Polyvinylpyrrolidone (PVP) for Lithium‑Ion Batteries: A 2026 Strategic Briefing

Executive summary

As lithium‑ion battery manufacturing scales to meet electrification goals across transportation, grid storage and consumer electronics, the market for specialty binders and dispersants has emerged as a strategically important upstream segment. Our latest PW Consulting market study on Polyvinylpyrrolidone (PVP) for lithium‑ion batteries frames this opportunity with a data‑driven forecast and actionable guidance for 2026 decision makers. The PVP market has more than doubled in value since 2020 and, under our base forecast, is projected to continue expanding at a compound annual growth rate of roughly 11.24% through the 2026–2032 horizon. This sustained growth underscores PVP’s role as a performance enabler across electrode slurries, separator coatings and advanced dispersant applications.

Polyvinylpyrrolidone (PVP) for Lithium Ion Battery Market

Why this report matters for 2026 decisions

Companies entering or operating in battery materials face three simultaneous pressures in 2026: accelerate time‑to‑market for differentiated chemistries, secure resilient and cost‑effective supply chains, and create defensible economics against input volatility and regulatory friction. Our PVP study translates market growth into decision‑useful intelligence — combining top‑line market sizing, concentration analysis, supplier profiling, raw‑material dynamics and hands‑on playbooks. While the full dataset and segment granularity are reserved for the report itself, the research delivers the strategic context boards and commercial teams need to prioritize investments, de‑risk procurement, and design competitive product roadmaps.

Polyvinylpyrrolidone (PVP) for Lithium Ion Battery Market

What the report contains — operational, transaction and technical tools

- Proprietary market model (historical 2020–2025 baseline and forecast 2026–2032) with scenario toggles for demand elasticity, price paths and regulatory stress tests.

- Concentration and competitive landscape analysis, including supplier scorecards that capture technical capability, production quality (battery‑grade controls), and geographical footprint.

- Supplier due diligence checklists, commercial contract templates (fixed vs index‑linked pricing), and a procurement playbook tailored for polymer feedstock risks.

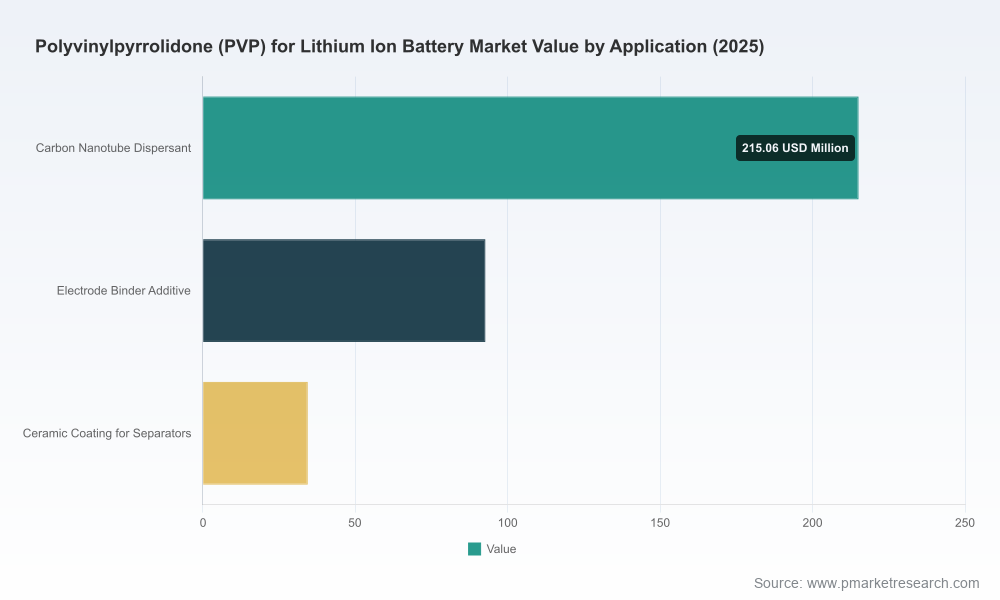

- Technical appendix on PVP grades (K‑series performance characteristics), use cases (dispersant, binder additive, separator ceramic coatings), and lab‑to‑line scale considerations.

- Valuation playbook for M&A and joint ventures (earn‑outs, earn‑ins and technology licensing structures) plus simple NPV templates calibrated to our market model.

- Regulatory and sustainability matrix outlining likely compliance levers and reputational risks tied to upstream monomer supply and chemical park constraints.

Macro dynamics shaping PVP in 2026

Several interlinked forces determine PVP market outcomes over the next twelve months and beyond:

Polyvinylpyrrolidone (PVP) for Lithium Ion Battery Market

- Robust end‑market demand: The trajectory of battery manufacturing capacity continues to support above‑average growth for battery‑grade additives. Our market model quantifies this using historical growth through 2025 and a forecast up to 2032, reflecting strong capital commitments across EV OEMs and cell producers.

- Upstream feedstock exposure: PVP production is fundamentally tied to N‑vinylpyrrolidone (NVP) and other commodity intermediates. Variability in feedstock availability, particularly in regions subject to environmental curbs, can abruptly tighten the market for high‑purity grades and drive premium pricing for battery‑grade materials.

