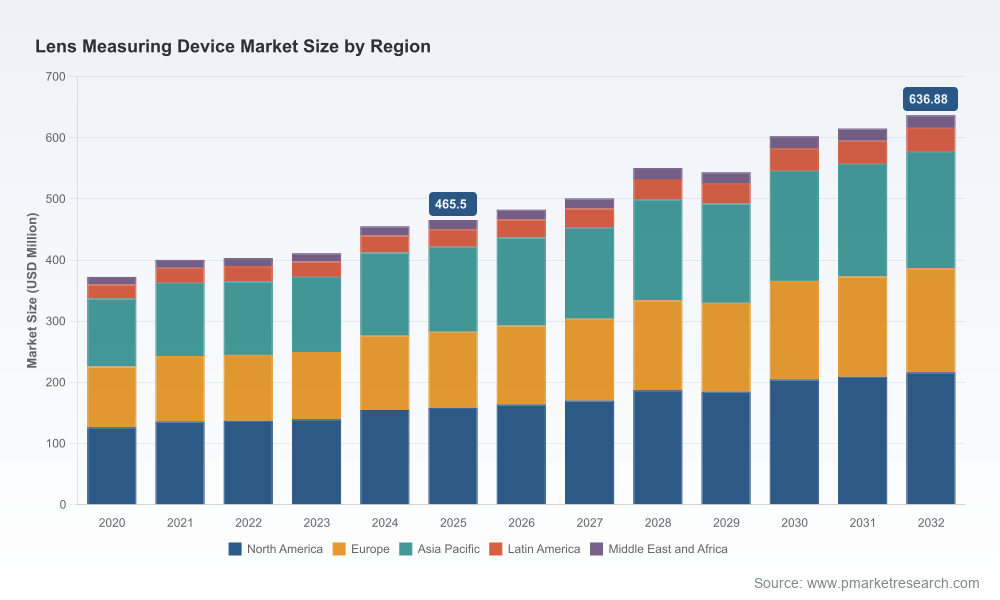

PW Consulting’s latest market intelligence release on the Worldwide Lens Measuring Device Market provides a focused, operational playbook for executives planning 2026 strategic moves. Built on a base year of 2025 and a forecast horizon to 2032, the study quantifies a clear recovery and expansion trajectory: the global market grew from an estimated USD 372.4 Million in 2020 to about USD 465.5 Million by 2025, and under our central scenario it progresses at a mid-single-digit compound annual growth rate (CAGR) through 2032. This release is designed as a decision-grade resource — rich in directional analytics, practical tools and scenario evaluations — while preserving the granular segmentation tables behind our subscription gateway to encourage direct engagement with the full dataset.

Worldwide Lens Measuring Device Market

Timing capital allocations. With the market on a steady up-cycle into the 2026 budgeting season, buyers and OEMs must align CapEx and R&D timetables to the medium-term forecast. Our report translates topline growth assumptions into actionable procurement windows and replacement cycles for clinical buyers and retail chains.

Worldwide Lens Measuring Device Market

Product roadmaps and feature prioritization. Measurement systems with expanded automation (including wavefront-based analysis), multi-point sensors for high-accuracy verification, and integrated UV/blue-light metrics are shaping buyer preferences. The report maps which capabilities move deals faster in different buyer segments and suggests minimum viable product (MVP) configurations for 2026 launches.

Worldwide Lens Measuring Device Market

M&A and partnership playbooks. Market momentum combined with fragmentation among mid-sized equipment suppliers creates opportunistic conditions for strategic consolidations, distribution alliances and co-development partnerships. We outline value creation scenarios and integration checklists tailored to both acquirers and targets.

Regulatory and market-access pacing. Lens measuring devices are regulated as medical devices in key jurisdictions, requiring conformity pathways that affect time-to-market and cost curves. Our study quantifies plausible approval timelines and regulatory effort estimates to support go/no-go decisions for product introductions in 2026.

Service and revenue-model choices. As customers increasingly demand digital integration into exam suites and remote-managed calibration, device manufacturers must weigh outright sales versus servitization models (e.g., device-as-a-service, bundled workflows). We provide revenue-model sensitivity analyses to inform pricing and retention strategies.

Time-series market sizing and a range-bound forecast to 2032 (base year 2025), including upside and downside scenarios calibrated to supply chain, regulatory and clinical adoption risk factors.

Buyer segmentation matrices and procurement decision trees that convert market trends into checklists for hospital systems, optical retailers and lens manufacturers.

Technology adoption heat maps assessing automation, sensor architectures, UV/blue-light capabilities and software integration priorities by buyer type.

Competitive benchmarking tools: feature-scorecards, time-to-certification estimates, and vendor capability matrices that support shortlisting for sourcing or M&A diligence.

Commercial playbooks: go-to-market routes, distribution models, pricing ladders, warranty and service strategies aligned to 2026 buyer expectations.

