Worldwide Pressure‑Resistant Sensor Market — Strategic Insights for 2026 Decision‑Making

Executive summary

As industrial and medical systems push deeper into harsher environments, pressure‑resistant sensors have evolved from component curiosities into strategic enablers. Our latest PW Consulting study sizes the global market at USD 2,439.6 Million in 2025 (base year), and models a trajectory to approximately USD 3,871.5 Million by 2032, reflecting a compound annual growth rate (CAGR) of 6.82% over the 2026–2032 forecast window. Historical performance shows steady acceleration from 2020 through 2025, underscoring both durable end‑market demand and rising complexity in sensing requirements.

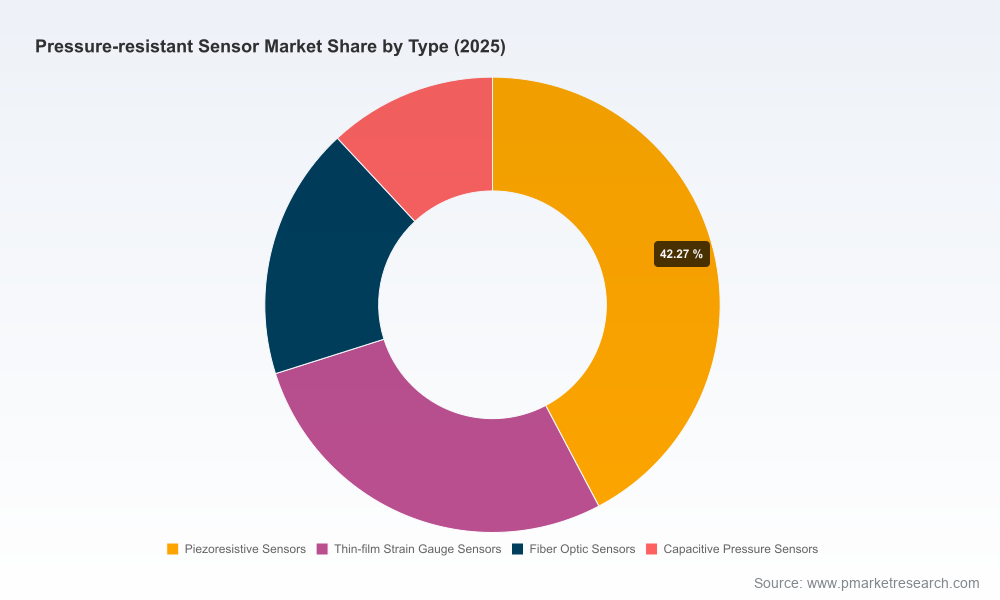

Worldwide Pressure-resistant Sensor Market

This briefing summarizes the report’s decision‑grade value for 2026 planning cycles. It surfaces the industry forces that will drive or derail product roadmaps, manufacturing investments, M&A, and go‑to‑market choices next year, while intentionally withholding the full segmentation tables that appear in the paid report so executives must access the source for transaction‑ready detail.

Worldwide Pressure-resistant Sensor Market

Why 2026 is a pivot year

- Reimbursement and regulatory shifts: A major inflection is already visible in implantable pressure sensing. In early 2025, Centers for Medicare & Medicaid Services (CMS) issued a National Coverage Determination enabling reimbursement pathways for FDA‑approved implantable pulmonary artery pressure sensors — a structural change that reduces commercialization risk for clinical adopters and device OEMs targeting chronic care. At the same time, implantable pressure sensors remain Class III devices in many jurisdictions, making regulatory strategy and quality systems (ISO 13485, ISO 9001) non‑negotiable for market entry.

- Sterilization and materials engineering: Proven housing materials and sterilization compatibility (e.g., polysulfone/polycarbonate housings compatible with Gamma and Ethylene Oxide sterilization, USP Class VI compliance) are differentiators for suppliers targeting both single‑use and implantable markets. These requirements materially influence supplier selection, inventory policies, and shelf‑life economics.

- Manufacturing footprint and capacity: Recent investments — for example, TE Connectivity’s new production facility expansion announced in late 2024 — signal that leaders are scaling for microfluidic and sensor integration demand. For challengers, this raises the bar on time‑to‑market and scale economics.

- Technology convergence: Advances in MEMS, fiber‑optic sensing, and integration libraries showcased at 2025 industry events (e.g., Millar’s TiSense modules at COMPAMED 2025) demonstrate that product differentiation increasingly arises from system integration — not solely from raw sensor accuracy.

What the PW Consulting report delivers (practical toolkit)

- Forward‑looking market model (2026–2032) with scenario sensitivity to price, volume, and adoption curves — ready to plug into corporate financial models.

- Competitive scorecards and supplier capability matrices, including manufacturing capacity, regulatory certifications, and sterile‑processing readiness.

- Technology roadmaps and adoption timelines for MEMS, piezoresistive, fiber‑optic, and capacitive approaches, with guidance on architectural tradeoffs for implantable vs. downhole vs. deep‑sea applications.

- Regulatory playbook covering Class III device pathways, ISO 13485 implementation priorities, and reimbursement engagement strategies following the 2025 CMS determinations.

