US GNSS Simulators Market Size, Share, and Forecast to 2034

Technology |

2026-06-29 12:16:00

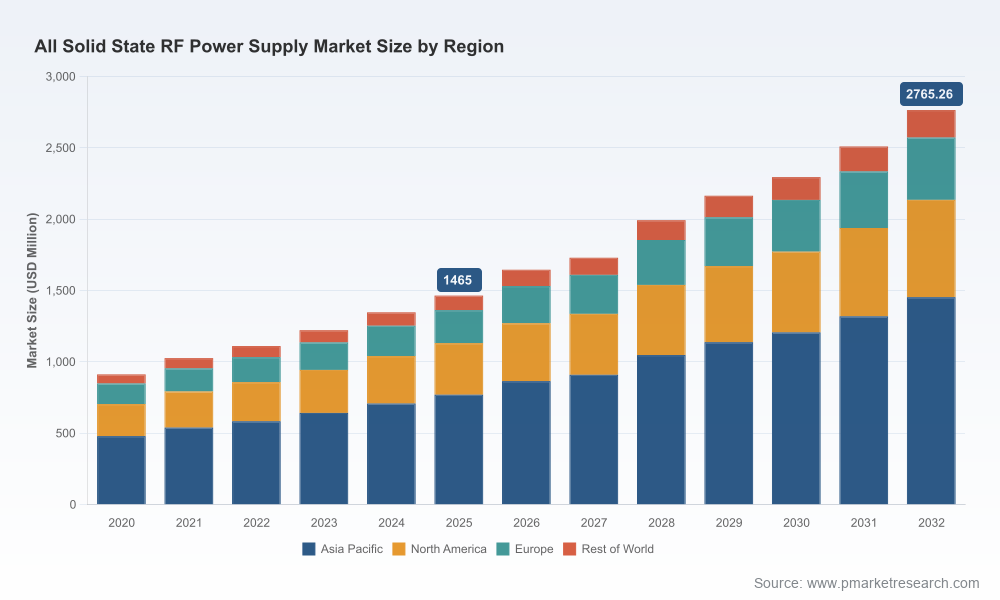

As capital allocation committees, product leaders, and strategic sourcing teams prepare budgets for 2026, the all solid state RF (SSR) power supply market is moving from niche innovation to mainstream industrial and semiconductor infrastructure. PW Consulting’s latest market study—anchored on a 2025 base year and projecting through 2032—identifies the economic momentum and technological inflection points that will determine winners and losers over the next investment cycle. The global market expanded to approximately USD 1,465.0 Million in 2025 and, under a baseline outlook, is expected to grow at a 9.48% CAGR to exceed USD 2,700 Million by 2032. For leadership teams planning product roadmaps, factory upgrades, or M&A activity in 2026, the quantitative trajectory is clear: materially larger addressable markets combined with accelerating technology substitution create windows for differentiation and consolidation.

Worldwide All Solid State RF Power Supply Market

Three converging forces make 2026 a tipping point. First, operational economics—driven by solid‑state efficiencies and lifecycle maintenance savings—are changing total cost of ownership calculations for plasma processing, thin film deposition, dielectric heating, and other RF‑driven industrial processes. Second, semiconductor end‑market demand patterns and adjacent industrial applications are finally aligning in favor of digital, precisely controlled RF solutions. Third, supply‑side maturation—particularly the availability of mature LDMOS, GaN and SiC transistor ecosystems—reduces technical risk for high‑power solid‑state designs.

Worldwide All Solid State RF Power Supply Market

These dynamics translate into concrete strategic choices: accelerate product development to capture near‑term replacement cycles, rationalize supplier portfolios toward low‑risk, high‑efficiency vendors, or pursue bolt‑on M&A to accelerate market entry. Our study provides the data and decision frameworks required to assess each path without exposing proprietary tactical segment breakdowns that competitive parties could exploit.

Worldwide All Solid State RF Power Supply Market

Market scale and growth: The worldwide SSR RF power supply market is in rapid expansion mode. From a 2025 base of USD 1,465.0 Million, our baseline forecast points to a near‑term inflection followed by sustained expansion to more than USD 2.7 Billion by 2032. That growth is underpinned by replacement of legacy tube and magnetron platforms and new greenfield industrial adoption.

Consolidation dynamics: The top tier of suppliers exerts meaningful influence—our concentration analysis shows a moderately concentrated market where the three largest players account for over half of industry revenues, with the top five approaching roughly seven in ten of the market. This profile signals healthy competitive tension while leaving room for regional specialists and high‑performance newcomers.

Technology drivers: LDMOS, GaN and SiC transistor technologies are the gating factors in design performance. Vendors delivering >90% system efficiencies in real‑world deployments achieve compelling payback profiles, particularly for continuous industrial RF processes where energy is a dominant operating cost.

Regulatory and band considerations: Operation in established ISM bands (including 13.56 MHz and 2.45 GHz) remains a core enabler of industrial deployment, lowering regulatory friction for many applications.

PW Consulting designed this study to be utility‑grade for strategy, procurement, and product teams. Key operational deliverables include:

Market sizing and forward scenarios (base, upside, downside) calibrated to multiple demand drivers so you can stress‑test CapEx plans.

