Microcarrier Market Research Report with Competitive Analysis and Insights

Art |

2026-06-19 10:38:04

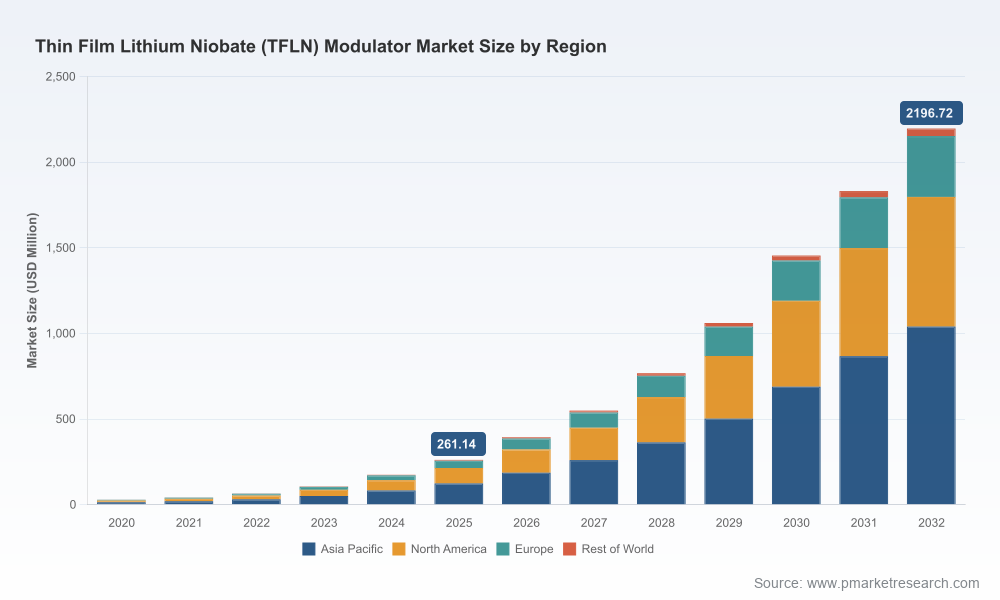

PW Consulting’s latest market study—base year 2025, forecast 2026–2032—frames Thin Film Lithium Niobate (TFLN) modulators as one of the fastest‑growing segments in photonics. The global market has expanded rapidly from a modest base in 2020 to an estimated USD 261.14 Million (base year 2025), and our revenue model projects a continued compound annual growth of 35.53% through 2032, reaching a multi‑billion-dollar opportunity by the end of the decade (our 2032 forecast: USD 2,196.72 Million). This briefing summarizes the strategic value of the full report for 2026 decision cycles, emphasizing what to act on now—and what the full study contains if you need transaction‑grade detail.

Worldwide Thin Film Lithium Niobate (TFLN) Modulator Market

Performance acceleration: TFLN modulators now routinely achieve bandwidths and drive efficiencies that materially change system architectures for datacenter interconnects, next‑generation telecoms, and coherent optical engines used in AI networking. These device‑level gains translate directly into system‑level cost and power improvements when adopted at scale.

Worldwide Thin Film Lithium Niobate (TFLN) Modulator Market

Productization and foundry momentum: 2024–2026 has seen the transition from lab demos to production‑grade wafers and packaged modules. Foundry services and PDK availability are hitting inflection points that enable design‑to‑production cycles—altering time‑to‑market for OEMs that secure early access.

Worldwide Thin Film Lithium Niobate (TFLN) Modulator Market

Concentration and competitive positioning: The supplier landscape is concentrated—top providers hold a dominant share of current revenue, creating a supplier‑selection imperative for buyers and an M&A playbook for investors looking to consolidate capability along the stack.

The market trajectory is nonlinear: the step from USD 261.14 Million in 2025 to a projected USD 393.62 Million in 2026 captures the near‑term acceleration driven by datacenter and AI interconnect pilot deployments, while the long‑term model (35.53% CAGR through 2032) captures broader adoption across telecom upgrades, quantum sensing, and aerospace/defense niches. For corporate strategists this creates three decision windows in 2026:

Protect and secure critical supply: lock in foundry capacity and wafer supply to support 2026–2027 product ramps.

Invest selectively in integration: fund packaging, test, and PDK co‑development to shorten qualification timelines.

Position for scale M&A or partnerships in 2027–2028 when demand profiles and unit economics will be clearer.

Across the value chain, three supplier types are emerging: production‑grade foundries and PDK providers; vertically integrated device manufacturers (IDMs); and system‑oriented module/packaging specialists. Key players illustrate each archetype:

HyperLight Corporation (Cambridge, MA)—a research‑spinout turned production player. Their TFLN Chiplet™ PICs and ultra‑high‑bandwidth packaged modulators (announced product launches in 2026) demonstrate a platform approach oriented to AI interconnects. Their recent partnerships with established wafer fabs signal a strategy to trade IP and design leadership for manufacturing scale—an instructive model for companies that lack fabrication assets.

