Worldwide Aesthetic Phototherapy Lamps Market — Strategic Outlook for 2026

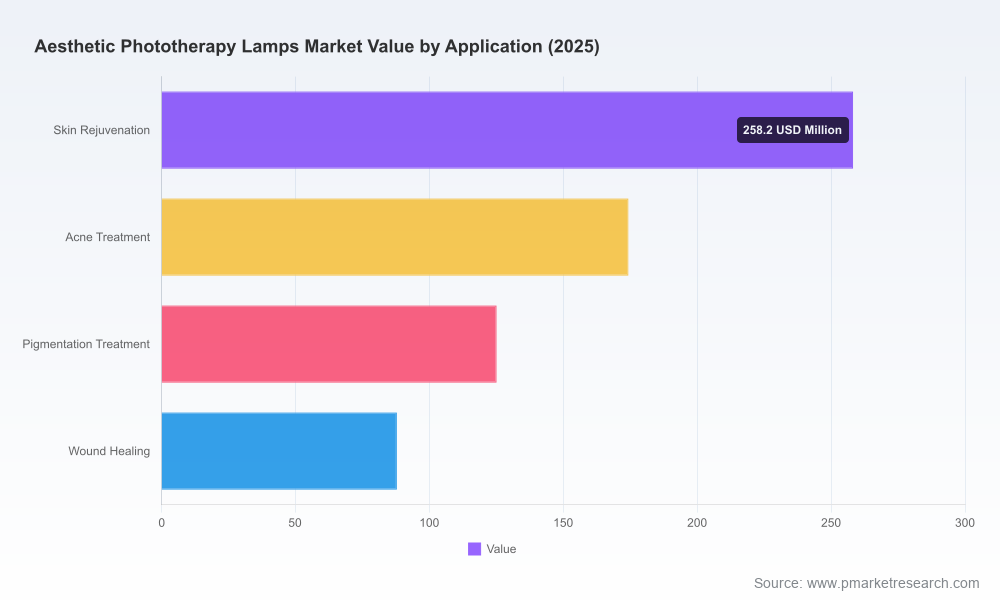

PW Consulting’s latest market study on the Worldwide Aesthetic Phototherapy Lamps market (base year 2025) synthesizes multi-year historical performance, regulatory inflection points and forward-looking scenarios to deliver an actionable intelligence pack for executive decision-making in 2026. The market has grown from a clearly defined five-year historical base into a robust mid‑market sector: total revenues reached USD 645.5 Million in 2025 and are projected to rise to USD 1,161.18 Million by 2032, implying a 2026–2032 compound annual growth rate (CAGR) of 8.75%. Our analysis translates that growth into strategic priorities for manufacturers, investors, and clinical service providers navigating product innovation, compliance and channel transformation.

Worldwide Aesthetic Phototherapy Lamps Market

Why this market matters to C‑suite teams in 2026

- Commercial momentum meets regulatory acceleration: Device-level clearances and new coding initiatives have shifted the commercial calculus for phototherapy solutions from niche adjuncts to mainstream aesthetic and dermatologic tools.

- Dual demand engines: Growth is driven by both professional adoption in clinical and salon channels and accelerating consumer adoption of at‑home therapeutic devices. Strategic plans must bridge these channels without cannibalizing value.

- Margin and scale opportunity: A sustained mid‑teens to single-digit CAGR in the medium term creates a runway for meaningful scale economies, vertical integration, and differentiated service offerings that extend beyond hardware into software, consumables and managed services.

Market trajectory: evidence-based context

Our historical series (2020–2025) documents a steady rebound and acceleration in capital and OTC spending for phototherapy technologies, reflecting both technological maturation (notably LED efficacy and modular excimer platforms) and expanding indications that intersect aesthetic and therapeutic dermatology. From a pragmatic planning standpoint, the USD 645.5 Million base in 2025 and the 8.75% forecast CAGR together signal a market large enough to warrant dedicated product lines, yet dynamic enough that first‑mover differentiation and regulatory timing materially affect ROI horizons.

Worldwide Aesthetic Phototherapy Lamps Market

Regulatory and reimbursement dynamics shaping 2026 decisions

- 510(k) landscape and device class expectations: Aesthetic LED phototherapy devices remain Class II under current US regulation, with 510(k) clearances required for many over‑the‑counter and physician‑directed products. Recent 510(k) approvals for both at‑home and clinical masks in 2024–2025 underline an active pathway for market entry.

- Data capture and coding developments: The activation of a CPT Category III code for photobiomodulation in 2025 and impending revisions to excimer procedure descriptors effective in 2027 create a dual opportunity: (a) to secure early data that supports future reimbursement, and (b) to position excimer-based offerings for broadened reimbursable indications.

- Reimbursement economics matter: Current CPT‑level reimbursements for certain excimer procedures give clinics a tangible per‑treatment revenue opportunity; procurement strategies and clinical trials that align products with billable indications will materially accelerate adoption.