- Go‑to‑market playbooks: channel strategies for hospital OEMs, energy‑sector integrators, and oceanographic equipment providers; recommended pricing levers and bundling tactics.

- Anonymized M&A target list and diligence checklist designed for buy‑side teams evaluating scale, IP, or vertical integration opportunities.

- Operational readiness checklists for sterilization validation, supply‑chain dual sourcing, and factory automation investments aligned to forecasted demand.

Competitive landscape — who matters and why

The market shows measurable concentration: the top three suppliers account for roughly 38% of industry revenue, and the top five about 52%. That structure creates a two‑tier dynamic — established large suppliers exert price and distribution power, while a mid‑tier of specialists compete on depth of application expertise and vertical integration.

Worldwide Pressure-resistant Sensor Market

- TE Connectivity — With a broad medical‑grade portfolio and recent capacity expansion, TE is positioned to capture growth where sensor integration into microfluidic assemblies matters. Their investments reduce lead times and favor customers seeking turnkey sensor integration.

- Honeywell International Inc. — Honeywell’s emphasis on clinical reliability makes it a preferred partner for hospital OEMs and regulated diagnostic platforms. Their reputation for consistency supports long‑term contracts and clinical validations.

- Edwards Lifesciences (part of BD) — Dominant in disposable hemodynamic monitoring kits, Edwards’ established ecosystems (and parent BD’s distribution reach) make them a strategic acquirer or partner for companies seeking immediate penetration of ICU and procedural markets.

- Merit Sensor Systems — Specialist MEMS piezoresistive offerings and high‑pressure capability make Merit attractive to device OEMs needing high‑pressure and harsh‑media compatibility; their MEMS expertise is central to miniaturization roadmaps.

- Utah Medical Products — As an originator of single‑use transducers with sterilization‑qualified housings, Utah Medical exemplifies how regulatory and sterilization readiness become commercial advantages in supply contracts with hospitals and biopharma customers.

- Amphenol All Sensors, Millar, Sensata, Setra, Metallux, Smiths Medical — These firms collectively span the remaining competitive spectrum: ultra‑low pressure respiratory sensors, catheter‑tip high‑fidelity MEMS, industrial grade robustness, and cost‑efficient high‑range sensors for demanding sectors. Millar’s recent showcase of implantable and chronic monitoring modules highlights the premium on long‑duration biocompatible sensing.

Key dynamics that should shape executive priorities in 2026

- Product portfolio focus: Prioritize development tracks that align with reimbursed clinical use‑cases and with industrial applications where sensor failure carries outsized safety or downtime costs (e.g., downhole oil & gas monitoring, deep‑sea exploration). For medtech firms, allocate R&D to implantable‑grade MEMS and long‑term biocompatibility testing.

- Regulatory and reimbursement readiness: Map product roadmaps against Class III timelines and reimbursement submission windows. Early clinical evidence generation and payer engagement can materially shorten commercialization cycles.

- Supplier and materials strategy: Lock down sterilization‑qualified housing suppliers and validate dual sourcing for high‑risk components. Materials choices that enable multi‑modal sterilization will unlock broader addressable markets.

- Manufacturing scale & vertical integration: Evaluate whether in‑house MEMS fabrication or strategic alliances with vertically integrated suppliers (capable of catheter‑tip assembly or microfluidic integration) are required to meet cost and time‑to‑market targets.

- M&A and partnering playbook: For acquirers, target niche specialists with clinical validation data or unique material/sterilization know‑how. For incumbents, consider bolt‑on acquisitions to fill portfolio gaps in high‑growth subdomains.

- Commercial models: Offer bundled disposable kits and closed‑system sampling integrations where possible — evidence shows strong hospital preference for systems that reduce cross‑contamination risk and simplify workflows.

How to use this report in your 2026 planning cycle

- Board and investor briefings — use the scenario outputs to stress‑test capital allocation for factory expansions and acquisition targets.

- R&D prioritization — align development sprints with the technology roadmaps and the short‑list of high‑value clinical indications profiled in the report.

- Commercial rollout — leverage go‑to‑market playbooks to set channel incentives, reimbursement liaison roles, and hospital field trials.

- Risk mitigation — operational checklists (sterilization validation, dual sourcing, quality certifications) should be converted into 90‑, 180‑, and 360‑day action plans.

Closing — the strategic edge in 2026

For 2026, pressure‑resistant sensors represent both an incremental product decision and a strategic fulcrum: where companies secure sterilization‑qualified materials, validated regulatory pathways, and scalable manufacturing, they secure outsized commercial returns. Our market model and toolset are purpose‑built to convert market intelligence into executable plans — from boardroom capital allocation to shop‑floor process control.

This article presents the high‑level strategic insight from PW Consulting’s Worldwide Pressure‑Resistant Sensor Market report. The full study contains the detailed segmentation matrices, regional and application splits, supplier benchmarking data, and transaction‑ready financial models that corporates, private equity buyers, and product teams require to act in 2026. Access the complete report and datasets through the PW Consulting portal to unlock the granular intelligence that informs closing decisions.

For detailed analysis of this topic, please visit the official page:Worldwide Pressure-resistant Sensor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com