Worldwide Electronic-Grade Helium Market: Strategic Imperatives for 2026 Decision‑Makers

PW Consulting — Executive Briefing on the 2026 Planning Horizon

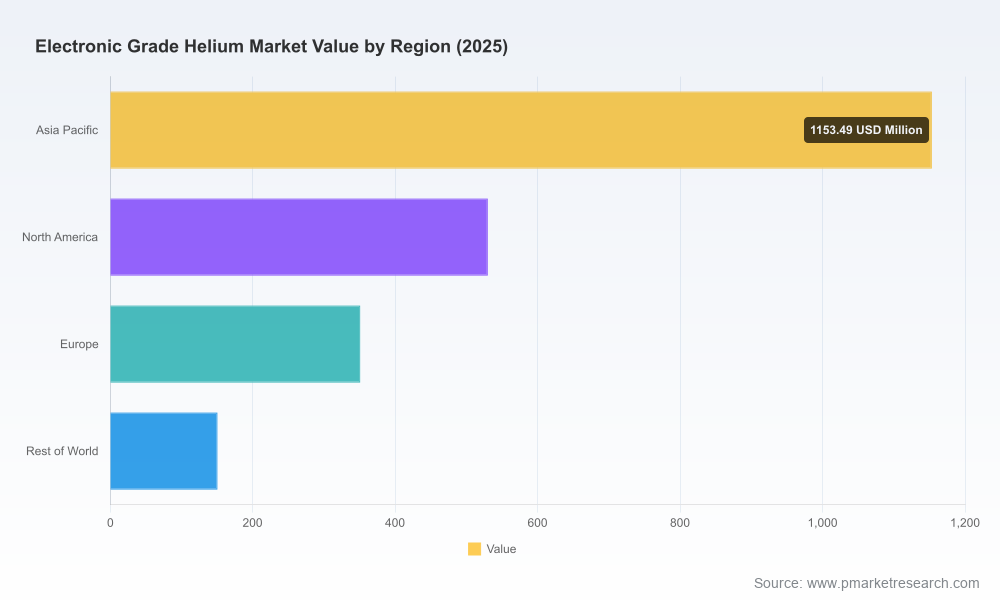

PW Consulting’s newest market study on the Worldwide Electronic‑Grade Helium Market provides a forward‑looking, decision‑centric framework for executives navigating one of the electronics supply chain’s most volatile raw materials. Anchored on a 2025 base year and a 2026–2032 forecast window, the study quantifies the industry’s recovery and structural growth: the global electronic‑grade helium market reached approximately USD 2,185.5 Million in 2025 and, at a compound annual growth rate (CAGR) of 8.15% through 2032, is projected to approach USD 3,782.13 Million by the end of the forecast period. These headline figures matter because they compress both rising demand from advanced semiconductor nodes and systemic supply risks into a single planning metric for procurement, operations, and capital allocation decisions in 2026.

Worldwide Electronic Grade Helium Market

Why this report matters for 2026 strategy

- Actionable risk assessment: The report translates macro supply shocks and geopolitical tail‑risks into discrete operational scenarios that procurement and supply‑chain teams can stress‑test in calendar‑year planning.

- Investment prioritization: Guided capex levers and ROI models help manufacturing leaders decide when to fund on‑site recovery, onshore storage, or long‑term supply agreements versus spot purchases.

- Supplier selection and contracting: Our competitive map and supplier playbooks provide negotiation anchors for multi‑year off‑take, transfill access, and contingency clauses—critical when price volatility can swing by multiples over quarters.

- Technology and reuse pathways: The study quantifies the potential operational impact of helium‑recovery systems and closed‑loop process architectures, offering financial breakeven horizons under multiple price and availability scenarios.

Context: Structural growth meets acute supply shocks

The market’s mid‑to‑long term trajectory is underpinned by secular demand from semiconductor fabrication—where ultra‑high‑purity helium (6N and above) plays essential roles in cooling, atmosphere control, and leak detection for advanced nodes—and by expanding volumes required in flat‑panel, optical fiber and photovoltaic manufacturing. That secular demand is layered atop a concentrated supply base: the top three suppliers account for a sizable portion of the market (CR3 ~62.5%), and the top five approach near‑majority control (CR5 ~78.9%). Such concentration amplifies the system’s sensitivity to upstream interruptions.

Worldwide Electronic Grade Helium Market

Early‑2026 events crystallized this systemic fragility. A force majeure at a major LNG‑linked production hub removed an estimated ~30% of global helium output destined for electronic applications, triggering spot price surges ranging roughly from 40% to 100% in affected markets. Concurrent logistical chokepoints—closures impacting key shipping lanes—exacerbated shortages for Asian chip hubs, accelerating local procurement scramble and highlighting the limits of global just‑in‑time strategies for mission‑critical gases.

Worldwide Electronic Grade Helium Market

Competitive landscape — who matters and why

- Air Liquide S.A. (Paris, France) — Global leader in industrial gases with deep purification, liquefaction and distribution capabilities. Recent investments to locate production near semiconductor clusters underscore a strategy of regionalized resilience.

