Sugar Free Ice-Cream Market Report: Emerging Technologies and Future Demand

Food |

2026-07-10 09:47:44

PW Consulting’s latest market research brief on the Worldwide Rotating Gamma System (RGS) market distills the commercial, clinical, regulatory and operational intelligence that hospital systems, radiotherapy providers, medical device manufacturers and investors need to prioritize capital and go-to-market decisions in 2026. Anchored on a 2025 base year and a detailed forecast through 2032, the study combines a robust market model with practical deployment playbooks and vendor-level strategic assessments — intentionally presenting depth while preserving proprietary segment-level tables and revenue matrices for subscribers.

Worldwide Rotating Gamma System (RGS) Market

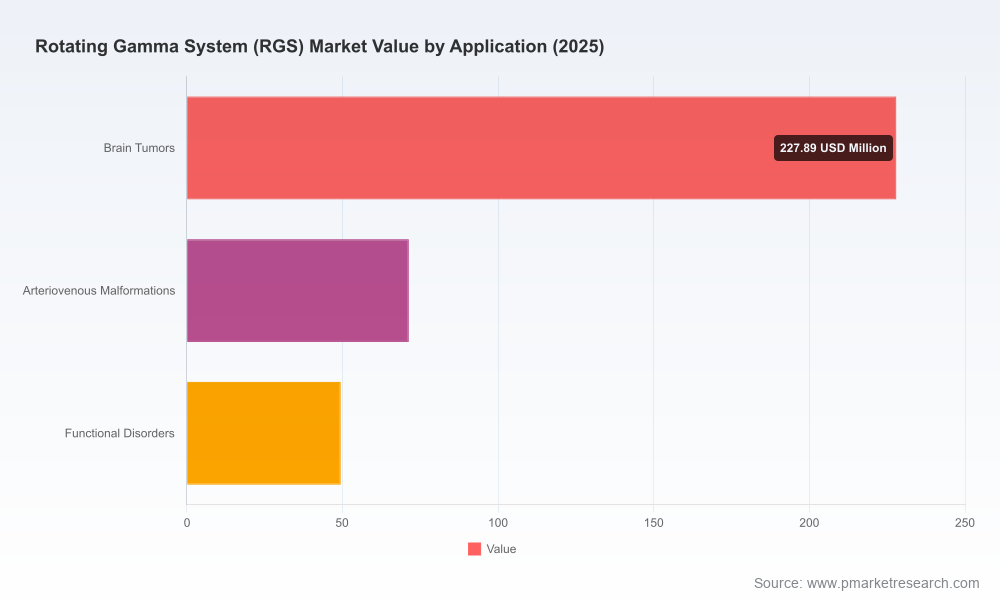

RGS adoption has entered a maturation phase characterized by steady market expansion and growing clinical validation. Our market model places the RGS market at USD 348.66 Million in the base year 2025, having expanded meaningfully from the early-decade baseline through a combination of new product introductions, regulatory clearances, and localized clinical studies. Looking forward, the market is forecast to reach approximately USD 507.19 Million by 2032, tracking at a compound annual growth rate of about 5.5% over the forecast horizon. This trajectory reflects both continued capital purchases of systems and the growing share of recurring maintenance and service revenue as installed bases age and treatment protocols broaden beyond traditional intracranial indications.

Worldwide Rotating Gamma System (RGS) Market

The report is designed as an operational toolkit for decision-makers. Highlights include:

Worldwide Rotating Gamma System (RGS) Market

The RGS competitive set is concentrated among a handful of specialized manufacturers that combine cobalt-60 source architectures with rotating delivery mechanics and varying levels of image guidance. PW Consulting’s assessment focuses on technological differentiation, regulatory positioning, channel strategies and service economics.

Strengths: Established product family (Vertex360, RGS Orbiter) engineered around cobalt-60 based noninvasive radiosurgery for cranial, spinal and select body indications. The company’s long-standing presence and engineering heritage offer buyers a familiar alternative to other rotating-source platforms.

Strategic considerations: American Radiosurgery’s advantage lies in proven delivery mechanics and established clinical workflows. Customers should evaluate service network maturity and spare-source logistics when comparing lifecycle economics.

Strengths: Akesis has rapidly positioned itself with the Galaxy RTi and Gemini360RT systems featuring continuous rotational delivery using thirty cobalt-60 sources and integrated in-plane real-time image guidance. Regulatory milestones have been notable: public notices and clearances have supported entry into the U.S. market.

Recent developments and implications: In 2024–2025 Akesis achieved regulatory milestones and clinical implementations in the United States, including a notable clinical deployment at a major cancer center in 2025. For purchasers, the Akesis offering introduces compelling operational features (real-time image guidance and rotational dosimetry) but also requires careful evaluation of initial service commitments and NRC/NRC-related logistics for source handling.

Strengths: Manufacturer of rotating gamma stereotactic systems (e.g., INFINI) with regulatory clearances in multiple markets. Strong focus on cost-efficient manufacturing and expanding international footprint.

Strategic considerations: MASEP’s product positioning typically appeals to institutions seeking competitive acquisition pricing. Buyers should quantify the trade-offs between lower upfront cost and long-term support, clinical training, and regulatory interoperability in non-domestic markets.

Strengths: Developer of image-guided rotating gamma platforms (TaiChi, Gamma Master) with prior clearances in the U.S. and China. Emphasis on integrated imaging guidance and treatment planning workflow improvements.

Strategic considerations: The TaiChi platform’s clearance history and integrated guidance suite make it attractive for centers prioritizing image-guided extracranial applications. Procurement teams should evaluate installation footprints and integration with existing oncology information systems.

Several industry dynamics materially affect 2026 decision-making:

For leaders setting 2026 capital plans, the RGS landscape offers a compelling mix of clinical potential and procurement complexity. PW Consulting’s Worldwide Rotating Gamma System market report equips stakeholders with the market-sizing, scenario modeling, vendor playbooks and operational templates necessary to convert opportunity into sustainable program performance. To preserve the integrity of our modeling and to support custom procurement guidance, detailed segment-level tables, vendor scorecards and financial models are available exclusively in the full report and subscription datasets. Visit our report page to access the complete intelligence pack and to schedule a strategy briefing with PW Consulting’s radiotherapy practice.

For detailed analysis of this topic, please visit the official page:Worldwide Rotating Gamma System (RGS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com