Water Bath Disinfectant Market to Reach USD 661 Million by 2034, Growing at a CAGR of 4.8%

Other |

2026-07-10 09:59:37

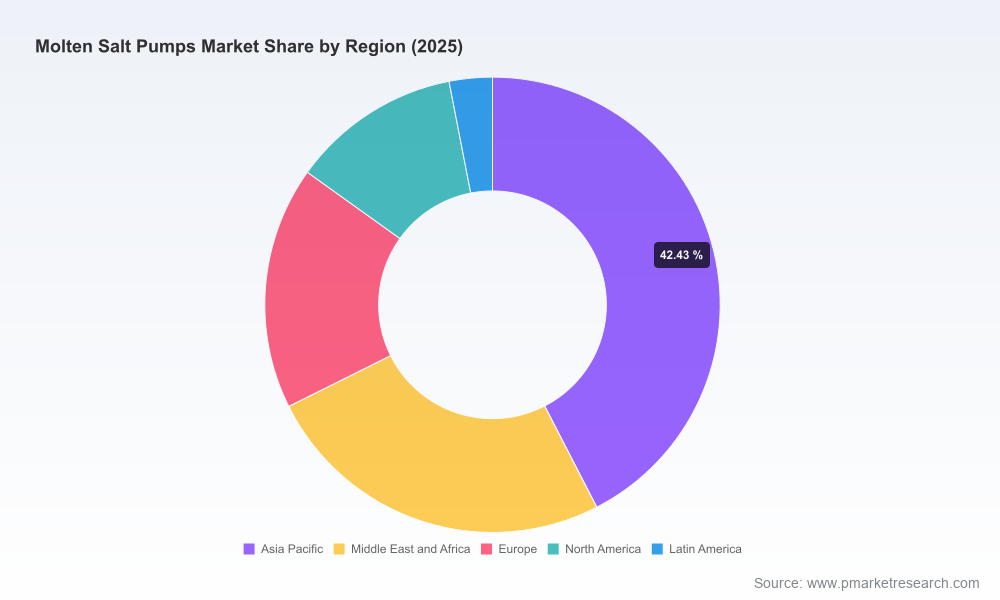

The molten salt pumps market has entered an inflection phase. After a period of steady growth through the early 2020s, the global market reached approximately USD 834.1 Million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of about 9.1% through 2032, reaching roughly USD 1.53 Billion by the end of the forecast horizon. That trajectory reflects simultaneous expansion across concentrated solar power (CSP) with integrated thermal energy storage, a rising pipeline of molten salt reactor demonstrators, and expanding industrial high‑temperature processes. For executives planning capital allocation, procurement, or R&D investments in 2026, the question is not whether to participate — it is how to position to capture value while managing technical and supply risks.

Worldwide Molten Salt Pumps Market

Technology deployment at scale: CSP plants with thermal storage and pilot molten salt reactors are moving from demonstration to pre-commercial stages, raising demand for pumps engineered for continuous high‑temperature service and long operational lifetimes.

Worldwide Molten Salt Pumps Market

Materials and reliability engineering are primary cost drivers: designs that successfully address corrosion, high‑temperature creep, bearing life and thermal distortion materially reduce lifecycle costs and project risk.

Worldwide Molten Salt Pumps Market

Consolidation and supplier concentration: the market exhibits moderate concentration, with the top three manufacturers controlling a notable portion of revenue and the top five an even larger share—factors that influence pricing power, lead times and aftermarket service availability.

Procurement timing and total cost of ownership (TCO) planning: Given a near‑double market size over the forecast and a 9.1% CAGR, buyers should shift from lowest‑capex procurement towards TCO optimization. Prioritize suppliers with demonstrable long‑term field data and validated thermal‑distortion mitigation strategies; short‑term savings on custom high‑temperature pumps can be offset by premature failures and long downtime in remote CSP and reactor sites.

Supplier qualification and strategic sourcing: The market’s moderate concentration makes supplier risk management essential. Shortlists should combine established global OEMs with regional manufacturers that can guarantee local content, faster response times and on‑site services. Expect lead times to compress for validated configurations—early engagement with preferred suppliers yields negotiating leverage and prioritized engineering capacity.

Materials and coatings as differentiators: Investment cases should account for higher upfront material costs (e.g., high‑nickel alloys and advanced thermal spray or cermet coatings) because they deliver lower maintenance and longer mean time between overhaul (MTBO). Procurement specifications that mandate materials validation under intended salt chemistries and temperatures are becoming standard.

Aftermarket services and performance guarantees: OEMs that bundle monitoring, spare parts kits, and guaranteed MTBO metrics command premium contracts and reduce system integrator risk. For asset owners, long‑term service agreements tied to clear performance KPIs are an effective hedge against obsolescence and supply disruptions.

R&D partnerships and pilot projects: For vendors and strategic buyers, co‑funding long‑duration test loops and materials qualification programs accelerates de‑risking and creates preferential access to validated designs. Our research shows recent operational milestones from pilot operators are influencing buyer confidence and procurement specifications.

Our Worldwide Molten Salt Pumps Market report is structured to enable immediate, practical decisions across commercial, engineering and procurement functions. Highlights include:

A concise market sizing and forecasting model calibrated to 2020–2025 historicals and a 2026–2032 forecast. The model quantifies system‑level demand drivers, sensitivity to CSP deployment scenarios and early nuclear demonstrator schedules.