Detailed technology adoption roadmap mapping LDMOS/GaN/SiC readiness to power tiers and control architectures—useful for product development prioritization.

Supplier heatmaps and a configurable scorecard framework to evaluate vendors across technical performance, service footprint, reliability data, and total cost of ownership.

Procurement playbooks with negotiated terms, lifecycle maintenance models, and energy savings calculators tailored to continuous vs. pulsed process profiles.

M&A and partnership screening matrices—identifying where inorganic moves will accelerate market entry versus where organic R&D investment is more effective.

Regulatory and standards checklist for ISM band operations and electromagnetic compatibility considerations in manufacturing environments.

The market exhibits a mixture of established instrument OEMs, specialist RF vendors, and focused high‑power innovators. Each occupies distinct strategic roles:

Advanced Energy (United States): A validated leader in semiconductor RF plasma generators; its suite of solid‑state platforms emphasizes precision RF and pulsed control tailored for process repeatability and integration with fab automation.

MKS Instruments (United States): Combines generator hardware with impedance matching and control subsystems—positioned as a systems supplier for thin film and deposition equipment OEMs seeking one‑stop RF delivery solutions.

TRUMPF Hüttinger (Germany): Strong in industrial plasma excitation and heating, leveraging decades of RF expertise and global service networks; attractive to industrial buyers prioritizing uptime and global support.

Coaxial Power Systems Ltd (United Kingdom): A cost‑effective specialist focused on sputter coating, ICP, diamond deposition and bespoke projects—well suited for non‑commodity industrial applications requiring flexible matching solutions.

Elite RF, Empower RF Systems, and Crescend Technologies (United States): High‑power and microwave specialists, delivering large‑scale amplifiers and magnetron replacements for industrial heating, CVD, and defense test applications; their appeal lies in power density and modular cooling designs.

Aethera Technologies (Canada) and Ampegon (Switzerland): Engineering‑heavy firms pushing high‑efficiency modular architectures for industrial heating and scientific acceleration applications; they demonstrate how high efficiency and reliability can be commercialized at scale.

pinkRF B.V. (Netherlands): Represents a new wave of programmable SSR vendors—its 2025 MPG10kS product launch underscores the trend toward ISM band programmable devices positioned as magnetron substitutes in dielectric heating and plasma processes.

Together, these vendors illustrate two competitive archetypes: system integrators that sell breadth and lifecycle support, and component‑oriented innovators that compete on efficiency, modularity and power density. Your strategic choice—partner with integrated providers, source modular subsystems, or develop in‑house capability—depends on your firm's appetite for vertical integration versus supplier risk reduction.

Solid‑state RF designs are dependent on advanced semiconductor transistors (LDMOS, GaN, SiC). The availability, cost volatility, and qualification cycles of these devices materially affect product roadmaps and manufacturing timelines. Buyers should prioritize suppliers with multi‑sourcing strategies or demonstrated long‑term vendor agreements for key RF semiconductors. In addition, thermal management and packaging supply chains (air/liquid cooling, RF combiners) are critical bottlenecks for high‑power units and deserve specific procurement attention in 2026.

Prioritize pilot integrations now: Start lab and production pilots in H1–H2 2026 to capture replacement cycles. The economics of SSR over legacy tubes become evident after live process validation—don’t wait for perfect benchmarks.

Adopt a hybrid sourcing strategy: Combine a system supplier for turnkey support with modular vendors for price and technology optionality. This hedges against single‑point failures and accelerates innovation absorption.

Factor efficiency into CapEx models: Pure price comparisons mask operational savings. Incorporate lifecycle energy and maintenance models into procurement scorecards to reveal true payback timelines.

Lock down semiconductor supply: Secure strategic agreements for GaN/LDMOS/SiC components where product roadmaps depend on predictable device supply and performance.

Scan for M&A targets: Identify regional specialists and programmable RF newcomers as bolt‑on acquisition opportunities to secure differentiated IP and faster market access.

Our report is designed as a working toolkit, not a static PDF. Clients receive a decision pack that includes modelled TCO calculators, supplier scorecards, and scenario playbooks to expedite boardroom decisions. Because the most valuable insights are tactical and context‑sensitive, we intentionally keep granular segment tables and company‑level revenue shares within the full report to preserve commercial confidentiality and to ensure subscribers gain exclusive access to actionable segmentation intelligence.

If your 2026 strategy requires clear answers—whether that’s choosing a primary SSR vendor, structuring an acquisition thesis, or designing a five‑year capital plan—PW Consulting’s Worldwide All Solid State RF Power Supply Market report provides the forecasts, risk matrices and procurement templates you need to move from analysis to execution. For full access to the segment breakouts, vendor benchmarking, and downloadable decision tools, visit our research portal and request the executive package.

The transition to all solid state RF power supplies is not incremental; it is structural. The market’s rapid scale‑up, combined with improving device efficiencies and the availability of programmable, high‑power architectures, creates durable strategic opportunities for firms that prepare now. 2026 will separate early adopters and orchestrators from laggards. Use the coming year to validate pilots, secure supply chains, and align procurement economics with long‑term operational returns—our report supplies the data, frameworks and operational toolsets to make those decisions with confidence.

For detailed analysis of this topic, please visit the official page:Worldwide All Solid State RF Power Supply Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com