Competitive landscape — what the field looks like in 2026

The market is populated by a blend of specialty lighting manufacturers, legacy medical device makers, consumer wearables players, and boutique European innovators. Key players operate across distinct go‑to‑market archetypes:

Worldwide Aesthetic Phototherapy Lamps Market

- Clinical and OEM lighting specialists: Companies with deep lamp and component expertise supply both finished devices and components to larger system integrators. Their competitive advantage is component quality, regulatory know‑how and B2B relationships with OEMs.

- Device and system integrators: Established aesthetic device manufacturers combine light therapy modules with energy-based systems and leverage existing clinical channels and service networks.

- Consumer brands and DTC innovators: A new cohort of at‑home LED mask and panel sellers competes on brand, convenience and platformized software experiences.

- Regional champions: Several companies focus on localized regulatory and channel depth—clinical sales, hospital procurement and salon networks—rather than global scale.

Notable participants highlighted in our competitive profiles include established component and lamp makers, OEM therapeutic lighting suppliers, medical device and laser manufacturers, and DTC consumer brands. Each profile in the report explores product portfolios, regulatory milestones, recent clearances, manufacturing footprints, and strategic moves—without disclosing proprietary or deal‑sized financials that remain behind our paywall.

Recent tactical milestones that change 2026 playbooks

- Multiple 510(k) clearances for both at‑home masks and clinical excimer devices in 2024–2025 demonstrate the FDA pathway is being actively used to enable wide consumer and clinical access.

- New CPT activity and coding updates create an opportunity to embed phototherapy services into reimbursable clinical workflows — a lever that can shift unit economics for clinics and manufacturers that invest in outcomes studies now.

- Procurement trends show hospitals structuring purchases as bundled CapEx transactions—manufacturers must adapt commercial models to offer integrated install, warranty and managed services options.

What the full report delivers (practical excerpts)

PW Consulting’s complete report contains the following operational assets designed to shorten time‑to‑decision for executives:

- Proprietary market model (2020–2032) with scenario toggles for pricing, reimbursement adoption and regulatory timelines.

- Regulatory and reimbursement matrix mapped by jurisdiction and device class, showing pathways, lead times and evidence requirements.

- Competitive intelligence dossiers: product line maps, recent clearances, go‑to‑market channels and M&A activity tracking for core competitors.

- Commercial playbooks for three archetypal entrants—clinical OEM, DTC consumer brand, and hybrid integrator—with suggested investment roadmaps and break‑even horizons.

- Clinical evidence prioritization guide identifying the smallest feasible RCTs and real‑world evidence programs that unlock coding and payer conversations.

- Procurement and pricing benchmarks, including CapEx tender models and service contract templates tailored to hospital and clinic buyers.

- Deal and partnership opportunity map highlighting targets for bolt‑on acquisitions, supply partnerships and channel alliances.

Strategic recommendations for 2026 — an executive checklist

- Prioritize regulatory sequencing: If your product targets both clinical and consumer segments, sequence submissions to secure clinical credibility first, then scale with OTC clearances where feasible.

- Invest in focused clinical evidence: Small, well‑designed RCTs tied to billable indications can catalyze adoption in clinic networks and support higher ASPs.

- Design channel bifurcation smartly: Maintain clear product and brand differentiation between professional and at‑home offerings to avoid channel conflict and margin erosion.

- Align with reimbursement windows: Use the CPT Category III and the 2027 excimer descriptor changes as trigger points—build registries now to be first to market when coding enables payer conversations.

- Reimagine commercial contracting: Prepare bundled CapEx+service offers for hospital tenders and subscription or consumable models for clinics and salons to enhance recurring revenue.

- Secure supply and component partnerships: Prioritize stable suppliers for LEDs and specialty lamps and explore dual sourcing to limit single‑point failure risks.

- Scan M&A selectively: Target companies that either broaden clinical indication breadth, add consumables recurring revenue, or accelerate geographic access to under‑penetrated distribution channels.

How PW Consulting helps — the decision support edge

Clients use our study as an immediate operating manual: to validate investment cases, size opportunity by channel, model reimbursement impacts, and accelerate regulatory timelines. We combine a robust quantitative model with proprietary primary interviews and a living deal tracker. Importantly, the report is structured to leave no gap between insight and execution—templates, timelines and risk matrices are delivered in editable formats to shorten board approvals and commercial pilots.

Next steps — a strategic call to action

The public summary above outlines the strategic contours a 2026 leadership team must master to capture disproportionate share in a market expanding from a USD 645.5 Million base toward USD 1.16+ Billion by 2032 at an 8.75% CAGR. For full access to the market model, granular segmentation tables, competitive scorecards and executable playbooks, please consult the PW Consulting report landing page or contact our market team. The full dataset and scenario models are required to stress‑test product roadmaps, M&A valuation assumptions and reimbursement‑driven revenue forecasts before capital allocation decisions are finalized.

PW Consulting — where market evidence meets executable strategy.

For detailed analysis of this topic, please visit the official page:Worldwide Aesthetic Phototherapy Lamps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com