Supplier capability assessments that go beyond product brochures: production footprint, test‑loop validation, materials stacks for chloride vs. nitrate salts, aftermarket network density and demonstrated operating lifetimes. These profiles are scored against procurement criticality matrices.

Practical procurement playbooks covering specification templates, RFQ scoring rubrics, contract clauses for performance guarantees, and recommended spare‑parts inventories tailored to remote CSP and reactor contexts.

Maintenance and reliability interventions: inspection frequency recommendations, instrumentation and remote‑monitoring specifications, failure‑mode analysis with mitigation pathways, and refurbishment vs. replacement decision thresholds.

Quantified scenario analysis: how policy shifts, raw material price volatility and accelerated CSP rollouts change demand and supplier bargaining power—enabling CFOs to stress‑test capital allocation plans.

The competitive field blends legacy pump specialists, industrial OEMs transitioning into high‑temperature markets, and agile regional suppliers. Key industry participants include established European and North American names with deep CSP and petrochemical experience, specialist firms focused on molten salt systems, and a growing set of Asia‑based manufacturers serving local projects and export markets.

Selected competitive observations:

Sulzer has positioned itself as a lead supplier for CSP and energy‑storage applications, delivering both hot and cold molten salt pumps for major projects and securing recent contracts that underscore its relevance to large‑scale deployments.

Flowserve emphasizes long life and thermal management, offering wet pit and vertical turbine designs engineered for multi‑decade operation—an attractive proposition for asset owners seeking long MTBO guarantees.

Hayward Tyler and other specialist high‑temperature OEMs differentiate via custom designs for extreme environments (including liquid sodium and liquid metal experience), valuable where nuclear qualification pathways are required.

Regional players and legacy pump makers bring competitive pricing and local engineering support. For projects prioritizing speed and regional supply chains, vetted local suppliers often provide the best balance of cost and responsiveness.

Market concentration metrics indicate a moderately consolidated market: the top three firms capture a meaningful share of revenue, while the top five firms consolidate an even larger portion of the market. This structure amplifies the importance of supplier selection and long‑lead contractual protections in 2026 procurement strategies.

Material selection matters: wetted components for chloride salt service commonly deploy high‑nickel alloys (e.g., Inconel 625) and advanced coatings such as high‑velocity oxygen fuel (HVOF) NiWC cermets to resist corrosion and wear at temperatures approaching or exceeding 600°C. Specifying validated metallurgy under project‑specific chemistry and temperature profiles is non‑negotiable.

Design features that reduce thermal distortion—such as thermal mapping and specialized support geometries—are increasingly standard for long‑duration CSP and reactor pumps. Engineering firms that demonstrate comprehensive thermal‑strain testing deliver lower lifecycle risk.

Standards and regulatory trends: national programs and agencies are focusing on reliability and lifetime metrics for next‑generation CSP and reactor projects. Procurement teams should expect tighter specification requirements and certification pathways tied to public funders and generational programs.

Supply chain bottlenecks for specialty alloys and high‑performance coatings — mitigate by qualifying multiple suppliers and securing forward purchase agreements for critical raw materials.

Technical risk around long‑term salt chemistry stability — address through extended test loops, co‑funded R&D and contractual acceptance testing tied to clearly defined performance metrics.

Service and spare parts scarcity in remote installations — build strategic spare kits, regional maintenance partnerships and OEM performance SLAs into procurement contracts.

Operational milestones from pilot operators have begun to de‑risk core components: independent test loops running continuous periods validate materials and seals and inform MTBO expectations.

Contract awards to established OEMs for combined pump and balance‑of‑plant packages reinforce the shift toward integrated supplier solutions for large CSP and storage projects.

Our report provides the actionable playbooks, supplier due‑diligence templates, and bespoke scenario models that procurement, engineering and strategy teams need to make confident 2026 decisions. We combine technical vetting (materials and test‑loop performance), commercial intelligence (supplier capacity and concentration analysis) and financial scenario planning (TCO and sensitivity models) to reduce decision uncertainty.

Note: This release is a strategic preview. The full Worldwide Molten Salt Pumps Market report includes the granular segmentation, regional and application breakdowns, proprietary supplier scoring matrices and downloadable model files used to generate the forecasts. Those segment‑level numbers and our proprietary assumptions are intentionally reserved for report subscribers to preserve the commercial value of the dataset.

Reframe procurement around TCO and service guarantees, not unit price alone.

Prioritize supplier validation for materials, thermal‑distortion control and field‑demonstrated MTBO.

Lock in strategic supply and spare parts agreements to hedge raw‑material and lead‑time risk in 2026 projects.

Consider co‑funded test loops or pilot programs to accelerate qualification and obtain preferential supplier access.

PW Consulting’s full report is designed to equip executive teams to translate the projected market expansion into concrete procurement, engineering and investment actions. For project teams preparing 2026 procurement cycles, the time to act is now—early partnership and supplier qualification will determine which projects realize predicted performance and which will be caught by avoidable failures.

For detailed analysis of this topic, please visit the official page:Worldwide Molten Salt Pumps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com