Worldwide Custom Gene Synthesis Service Market: Strategic Outlook for 2026 Decision-Makers

Executive snapshot

PW Consulting’s latest market study on the Worldwide Custom Gene Synthesis Service Market synthesizes five years of historical performance and a seven-year forecast horizon to deliver an actionable strategic playbook for executives entering 2026. At the macro level, the market has more than doubled since 2020 and, driven by accelerating demand across biopharma, synthetic biology and research, is projected to sustain strong growth with a compound annual growth rate of 17.02% across our forecast window. By the end of the base year (2025) the market reached the multi‑billion USD scale and is forecast to expand markedly through 2032 under multiple demand and regulatory scenarios.

Worldwide Custom Gene Synthesis Service Market

Why this report matters to 2026 strategy

- Timing: 2026 is a decision inflection point — capital investments, capacity commitments, and commercial partnerships initiated now will hit critical milestones as demand scales and regulation tightens.

- Actionability: The study is built for executives who need executable recommendations (vendor selection frameworks, contract negotiation levers, compliance gap analyses), not just high‑level forecasts.

- Risk‑aware growth: Our analysis marries forward revenue trajectories with a detailed evaluation of regulatory, technological and supply‑chain risks that will shape commercial outcomes in 2026–2032.

Market trajectory and what the macro numbers conceal

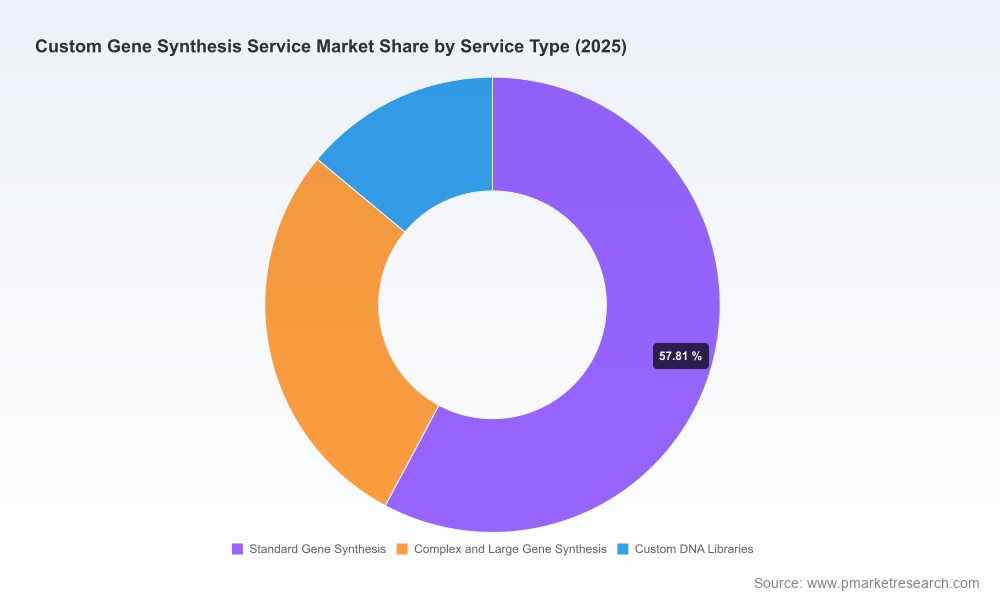

At a high level, the sector’s strong 17.02% CAGR reflects three concurrent dynamics: rising outsourcing of gene synthesis by biopharma and biotech firms, expansion of synthetic biology in industrial and agricultural R&D, and the commoditization of routine gene services alongside premium demand for complex constructs and GMP‑grade material. While headline growth is compelling, decision‑makers must look beyond aggregate figures. The market is stratifying: high‑velocity, low‑margin standard gene services coexist with specialist, higher‑margin offerings (e.g., GMP‑grade DNA for clinical trials, complex long‑range constructs and large custom libraries). Our report exposes the operational and commercial inflection points within that stratification and prescribes tailored responses for suppliers and buyers alike.

Worldwide Custom Gene Synthesis Service Market

Strategic implications for 2026 planning

- Capacity and lead‑time engineering: Rapid turnaround services are becoming table stakes for discovery partnerships. Investing in automation, standardized workflows and validated supply chains will be essential to keep lead times competitive without sacrificing quality.

- Regulatory readiness as a commercial differentiator: Compliance with evolving screening and quality standards is no longer a cost center — it is a gatekeeper to enterprise customers and to participation in clinical supply chains. Firms that operationalize screening and documentation will win larger contracts and premium pricing.

- Product portfolio optimization: Companies should rationalize product tiers (standard vs complex vs GMP) and align pricing and go‑to‑market models to avoid margin compression—this includes clear SLAs, warranty language and optionality around sequence verification services.

- Partnerships and vertical integration: Strategic alliances (contract manufacturers, cold‑chain logistics, analytical service providers) reduce go‑to‑market friction. Conversely, vertical integration into GMP manufacturing can unlock higher‑value clinical markets but requires disciplined investment and compliance execution.