- Air Products and Chemicals, Inc. (Allentown, PA, USA) — A major helium producer with an emphasis on storage/transfill networks and extraction innovation. Their integrated supply‑chain assets make them a go‑to for long‑term contracts and engineered logistics solutions.

- Linde plc (Woking, UK operations) — One of the largest helium processors, with a diversified sourcing mix and large‑scale processing assets that serve global electronics customers; their capacity decisions have immediate market impact.

- Taiyo Nippon Sanso Corporation / MATHESON (Tokyo / New Jersey) — A specialist in ultra‑high‑purity electronics gas, holding rights to multiple helium sources and certified supply streams for critical semiconductor applications.

- Messer SE & Co. KGaA (Bad Soden, Germany) — Regional and global supplier with targeted electronic‑grade offerings across manufacturing geographies.

- Exxon Mobil Corporation (Irving, TX, USA) — Operator of major helium production assets; their upstream decisions (e.g., plant maintenance scheduling) directly affect global availability.

- QatarEnergy / Qatargas (Doha, Qatar) — Historically a large volume source via LNG facilities; operational disruptions at these facilities cascade through global supply and pricing dynamics.

- Gazprom (Moscow, Russia) — Produces helium as a byproduct of natural gas operations, representing an alternative stream subject to broader geopolitical considerations.

Recent developments reflect the market’s dynamic rebalancing. Leading suppliers have accelerated regional investments—such as a new facility opened to serve semiconductor manufacturers near a major Asian port—while emerging suppliers in China achieved certifications and mass production of ultra‑high‑purity helium for electronics. These moves are not merely capacity additions; they are strategic statements about proximity, certification, and customer intimacy. Collectively, they form part of an accelerated re‑regionalization trend that PW Consulting maps and scores in the report.

Practical contents of the report — what you will find inside

- Comprehensive market sizing (2020–2025 historical series and 2026–2032 forecasts) expressed in USD Million and reconciled across demand drivers.

- Scenario modeling that converts geopolitical, logistic and production shocks into procurement and production impacts across a range of recovery timelines.

- Supplier due‑diligence templates and negotiation playbooks tailored to electronic‑grade helium purchases (contract terms, minimum viable inventory, force majeure clauses, certification audits).

- Capex and opex models for onsite recovery, onshore storage, and alternative sourcing strategies, with sensitivity analyses under multiple price‑shock scenarios.

- Regulatory and geopolitical heat maps identifying transport chokepoints, strategic chokehold facilities, and country‑level risks to supply continuity.

- Technology assessment of helium recovery and purification systems (including reported recovery rates and China’s domestic capacity developments), and the operational levers required to attain closed‑loop efficiencies.

- Executive decision matrices that translate market intelligence into 30/90/180‑day tactical actions and 1–3 year strategic initiatives.

Strategic recommendations for 2026 planning

- Adopt multi‑vector sourcing: Short‑term spot purchases should be complemented by staggered multi‑year contracts with geographically diversified suppliers and transfill access to reduce single‑source exposure.

- Prioritize proximity and certification: For fabs and high‑precision electronics sites, suppliers with nearby transfill/storage and recognized semiconductor certifications offer fewer logistics failure modes.

- Invest in reuse and recovery: Where throughput economics allow, rapid deployment of helium recovery systems yields favorable payback under stressed price environments—PW’s models show materially shorter payback periods at current volatility levels.

- Design inventory guardrails: Move from lean inventories for non‑critical inputs to tiered buffers for mission‑critical gases; define triggers tied to spot spreads and supplier alerts to automate replenishment.

- Stress‑test scenarios: Build scenario playbooks that map a 30% supply outage, maritime transit interruptions, and rapid demand spikes—each with a defined set of tactical actions for procurement, production scheduling and customer communications.

- Engage in collaborative risk sharing: Explore supplier co‑investment in regional storage or recovery projects to align incentives for resilience and cost stability.

What we intentionally hold back — and why you should read the full report

Consistent with our “trailer” approach, this briefing surfaces the strategic implications, headline market sizing, concentration metrics, and the key supplier plays that will shape 2026 decision cycles. To preserve the competitive value of our modeling and to compel rigorous planning, we do not publish detailed segment‑by‑segment revenue splits or granular regional/application breakouts in this press release. The comprehensive dataset, proprietary scenario outputs, supplier scoring matrices and executable contract language are available in the full report—resources that procurement teams, CFOs and plant operations leaders will need to operationalize the strategies summarized here.

Closing — timing and next steps

For organizations defining 2026 budgets and operational plans, helium is no longer a soft commodity: it is a strategic input requiring dedicated governance. With market momentum heading toward an estimated USD 3.8 billion by 2032 at an 8.15% CAGR, coupled with concentrated supplier control and recent large‑scale disruptions, the cost of inaction is measurable in production downtime, expedited logistics premiums, and lost customer commitments.

PW Consulting’s Worldwide Electronic‑Grade Helium Market report translates these risks into prioritized actions and quantifiable investment cases. Procurement, supply‑chain, and technology leaders should consult the full study to access the models, procurement playbooks, and supplier diligence tools required to build resilient, cost‑effective helium programs for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Electronic Grade Helium Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com