Lightium AG (Schlieren, Switzerland)—positioned as a production foundry with wafer scale capability and PDK support across multiple wavelength bands. Their consortium activity and funding trajectories suggest an ambition to act as a European/Western foundry anchor—important for geo‑diversified procurement strategies.

Liobate Technologies, Ori‑Chip, Quantum Computing Inc., Rofea, AFR, Agiltron, Neon—represent a mix of IDMs and component specialists with growing portfolios spanning intensity, phase, and IQ modulators. These vendors demonstrate how product differentiation (bandwidth, Vπ, integration level) is becoming the primary non‑price competitive axis.

CCRAFT (Switzerland)—their publicized production‑ready TFLN foundry launch underscores the emergence of third‑party manufacturing capacity. For system integrators, third‑party foundries change supplier bargaining power and speed of innovation.

For buyers and investors the practical takeaway is straightforward: supplier selection in 2026 must be evaluated on three vectors—fabrication access and roadmap, PDK and IP openness, and packaging/test maturity. Our full report benchmarks each vendor across these dimensions and maps supplier strengths to concrete customer use‑cases.

Manufacturing bottlenecks and wafer scaling: high‑quality TFLN wafers and specialized cleanroom processes remain constrained. Only a handful of fabs offer the combination of yield, turnaround, and process control required for large‑scale deployment—making early capacity commitments a risk mitigation priority.

Equipment and process transition: industry momentum toward DUV stepper lithography on TFLN wafers (replacing slower e‑beam flows) is enabling higher yields and lower losses at scale. Companies that align with DUV‑capable foundries will have shorter paths to >110 GHz devices with manufacturable propagation loss figures.

Standards and interoperability: progress on PDKs, waveguide, and coupler standards is reducing integration friction—but the pace of standardization varies by region and consortium, creating timing risk for multi‑region product launches.

Geopolitics and regional supply development: localized pilot production (e.g., China’s 6‑inch TFLN line) introduces both opportunity and competitive pressure; buyers should plan dual‑sourcing strategies that account for regulatory, export control, and local content dynamics.

System OEMs and hyperscalers: secure co‑development agreements that include wafer capacity and PDK access. Prioritize suppliers that offer roadmap guarantees to support higher baud rates and lower energy per bit—these will drive system‑level TCO wins in AI networks.

Component manufacturers: invest in packaging and test automation now. The differentiation window will shift from raw device performance to total‑cost‑of‑integration—packaging IP will monetize across multiple customer segments.

Foundries and fabs: validate DUV tool flows for TFLN and establish MPW channels with clear PDK roadmaps. Foundry partners that can shorten iteration cycles will capture disproportionate design wins.

Investors and M&A teams: prioritize targets that combine IP leadership with near‑term access to scalable wafer supply or differentiated packaging. Consider bolt‑on acquisitions to secure PDKs and proprietary test flows rather than purely device portfolios.

Defense and quantum integrators: adopt a tiered qualification plan that recognizes long lead times and limited production runs; early technical collaboration can create defensible supply relationships without requiring massive upfront capital.

A calibrated market model (historical 2020–2025 and forecast 2026–2032) with scenario toggles for demand, supply constraints, and price erosion—expressed in USD Million and suitable for incorporation into board‑level models.

A vendor playbook: granular vendor scorecards across fabrication capability, IP and PDK maturity, packaging/test readiness, commercial terms, and go‑to‑market posture—designed to shorten supplier due diligence from months to weeks.

Supply‑chain heatmaps and risk matrices that pinpoint wafer capacity chokepoints, equipment dependencies (e.g., DUV steppers), and critical raw material vulnerabilities.

Actionable procurement and integration checklists, plus an ROI toolkit for evaluating TFLN adoption in datacenter, telecom, and quantum use cases—and an acquisition/partnership playbook for corporate development teams.

Scenario slides and an executive‑ready briefing tailored for boardrooms and investment committees.

We intentionally preserve certain granular segmentation tables and supplier revenue splits for report subscribers—this is a strategic “trailer”: enough depth to inform a 2026 action plan, with the detailed subsegment datasets available to clients who need transaction‑grade numbers and supplier benchmarking for procurement, M&A, or CapEx decisions.

Download the full report to access carrier‑grade datasets, vendor scorecards, and the interactive financial model.

Schedule a strategy workshop with PW Consulting to map your product, sourcing and M&A options against the three demand scenarios we model for 2026–2028.

Begin immediate supplier due diligence focused on wafer access, PDK maturity, and packaging capability—these three factors determine whether a 2026 product launch becomes a strategic advantage or an inventory liability.

In a market expanding at a multi‑decade‑defining pace, timing matters as much as technical superiority. PW Consulting’s Worldwide TFLN Modulator Market report converts the headline CAGR and growth figures into executable choices for 2026. For the full datasets, vendor profiles, and executable roadmaps referenced above, please access the report and contact our engagement team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Thin Film Lithium Niobate (TFLN) Modulator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com