U.S. Urology Devices Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-21 12:21:46

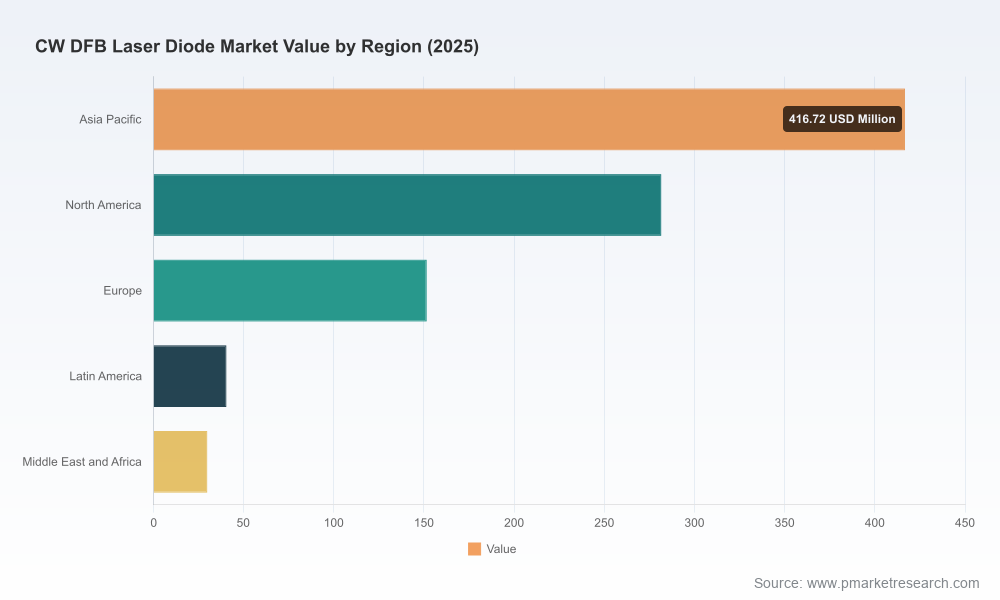

PW Consulting’s latest CW DFB Laser Diode Market brief (base year 2025) equips senior executives, procurement leads, and technology strategists with a concise, action-oriented view of where the market is today and where it will matter most through the 2026 planning window and beyond. The market has moved from a mid-single-hundred-million-dollar base in 2020 to roughly USD 920 Million in 2025, and our forecast—driven by device-level adoption in cloud infrastructure, silicon photonics integration, and next-generation sensing—points to sustained expansion through 2032 at a compound annual growth rate of approximately 8.15%. By 2032 the market is expected to exceed USD 1.5 billion, underscoring the commercial runway for suppliers and system integrators alike.

CW DFB Laser Diode Market

Timing investment vs. capacity risk: The market is at an inflection between device innovation and manufacturing scale-up. Our analysis reconciles demand drivers (notably AI-driven hyperscale networking and co-packaged optics) with current and planned wafer- and chip-level capacity to highlight where supply tightness and surplus risk will appear through 2028.

CW DFB Laser Diode Market

Supplier selection with qualification realities in mind: Component procurement for data-center transceivers and uncooled modules must balance performance, cost, and Telcordia-style reliability qualifications for non-hermetic operation up to 85°C. This report gives procurement teams a clear decision framework for preferred vendor performance vs. qualification lead times.

CW DFB Laser Diode Market

Product roadmap alignment: For platform owners evaluating 800G–1.6T transceivers, silicon photonics, or co-packaged optics (CPO), the technology trade-offs between high-output single-mode CW DFB chips, quantum-dot (QD) variants, and discrete-mode devices are mapped to real-world system objectives—reach, OSNR, thermal budget, and integration complexity.

Market-sizing & scenarios: A transparent methodology covering historical shipments (2020–2025), demand drivers, and three forward scenarios (conservative, base-case, accelerated) through 2032—each with underlying assumptions you can apply to internal forecasts.

Technology-to-application mapping: Comparative performance matrices (linewidth, output power, uncooled reliability, coupling efficiency) that translate device attributes into system-level KPIs for optical comms, sensing/LiDAR, and medical/industrial channels.

Supply chain heatmaps: Epitaxial wafer capacity, contract manufacturing footprints, and critical sub-tier vulnerabilities (notably InP wafer throughput and test/assembly bottlenecks) with mitigation playbooks for procurement and operations teams.

Vendor scorecards & partner shortlists: Objective scoring by technical fit, qualification readiness, roadmap breadth, and manufacturing scale—designed to shorten RFP cycles and support dual-sourcing strategies without sacrificing time-to-market.

Regulatory & qualification checklist: Practical guidance for Telcordia GR-468 and other qualification paths relevant to field-deployed, non-hermetic, uncooled operation up to 85°C—what to expect in test duration, failure modes to watch, and cost implications.

Commercial models & price-trajectory insights: Forward-looking unit-cost scenarios driven by capacity ramp timing, yield learning curves, and expected mix-shifts toward higher-power, uncooled parts used in silicon photonics and CPO.