Procurement and TCO calculators that convert device list prices, service contracts and expected throughput into multi‑year cost of ownership models for clinics and retail chains.

Regulatory navigation maps, including the practical implications of Class II device classification and quality-management expectations, with an ISO 13485 compliance checklist.

Raw datasets and reproducible forecast inputs — available in the full report — for teams that run proprietary scenario modeling or internal valuation exercises.

The supplier universe for lens measuring devices mixes global optics/ophthalmic OEMs, specialist diagnostic equipment manufacturers, and a set of regional distributors. Several themes define the competitive dynamics going into 2026:

Leaders pushing automation and integration. Incumbents with deep optics and diagnostic expertise are differentiating via wavefront technology, expanded measurement point architectures, and embedded spectrometers that quantify UV and blue-light characteristics. These feature sets improve clinical confidence and enable premium pricing in certain buyer segments.

Collaborative supply models. Partnerships and OEM agreements (including distribution and co-branded product arrangements) are increasingly common as device makers pursue rapid route-to-market without duplicating manufacturing or certification investments.

Mid-sized players competing on workflow fit. Companies focused on optometry practice workflows emphasize ease-of-use, interface compatibility with digital exam suites, and service responsiveness — attributes that matter nearly as much as raw measurement specs to many buyers.

Examples to benchmark. Prominent names illustrate these dynamics: technology-driven firms that emphasize wavefront and spectrometry solutions; manufacturers deploying multi-point Hartmann sensor arrays for high-accuracy verification; regionally strong suppliers that prioritize clinical usability and service networks; and diagnostic portfolio players integrating lensmeters into broader digital exam suites. Recent product debuts in the trade show circuit continue to push automation and user-experience upgrades as near-term differentiators.

Regulatory gateways influence commercialization timelines. In major markets lens measuring devices are regulated such that vendors should plan for formal clearance processes; this affects launch sequencing and resource allocation for regulatory filing and quality-system investments.

Quality systems matter for market access. Compliance with global medical-device quality frameworks is a baseline expectation; this includes documented processes for design controls, supplier management and post-market surveillance.

Reimbursement nuances limit direct device-level reimbursement. Lens measurement procedures are commonly bundled into broader eye exam or refraction billing codes, rather than generating device-specific reimbursement. For OEM commercial teams, this means value arguments should target operational efficiency, throughput and clinical accuracy rather than asserting stand-alone device reimbursement.

Hospital and clinic purchasing is CapEx-driven. Procurement cycles in clinical settings favor integration into digital exam suites and demonstrable workflow time savings; the report translates these buyer preferences into procurement decision matrices that influence supplier selection.

Automation and accuracy. Multi-point sensing and advanced optical analysis continue to push the boundary of measurement accuracy, supporting premium positioning among discerning clinical buyers.

Software-enabled workflow integration. Devices that integrate seamlessly with patient record systems, provide standardized data exports and enable remote calibration/service earn shorter procurement cycles.

Servitization. Manufacturers that offer lifecycle services — calibration, predictive maintenance, software updates and outcome analytics — unlock recurring revenue streams and strengthen customer retention.

Cloud and AI augmentation. Early implementations of AI for anomaly detection and automated verification reduce technician time and error rates; buyers will scrutinize models for explainability and regulatory readiness.

OEMs and product teams — use the feature-pricing matrices and certification timelines to prioritize 12–18 month roadmaps and plan regulatory submissions that align with 2026 commercial targets.

Distributors and channel partners — leverage the buyer segmentation and procurement checklists to tailor sales motions for optical retail groups, hospital systems and manufacturing quality departments.

Healthcare providers and group purchasers — apply our TCO models and throughput analyses to standardize procurement specifications, enabling apples-to-apples comparisons across competing bids.

Investors and corporate development teams — use the scenario analyses and vendor benchmarking to identify attractive consolidation targets, partnership opportunities and technology gaps that can be addressed through M&A.

This strategic preview surfaces the decisive themes and practical actions you need for 2026 planning: a recovering and expanding addressable market, technology-driven differentiation, procurement decisions skewed toward integration and service, and regulatory constraints that condition time-to-market. For practitioners requiring the granular inputs — full regional and application splits, vendor market shares, concentration metrics, downloadable time-series spreadsheets and our complete methodology — the comprehensive dataset and executable templates are available in the PW Consulting report portal. The full dossier contains the withheld segmentation tables and raw figures that underpin all the playbooks summarized here, enabling teams to plug our assumptions directly into internal models and procurement processes.

To engage with the full report, access the Worldwide Lens Measuring Device Market dossier on the PW Consulting website or contact your firm’s account executive to arrange a briefing and dataset export tailored to your 2026 strategic planning cycle.

For detailed analysis of this topic, please visit the official page:Worldwide Lens Measuring Device Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com