Competition: who matters and how to play

The market is competitive and moderately concentrated, with a subset of global providers commanding a disproportionate share of enterprise demand. Our competitive review profiles the full competitive set but highlights a core group of market leaders and specialty players whose strategies are shaping customer expectations and pricing dynamics. Key observations for 2026:

Worldwide Custom Gene Synthesis Service Market

- Platform scale and differentiation: Players with proprietary synthesis platforms (for example, silicon‑based high‑throughput synthesis) are leveraging throughput economics to win large synthetic biology and biopharma projects. These companies are best positioned to offer economies of scale for high-volume, standardized needs.

- Speed and reliability as sales levers: Several providers emphasize very rapid delivery windows for routine constructs; those offerings are resonating with discovery teams focused on iterative experiments and time to data.

- Specialist, high‑value service providers: Firms that focus on complex sequences, high GC content, repeat regions, or GMP‑grade supply have carved out defensible niches where technical expertise and quality systems are primary switching costs.

- Emerging regional strategy: Select players are investing in regional manufacturing and regulatory readiness to address localized demand, clinical trial supply, and compliance expectations — a trend that will accelerate in 2026.

Profiles in competitive positioning (illustrative)

- Established global integrators that combine speed, codon optimization and end‑to‑end cloning solutions—they maintain broad portfolios for both discovery and translational programs.

- High‑throughput platform specialists using proprietary synthesis chemistry and automation to serve large‑scale synthetic biology and industrial customers.

- GMP‑focused providers and contract manufacturers targeting clinical grade DNA and gene therapy supply chains, increasingly certified to meet regulatory expectations.

- Cost‑competitive regional providers that supply routine constructs and fragment services to academic and small biotech customers, competing on turnaround and price.

Regulatory and standards landscape — a front‑stage concern in 2026

Regulation is reshaping commercial practice. Recent policy moves and international standards are creating concrete obligations for providers and customers alike. Key items influencing 2026 strategy include:

- Order and sequence screening frameworks that require providers to implement customer verification and sequence‑of‑concern (SOC) screening protocols. Operationalizing these controls is already a procurement prerequisite for many enterprise customers.

- Emerging international standards that codify production and quality control expectations for synthesized gene products — firms will need documented management systems to demonstrate compliance during customer audits and regulatory inspections.

- Voluntary consortium protocols that continue to set de‑facto industry norms for customer and sequence screening. Adherence to such protocols both mitigates biosafety risk and signals credibility to enterprise buyers.

For buyers: insist on audit trails, screening logs, and supplier self‑attestations as contractual prerequisites. For suppliers: embed screening and traceability into order workflows and consider third‑party certification to reduce friction with cautious customers.

Recent market developments that matter (2024–2025)

- New service launches and platform innovations have compressed lead times and expanded the envelope of manufacturable constructs — affecting buyer expectations for speed versus complexity trade‑offs.

- Strategic acquisitions and facility investments have increased regional capacity and GMP availability in target markets, altering local competitive dynamics.

- Regulatory certifications and standards adoptions are converting into commercial advantage for certified suppliers that can serve clinical pipelines and regulated programs.

Report contents — practical tools and modules

PW Consulting’s report is constructed for decision execution. It includes:

- Demand modeling and scenario analysis (base, upside, downside) that translates macro growth into supplier capacity needs and addressable segments across the forecast period.

- Vendor selection and RFP templates that operationalize compliance, QC, and pricing levers for procurement teams.

- Commercial playbooks for suppliers (pricing architecture, product tiering, service bundles) tailored by customer persona (biopharma, academia, CROs, diagnostics).

- Compliance readiness checklists, audit evidence templates and sample contractual clauses to accelerate safe market entry into regulated clinical supply chains.

- M&A and partnership screening frameworks identifying target profiles, integration risk drivers, and valuation sensitivities for 2026 deal making.

How to use this study in 2026 — three priority moves

- Buyers (biopharma, CROs, diagnostic firms): run a supplier rationalization using our vendor scorecard to consolidate spend with 2–3 strategic partners that meet your discovery and translational pipelines’ quality and compliance requirements.

- Suppliers: prioritize investments that reduce cost‑per‑construct for standard products while protecting margins on complex/GMP services through certification and differentiation.

- Investors and M&A teams: use our scenario outputs to stress‑test capital deployment cases and to identify targets that provide rapid access to GMP capacity, regional footprint, or proprietary synthesis platforms.

Risks, blindspots and monitoring triggers

Three monitoring triggers should be on every executive dashboard in 2026:

- Regulatory tightening (e.g., narrower oligo screening thresholds or mandatory provider registries) that could raise compliance costs and create entry barriers.

- Platform disruptions (novel cell‑free production methods, sequencing‑informed error correction) that materially shift unit economics and supplier competitive hierarchies.

- Supply chain shocks affecting raw material or reagent availability which could impact lead times and pricing; hedging supplier relationships and maintaining qualified secondary vendors is prudent.

Conclusion and next step

PW Consulting’s Worldwide Custom Gene Synthesis Service Market report gives executives the strategic context, operational tools and risk frameworks required to make high‑confidence decisions in 2026. The market’s robust growth trajectory presents significant opportunity, yet the interplay of technological change and tightening regulation demands disciplined, forward‑looking responses. Our work offers a roadmap for capturing upside while managing biosafety, quality and commercial risk.

For the full dataset, regional and end‑use segmentation, vendor benchmarking tables and the proprietary scorecards that underpin our recommendations, visit the full report page and download the executive packet.

For detailed analysis of this topic, please visit the official page:Worldwide Custom Gene Synthesis Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com