Floriculture Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-07-01 08:42:47

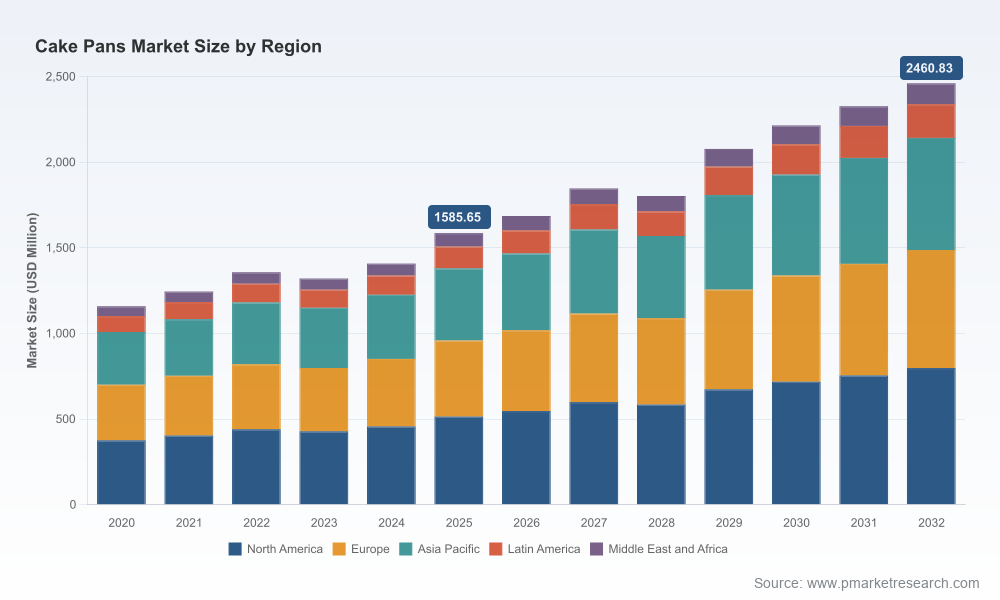

The global cake pans market has entered a period of steady, structurally-backed expansion. PW Consulting’s new Worldwide Cake Pans Market report (base year 2025, forecast period 2026–2032) synthesizes proprietary primary research, supply-chain modeling, and commercial benchmarking to equip executives with the evidence and playbooks needed to convert opportunity into market-leading performance in 2026. The market reached approximately USD 1,586 million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 6.48% in the 2026–2032 window, reaching roughly USD 2,461 million by 2032. This release is designed as a strategic toolkit — rich in operational guidance and decision-ready analysis — while intentionally reserving the full granular segmentation tables for the report itself.

Worldwide Cake Pans Market

Translate macro growth into commercial priorities: understand which product archetypes and channel plays are accelerating demand, and which are stalling, so you can allocate marketing and SKU investment efficiently.

Worldwide Cake Pans Market

De-risk supply chains under new trade regimes: with evolving tariffs and raw-material volatility, this report quantifies exposure and prescribes sourcing and hedging responses tailored to bakeware manufacturers and distributors.

Worldwide Cake Pans Market

Optimize portfolio and pricing: use our elasticity models and SKU rationalization framework to lift margin without sacrificing shelf presence.

Plan inorganic growth with precision: our M&A screens and integration playbooks point to targets and integration pitfalls relevant to both strategic and private-equity buyers.

We built the report around the needs of executives preparing plans for 2026 execution. Key deliverables include:

A clear-sized market model (historical 2020–2025 and a 2026–2032 forecast) with scenario variants for inflation, raw-material shocks, and channel shift.

Commercial playbooks for major routes-to-market (retail, online, specialty, DTC) that feature customer acquisition KPIs, promotional trade-offs, and assortment recommendations.

Material and supplier risk matrices covering aluminum, steel, silicone, ceramic and composite inputs — with negotiation templates, lead-time mitigation options, and total-cost-of-ownership calculators.

Competitive benchmarking: qualitative and quantitative profiles of the sector’s leading manufacturers and brands, plus go-to-market maps highlighting incumbents’ strategic moats.

SKU rationalization and margin-migration tools that let you run “what-if” decisions at brand and channel level without re-running full financial models.

Regulatory compliance checklist and quality-assurance scorecards tailored for baked-goods partners and private-label relationships.

M&A diligence pack and integration playbook focused on operational synergies, cross-sell pathways, and rapid cost-capture opportunities.

The cake pans market demonstrates resilient growth following the demand shocks of the early 2020s. PW Consulting’s topline model shows expansion from just over USD 1.15 billion in 2020 to approximately USD 1.59 billion in 2025, followed by an expected broad-based acceleration that lifts the market to roughly USD 2.46 billion by 2032 at a 6.48% CAGR. This trajectory underscores two concurrent dynamics: continued consumer appetite for at-home and artisan baking formats, and a step-up in premiumization and specialized formats that command higher ASPs (average selling prices).