The CW DFB laser diode space today is characterized by a handful of established global players complemented by specialized innovators. Market concentration shows meaningful leader presence—CR3 and CR5 metrics indicate a market where top suppliers collectively hold a large share, but there remains room for regional players and technology specialists to win designs. The practical implication for OEMs and module vendors is simple: the top-tier suppliers set qualification timetables and price floors, while agile competitors can win differentiated designs or localized supply agreements.

MACOM (Lowell, MA): Known for robust, high-power O-band devices optimized for uncooled operation and silicon-photonics interfaces. Their approach emphasizes manufacturable, thermally robust designs suited to datacom environments.

Coherent Corp. (Saxonburg, PA): Focused on high-efficiency CW DFB chips tailored to 800G/1.6T transceiver ecosystems and AI data-center needs; recent sampling of higher-output prototypes signals their intention to move aggressively into co-packaged optics and SiPh markets.

Broadcom (San Jose, CA): Offers edge-emitting solutions engineered for compatibility with external modulators and silicon photonics modules; their product strategy is tightly coupled with transceiver OEM roadmaps.

Furukawa Electric (Tokyo, Japan): A manufacturing-scale competitor actively expanding capacity to serve data-center demand. Their announced plant expansions—targeting substantial capacity increases—are a structural factor for future supply balances.

Innolume (Dortmund, Germany) & DenseLight (Singapore): Represent capability differentiation—QD-based high-power options and InP-based high-output chips respectively—positioned to capture premium, performance-sensitive applications.

Specialists and distributors (Eblana, SemiNex, Frankfurt Laser, RPMC): These players fill niche needs—single-frequency sources for sensing, mid-IR coverage, or distribution and integration services—often accelerating customer time-to-market for non-standard specifications.

Recent industry moves reinforce the dual themes of capability push and capacity build. Notable developments in 2025 included capacity expansion announcements from major manufacturers, product sampling of multi-hundred-milliwatt CW prototypes for co-packaging, and multiple new product introductions from regional vendors targeting uncooled O-band operation. These shifts are material to decision-makers planning procurement or capital investments in 2026: sampling pipelines and factory ramp schedules will determine who can meet aggressive module delivery timelines.

Wafer-level capacity is the leading near-term constraint. InP epitaxy and chip fabrication throughput dictate the pace at which high-power devices can be delivered; announced fabs and expansions will change balances but introduce ramp and yield uncertainty.

Qualification lead times matter. Telcordia GR-468-style reliability for non-hermetic, uncooled operation to 85°C is a gating factor for many data-center deployments—budget and schedule accordingly.

Integration choices shift risk. Choosing a proven vendor with immediate qualification capability reduces launch risk but can limit architectural experimentation. Conversely, partnering with a technology-intensive newcomer can yield performance gains but demands deeper co-development and longer validation cycles.

Establish a 24–36 month supplier qualification roadmap. Start now with dual-track engagement: (1) an “availability” track with large, qualified suppliers to secure baseline volumes, and (2) an “innovation” track with specialist vendors to lock in next-generation performance features.

Layer procurement with contingent capacity clauses. Given announced capacity expansions and variability in ramp yields, contracting that ties pricing and delivery to verified performance milestones reduces exposure to shortages while preserving upside.

Build internal test and qualification capability. Wherever possible, augment vendor testing with in-house reliability and thermo-optical validation to shorten iteration cycles and gain negotiating leverage.

Prioritize strategic partnerships over simple procurement. For customers targeting CPO or tight silicon-photonics integration, consider co-development agreements that align roadmaps and secure preferential allocation during wafer ramp periods.

Monitor technology signals closely. Product samplings, high-power CW demonstrations, and QD performance claims are near-term indicators of which suppliers will win design-ins. Maintain an intelligence process to convert product samplings into sourcing decisions.

This article highlights the strategic contours and practical implications executives need for 2026 planning, but deliberately omits the granular segment-level tables and region-by-application breakdowns that are central to procurement and investment due diligence. The full CW DFB Laser Diode Market report contains detailed segment forecasts, price curves, supplier revenue share models, and downloadable scorecards that translate the high-level guidance above into executable procurement and investment actions.

For teams preparing budgets, RFPs, or M&A screens in 2026, the full dataset and supplier-by-supplier benchmarking in our report provide the granular inputs needed to convert strategic intent into contracts and capital allocation. PW Consulting’s advisory team is available to translate the report’s scenarios into bespoke sourcing strategies, qualification roadmaps, and investment stress-tests tailored to your risk appetite and time-to-market constraints.

Contact PW Consulting to access the full CW DFB Laser Diode Market report and supporting datasets to underpin your 2026 plans. The headline is clear: the market is growing, supplier dynamics are shifting, and 2026 decisions will define who captures the most value in the next wave of optical and sensing architectures.

For detailed analysis of this topic, please visit the official page:CW DFB Laser Diode Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com