- Technical differentiation matters: Not all PVP is created equal. Battery applications demand tightly controlled impurity profiles, polymer K‑values tuned to rheological needs, and manufacturing practices aligned to battery‑grade cGMP standards. Suppliers that combine high‑purity production with application‑specific know‑how command pricing power and preferred supplier status.

- Concentration and bargaining dynamics: The market displays high levels of supplier concentration, with a small set of global and regional players controlling the majority of supply—creating both supply risk and strategic leverage for well‑positioned buyers and suppliers.

Competitive landscape — supplier archetypes and implications

Our competitive analysis groups active players into three archetypes, each with distinct implications for buyers and investors:

- Global performance polymer majors — exemplified by producers with deep R&D and specialty binder portfolios. These players offer differentiated chemistries for separator coatings and advanced binder systems, and are attractive partners for OEMs looking for co‑development and long‑term supply assurance.

- Large chemical conglomerates — companies with broad additive portfolios that can bundle materials and provide scale, technical breadth, and robust quality systems. Their scale supports long‑term contracts and multi‑region footprint advantages.

- Specialist battery‑grade producers — a group of producers, particularly in Asia, focused on battery‑grade K‑series PVP and industrial scales optimized for slurry and dispersant applications. These suppliers emphasize cost competitiveness, local supply security and rapid application support for cathode manufacturers.

Representative firms profiled in the report include Ashland Inc., BASF SE, Boai NKY, NIPPON SHOKUBAI, Synvent Materials (Ningxia), Henan Pengfei New Materials and Huzhou Sunflower Specialty Polymer. Our vendor matrix evaluates each on technical portfolio, quality controls, capacity, transparency, and commercial flexibility. Notably, the market shows high consolidation at the top—the top three suppliers account for roughly two‑thirds of the market while the top five reach close to four‑fifths—an important context for negotiation strategy and risk management.

Recent supplier moves and what they signal (selection)

- Technical application updates from several Chinese producers during 2024–2025 point to accelerated lab‑to‑line validation of K30 formulations in cathode slurries, signaling narrowing performance gaps between local and global suppliers.

- Increased profiling and benchmarking activity among global buyers in early 2026 reflects a shift toward supplier scorecards that factor in trace‑impurity controls, cGMP practices and environmental compliance—beyond simple cost per ton comparisons.

Strategic recommendations for 2026 (actionable priorities)

For executives and investment committees deciding in 2026, our report crystallizes choices into a set of prioritized actions:

- Operational resilience — multi‑tier sourcing: Adopt a “primary + strategic secondary” sourcing model. Secure capacity with at least one global supplier offering specialty binders and one regional battery‑grade producer to mitigate local feedstock or regulatory disruptions.

- Contract design — blend fixed and index‑linked elements: Combine baseline volumes under fixed‑price or floor‑price contracts with a flexible tranche tied to a transparent index to balance predictability and market responsiveness.

- Vertical options — evaluate upstream integration selectively: For large cell makers with predictable volume growth, evaluate minority investments or tolling agreements with producers to secure battery‑grade throughput without the full capex of polymer production.

- Product strategy — prioritize performance and scale: Invest in in‑house formulation capability to exploit PVP’s functional role (dispersant, binder additive, separator coatings), focusing R&D on grades that shorten processing time or improve electrode loading—tangible metrics that resonate with OEM value chains.

- Regulatory and sustainability diligence: Embed upstream supplier audits into procurement and incorporate lifecycle and compliance metrics into supplier scorecards to avoid single‑source exposure stemming from regional regulatory actions.

- M&A and partnership playbook: For chemical companies seeking to enter or expand in the battery PVP space, pursue bolt‑on acquisitions of regional battery‑grade capacity or JV structures that combine process expertise with local market access.

Using the PW Consulting report in the boardroom

Boards and executive teams can use the deliverables to fast‑track 2026 decisions across three agendas:

- Capex and supply chain: Calibrate plant capacity decisions and capital allocations using our scenario outputs to test upside demand, price volatility and feedstock shocks.

- Commercial negotiations: Deploy supplier scorecards and pricing templates directly in RFPs and contract negotiations to shorten procurement cycles and reduce execution risk.

- Technology roadmapping: Prioritize polymer grades and binder formulations that deliver the greatest margin lift or process simplification for cell manufacturing lines, backed by lab validation pathways outlined in the technical appendix.

Conclusion — from insight to implementation

PVP is no longer an ancillary commodity in the battery value chain; it is a decision‑critical input where purity, polymer properties and supplier reliability materially affect cell performance and manufacturing economics. Our 2026‑oriented briefing makes two central points clear: the addressable market is expanding rapidly and supplier dynamics are increasingly strategic. Executives who act now—by securing diversified supply, aligning contracts to manage feedstock volatility, and investing in formulation capabilities—will both protect margins and unlock performance advantages.

To access the full dataset, segment breakdowns, supplier scorecards and downloadable models that underpin these conclusions, please consult the PW Consulting market report landing page for Polyvinylpyrrolidone (PVP) for Lithium‑Ion Batteries. The report preserves detailed segmentation and proprietary forecasts to support transaction diligence, procurement strategy and R&D prioritization.

For detailed analysis of this topic, please visit the official page:Polyvinylpyrrolidone (PVP) for Lithium Ion Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com