The market remains fragmented, with well-established heritage brands coexisting alongside specialized commercial suppliers and efficient contract manufacturers. The PW report profiles the following firms and evaluates their strategic postures:

Nordic Ware (United States) — known for durable aluminum designs and iconic Bundt shapes; brand strength in home-baking occasions and seasonal gifting.

USA Pan (United States) — commercial-grade aluminized steel with robust non-stick finishes; attractive for bakery clients seeking durability and throughput.

Fat Daddio's (United States) — anodized aluminum specialist with strong channel pull among serious home bakers and small commercial operations.

Emile Henry (France) — ceramic expertise; premium heat-retention positioning aligned to artisan and home-convival applications.

Kaiser Bakeware (Germany) — precision-engineered bakeware; strength lies in quality perception and consistency across formats.

Wilton Brands (United States) — product innovation and decorating ecosystem; advantage in differentiated, themed, and seasonal SKUs.

American Pan & Parrish Magic Line (United States) — industrial- and professional-focused suppliers with scale in sheet and stock pan production.

Calphalon & Le Creuset — premium, performance-oriented cook/bake brands that command pricing premium through material and brand equity.

Wuxi Hongbei Bakeware Co., Ltd. (China) — contract manufacturing and custom-production capabilities supporting private-label and supply-chain flexibility.

Our competitive matrices evaluate product breadth, channel strength, manufacturing footprint, and cost competitiveness — enabling rapid identification of white spaces for new entrants and consolidation targets for incumbents.

Several near-term developments materially affect 2026 strategic choices:

Quality and compliance risk: a February 2026 Class I recall of certain cake mixes underscores the reputational and legal exposure that can ripple through brand owners, co-packers, and their bakeware suppliers. Our due-diligence checklist and supplier audit protocols address this exposure directly.

Commodity and input volatility: agricultural and commodity price movements — exemplified by elevated wheat prices and related inflationary pressure on the broader baking ecosystem — are signaling higher working-capital needs for downstream partners and changing consumer price sensitivity. While wheat is not a raw material for pans, the broader food inflation dynamic alters demand patterns for baked goods and influences retailer promotional behavior.

Trade policy and tariffs: new ad valorem import measures implemented in 2025 have created immediate reassessment of nearshore vs. offshore sourcing economics for metallic and silicone inputs. Our cost-to-serve and landed-cost models quantify the inflection points at which reshoring, nearshoring, or inventory hedging become value-accretive.

Labeling and cottage regulations: U.S. labeling requirements for allergens and rules for small-scale cottage food operations are changing route-to-market compliance obligations and private-label risk. We include a compliance playbook that aligns product labeling, co-packer agreements, and traceability efforts to minimize recall exposure and market disruption.

Short term (0–90 days): conduct a rapid supplier risk audit focusing on tariffs, lead times, and single-source exposures; implement mandatory QA checkpoints with top co-pack and private-label customers.

Near term (3–9 months): rework commercial promotions to protect margin using our elasticity models; resegment assortments across channels and accelerate DTC pilots for premium SKUs with higher contribution margins.

Medium term (9–18 months): pursue targeted procurement consolidation and nearshoring for high-cost input families; invest in product innovation (material finishes, modular pans, reusable packaging) to capture premiumization tailwinds.

M&A and partnership agenda: use our M&A screen to evaluate tuck-ins that deliver manufacturing capacity, channel access, or proprietary finishing technologies — prioritize deals where operational synergies can be captured within 12 months.

Regulatory & quality build: deploy traceability for co-pack arrangements, update labeling practices to exceed minimum allergen transparency requirements, and institute rolling recall drills.

Clients receive both the analytical backbone and the execution playbooks. Options include standalone report purchase (with full segmentation and downloadable models), bespoke deep dives (region-, material-, or channel-specific), integration support for M&A transactions, and implementation projects combining procurement, commercial, and operations teams. Where clients require it, we supply scenario-ready financial models that can be embedded into enterprise planning systems.

PW Consulting’s Worldwide Cake Pans Market report is intentionally structured to give leaders immediate, executable guidance while reserving the granular segmentation tables and proprietary datasets for report subscribers. For access to full region, material-type, and channel splits — and to license our dealer- and SKU-level models — please consult the report landing page or contact a PW Consulting industry lead. The decisions you make in 2026 will determine who captures the premiumization and channel-shift gains; this report is designed to make those decisions faster, clearer, and less risky.

For detailed analysis of this topic, please visit the official page:Worldwide Cake Pans Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com