Global Trends and Growth Analysis of the Biodegradable Pharmaceutical Packaging Market

Health |

2026-05-27 14:44:01

PW Consulting’s newly released market research on the Worldwide Cryostation Optical Cryostat Market offers a focused intelligence package tailored for procurement leaders, R&D directors, corporate strategists, and investor teams preparing to act in 2026. The market is at an inflection point: sustained double‑digit compound annual growth, measurable concentration among a handful of technology leaders, and accelerating demand driven by quantum materials and magneto‑optical experiments are reshaping supplier selection, product design priorities, and commercial models.

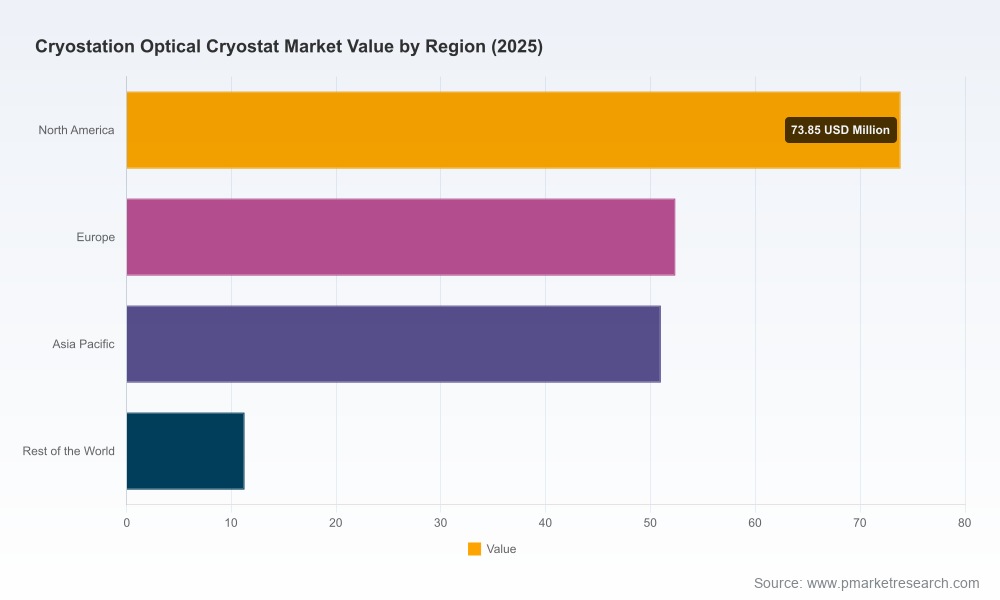

Worldwide Cryostation Optical Cryostat Market

Fast, predictable expansion: The market exhibits a robust CAGR of 10.82% across the forecast horizon, reinforcing the business case for near‑term capacity investments, channel expansion, and product line extensions focused on closed‑cycle, low‑vibration platforms.

Worldwide Cryostation Optical Cryostat Market

Strategic timing for procurement and partnerships: Buyers that align 2026 procurement cycles with vendors’ product roadmaps and trade show cadences can capture improved lead times and better integration options for nanopositioners, fiber feedthroughs, and high‑field magnet options.

Worldwide Cryostation Optical Cryostat Market

Consolidation and supplier leverage: Market concentration metrics indicate that the top three to five suppliers account for a meaningful share of revenue — creating an environment where competitive differentiation happens through feature depth, system integration, and aftermarket services rather than price alone.

Our base‑year analysis shows a market that has more than doubled in scale over the past half‑decade and is projected to continue expanding into the early 2030s. This pace of growth validates investment in modular cryogen‑free platforms, rack‑compatible mobility solutions, and automation features that reduce operator overhead. For corporate decision‑makers, the headline takeaway is simple: firms that want to lead must prioritize systems engineering and channel readiness now, not later.

PW Consulting’s report was built as a playbook for executives and technical buyers. The core deliverables are designed to convert market insight into executable plans:

Market sizing and scenario models — base, upside, and downside demand paths with sensitivity to quantum R&D funding and capital equipment procurement cycles.

Technology roadmaps and product benchmarking — head‑to‑head comparisons of vibration performance, optical access geometry, lowest achievable temperatures, magnet integration, and automation capabilities.

Procurement and TCO tools — RFP templates, evaluation scorecards, and total cost of ownership models that account for installation, maintenance, service contracts, and cryogen elimination benefits.

Supplier assessment matrices — qualitative and quantitative profiles for incumbent and emerging vendors focused on manufacturing maturity, customization capability, lead times, and IP ownership.

Go‑to‑market and channel playbooks — recommendations for distributors, academic consortia partnerships, and government procurement strategies, including timing around major conferences and grant cycles.

Regulatory and use‑case guidance — practical notes on classification, permitted usages in laboratory settings, and explicit cautions that these systems are intended for research and are not medical diagnostic devices.

