أحدث تقنيات إبر إذابة الدهون في الرياض

Health |

2026-06-03 05:07:56

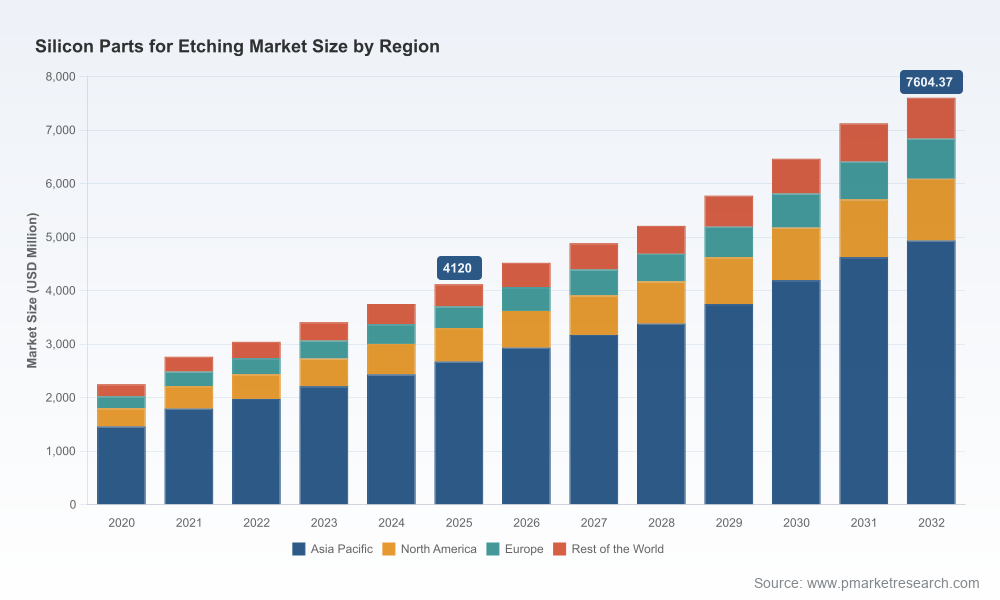

PW Consulting’s latest market study on Worldwide Silicon Parts for Etching provides a focused, decision-grade briefing for executives preparing 2026 strategies. The market has grown rapidly over the past half-decade and, based on our base-year analysis (2025), the industry stands at approximately USD 4.12 billion. With a compound annual growth rate (CAGR) of 9.15% across our 2026–2032 forecast horizon, the market is projected to approach the mid-to-high single-digit billion range by 2032. This preview outlines the strategic implications of that trajectory, highlights practical actions for procurement, manufacturing and corporate development teams, and maps the competitive dynamics you must factor into near-term plans. For full segmented tables, supplier scorecards and proprietary datasets, view the complete report on our website.

Worldwide Silicon Parts for Etching Market

Silicon components—focus rings, electrodes, wafer carriers and other chamber parts—are not exotic one-off items: they are high-frequency consumables in plasma etch processes. Industry data indicates many of these parts require replacement after on the order of a few hundred wafer processes, which creates persistent, repeatable demand streams that amplify the effect of wafer-start cycles. At the same time, the technical bar keeps rising: fabs are demanding near-zero defect monocrystalline silicon produced with advanced growth techniques, and process nodes and materials innovations are forcing tighter impurity, dimensional and thermal stability tolerances.

Worldwide Silicon Parts for Etching Market

What this combination of recurring consumption and rising specification intensity means for 2026 decision-makers is straightforward: supplier selection, qualification timelines and inventory strategies will materially influence both cost of ownership and process uptime. The market-level growth we forecast (CAGR 9.15%) is not evenly distributed by technology or geography, and those asymmetries are precisely what our full report exposes—allowing companies to prioritize investments and partnerships that will deliver outsized returns in the coming 12–36 months.

Worldwide Silicon Parts for Etching Market

Adjusted market sizing and trend analysis: validated historicals (2020–2025) with baseline 2025 market sizing and forward projections to 2032, including scenario runs that stress-test wafer-start volatility, replacement-cycle shifts and material-cost shocks.

Supplier landscape and competitive benchmarking: qualitative profiles and performance attributes of the principal incumbent and emerging players, with a focus on capabilities that matter—material purity, MCZ growth competency, large-diameter capability, vertical integration and OEM alignment.

Operational playbooks: actionable procurement templates, supplier qualification checklists, and a “first 90 days” supplier-onboarding plan tailored to both fab operators and equipment OEMs.

Risk & resilience matrices: scenario planning templates and recommended contract structures (e.g., capacity reservation, hedged pricing tiers, and service-level agreements oriented around contamination events and delivery lead times).

Investment and M&A scoring: a practical framework to prioritize targets (capacity, technology, market access) and a red/amber/green decision grid for near-term transactions.

The supplier ecosystem is heterogeneous: a small number of established vendors serve as structural backbone providers to OEMs and large fabs, while a wider set of regional specialists competes on lead time, customization and price. Our concentration analysis indicates that the top three suppliers control a meaningful share of the market, and the top five approach roughly two-thirds of total market share—an environment that favors both high-quality incumbents and well-capitalized entrants who can match purity and consistency requirements.