Integration checklists — electrical, optical, and cryogenic interface guides for plugging cryostats into larger quantum stacks or spectroscopy rigs without introducing excess vibration or EMI.

Our competitive analysis focuses on vendors that shape product expectations and procurement terms across research institutions and advanced industrial labs. Several names consistently appear as leaders in product capability, channel execution, or ecosystem integration:

Montana Instruments (Bozeman, MT) — Known for cryogen‑free closed‑cycle systems optimized for low vibration and automation, with large sample spaces that facilitate complex optical and electrical experiments. Their trade show presence and continuous product refreshes make them a go‑to for teams prioritizing turnkey stability and integration.

Lake Shore Cryotronics (Westerville, OH) — Offers flexible optical access configurations across a broad spectral range and both cryogen and cryogen‑free options. Their legacy in instrumentation and measurement complements labs that need tight integration between cryogenic environments and metrology gear.

attocube systems GmbH (Haar, Germany) — Produces compact, low‑vibration closed‑cycle platforms with emphasis on magneto‑optical compatibility and rack‑friendly designs. Their product line targets customers who prioritize footprint‑efficient, mobile sub‑4K solutions.

Advanced Research Systems (Macungie, PA) — Focuses on ultra‑low drift platforms and custom flow cryostats; suitable for teams needing bespoke probe stations or complex coaxial/fiber feedthroughs integrated at procurement.

Quantum Design (San Diego, CA) — The OptiCool family demonstrates how magnet integration and optical access are converging; recent vector magnet extensions signal growing demand for combined magneto‑optical experiment capabilities.

Oxford Instruments / Andor (Abingdon, UK) — Provides established spectroscopy and microscopy platforms with user‑friendly loading options and strong service footprints in key research markets.

These vendor profiles include recent tactical moves — new vector magnet launches, trade show positioning, and notable university procurements — which we map in the report to likely product roadmap trajectories and supply implications for 2026.

Technology substitution: The shift away from liquid cryogens toward closed‑cycle pulse tube and GM cryocoolers changes installation requirements, operating expenses, and safety protocols.

Demand concentration: Research programs in quantum information and magneto‑optical science are the primary growth drivers; strategic partnerships with national labs and university consortia accelerate adoption but create dependency on grant cycles.

Service and aftermarket: As systems grow more complex, service, calibration, and rapid spare delivery become competitive differentiators. OEMs that invest in remote diagnostics and preventive maintenance capture higher lifetime value.

Regulatory clarity: These systems are generally classified as standard laboratory equipment and do not require medical device approvals — a point that simplifies procurement for research organizations but also limits alternative reimbursement pathways.

Supply chain and lead times: Recent high‑profile procurements and trade show product rollouts indicate tightening lead times for certain high‑spec configurations; buyers must balance custom requirements against available inventory windows.

Adopt an integration‑first procurement specification: Prioritize vendor evaluations on interface compatibility (fiber, RF, magnet ports) and vibration isolation performance rather than lowest upfront price.

Lock multi‑year service agreements early: Given equipment complexity and the premium on uptime in quantum experiments, budget for extended maintenance that includes remote diagnostics and prioritized spare shipments.

Explore strategic OEM partnerships: For companies supplying components to instrument makers, 2026 is an opportunity to embed nanopositioning, low‑noise electronics, or cryocooler modules upstream of system assembly.

Coordinate procurement with funding timelines: Align capital orders with grant cycles and major conference product releases to secure trade‑in or bundle offers and to ensure compatibility with the latest vector magnet or automation options.

Stress‑test supply scenarios: Use the report’s scenario models to understand how shifts in R&D funding or a sudden increase in demand for high‑field optical experiments affect lead times and TCO.

Design for serviceability: When drafting specs, require modular subassemblies and clear spare parts lists to reduce downtime and mitigate the impact of supplier concentration.

This article outlines the strategic contours executives need to consider entering 2026, but the actionable edge resides in granular outputs that PW Consulting retains for the full report: complete segmentation tables, supplier scorecards with weighted scoring, downloadable RFP templates, TCO calculators calibrated to lab usage profiles, and the detailed scenario matrices that translate market growth into procurement timelines.

If your 2026 plan includes capex for quantum platforms, spectroscopy upgrades, or magneto‑optical facilities, this research provides the frameworks and tools to convert market momentum into defensible procurement and partnership decisions — without guesswork.

PW Consulting recommends that stakeholders schedule a briefing with our senior analysts to run a tailored impact analysis for their organization. The full report contains the proprietary breakdowns and operational templates essential for implementing the recommendations summarized here. Visit the report landing page to download the executive summary and to arrange a private consultation.

For detailed analysis of this topic, please visit the official page:Worldwide Cryostation Optical Cryostat Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com