Silfex Inc. (Eaton, Ohio, USA): recognized for high-purity custom components and close integration with major equipment OEMs; strength in critical gas-distribution parts and edge rings.

Hana Materials Inc. (Cheonan-si, South Korea): integrated ingot-to-part capability with emphasis on silicon electrodes and rings for dry etch; notable in APAC supply chains and OEM partnerships.

Mitsubishi Materials Corporation (Japan): traditional materials and components supplier with proven quality credentials for etch applications.

Coorstek (USA): positions on high-reliability silicon components engineered to withstand aggressive plasma environments while improving uniformity.

Ningxia Dunyuanjuxin Semiconductor Technology Corporation (DSTC) and other China-based specialists: emphasize scale, a broad portfolio (focus rings, showerheads, shielding rings) and cost-competitive delivery into regional fabs.

Sicreat and other focused monocrystalline suppliers: differentiate on ultra-low impurity content, MCZ growth techniques and the ability to produce large-diameter parts—attributes that map directly to advanced-node and high-volume applications.

Regional and niche players (Semicorex, Worldex, Thinkon/Dynafine, Techno Quartz, RS Technologies, KC Parts Tech.): serve specific OEMs and fabs with tailored geometries, shorter lead-times, or specialist coatings and trays.

Across this competitive set, winning levers are technical certification, OEM approvals, scale for large diameters, and the ability to manage rapid replacement cycles without contamination incidents. The CR3/CR5 concentration metrics in our study underscore an important strategic reality: while market share is concentrated, switching costs and qualification hurdles create durable moats for suppliers that consistently meet purity and defect thresholds.

Consumable cadence: replacement cycles measured in hundreds of wafers imply steady recurring demand; procurement teams must align reorder points with process ramp schedules to avoid unscheduled downtime.

Purity and defect control: advanced fabs increasingly require zero-dislocation or equivalently strict specifications—growth techniques such as Magnetic Czochralski (MCZ) and associated QC protocols are no longer optional for parts used in advanced-node etching.

Geopolitical and regional clustering: Asia Pacific remains a dense cluster for both fabrication capacity and component production; companies should plan for concentrated risk while leveraging regional supplier advantages for speed to market.

Scale and diameter: the ability to produce low-impurity monocrystalline parts at large diameters (up to and beyond 300–400 mm) is becoming a differentiation axis for suppliers serving next-generation etch chambers.

For fabs and OEM procurement leaders:

Implement a two-tier sourcing strategy: secure a primary qualified supplier with capacity reservation and a secondary, regionally diversified partner for surge coverage.

Negotiate quality-driven contracts: include contamination indemnities, rolling qualification timelines, and performance SLAs tied to yield impact, not just part delivery.

Optimize inventory using consumption-based reorder points synced to wafer-start forecasts and scheduled campaign runs to minimize both stockouts and obsolete inventory.

For materials and component suppliers:

Prioritize investments in MCZ growth and advanced QC to meet the zero-dislocation expectations of advanced-node fabs.

Develop modular, value-added services (e.g., pre-conditioning, on-site technical support, rapid requalification kits) that reduce OEM switching costs and enhance stickiness.

Use the 9.15% CAGR baseline to model capacity expansion and project break-even timelines; favor flexible-capacity options over inflexible greenfield builds where possible.

For investors and M&A teams:

Target suppliers that combine proven process credentials (low-impurity monocrystalline output), OEM approvals and untapped regional customer bases—these exhibit the best risk/reward given market concentration dynamics.

Apply our M&A scoring framework to prioritize bolt-on acquisitions that fill capability gaps (large-diameter growth, rapid QC) rather than simple volume plays.

When preparing 2026 budgets and three-year plans, translate the macro CAGR and our scenario outputs into three operational metrics: (1) capacity coverage (months of expected consumable demand secured under contract), (2) inventory days-on-hand measured against replacement cadence, and (3) supplier risk exposure (single-source critical parts). We provide templates that convert the market-level growth trajectory into these practical KPIs so boards can quantify the cost of under-capacity, the value of a second qualified source, and the NPV of supplier investments versus in-house development.

This article is a deliberate strategic preview. The full PW Consulting report contains proprietary regional and application-level splits, detailed supplier scorecards, pricing trend curves, and downloadable forecast datasets that operational and strategy teams will need to execute confidently in 2026. Those proprietary elements are available through our report portal and include: interactive scenario models, supplier due-diligence packs, and RFx-ready procurement templates.

To obtain the complete report and access the supporting datasets and playbooks, please visit the PW Consulting report page or contact our industry practice lead directly. Our team is available to run a tailored briefing workshop for procurement, manufacturing and corporate development teams to translate the findings into 90-, 180- and 365-day action plans.

PW Consulting’s Semiconductor Materials & Components practice combines market modeling, supplier due diligence and operational playbooks to help clients convert market intelligence into measurable business outcomes. Our analyses are grounded in validated field data, supplier interviews and rigorous scenario stress-testing to ensure that 2026 decisions are both defensible and executable.

For detailed analysis of this topic, please visit the official page:Worldwide Silicon Parts for Etching Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com