Wood Vinegar Market to Reach US$ 9.6 Billion by 2031 as Demand for Sustainable Agricultural Solutions Accelerates

Other |

2026-05-19 08:26:31

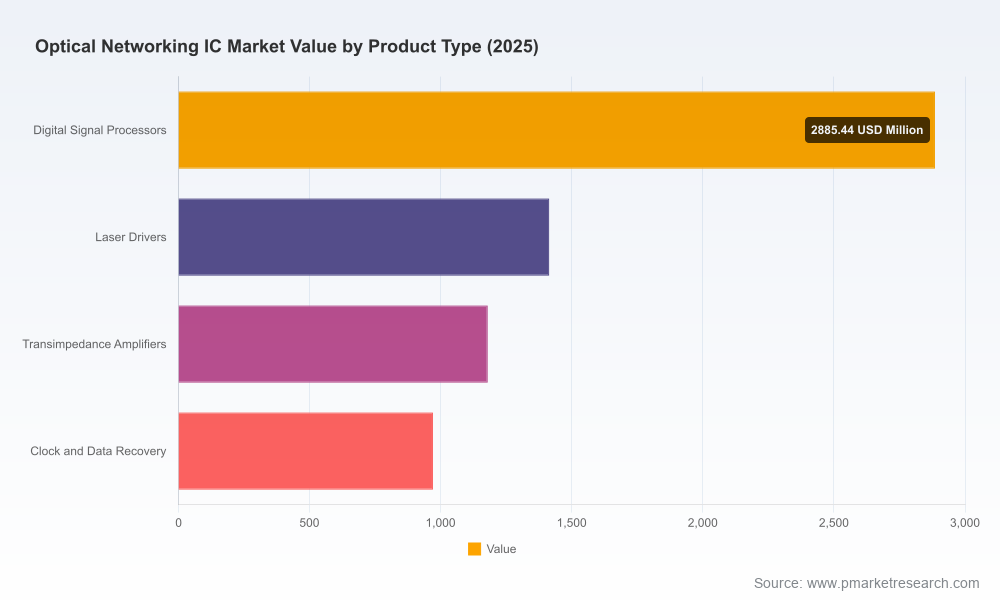

PW Consulting’s latest market study on the Worldwide Optical Networking IC market frames 2026 as an inflection year for technology selection, supply-chain architecture, and capital allocation. Built on a robust historical base (2020–2025) and a detailed forecast through 2032, the study quantifies an industry that reached approximately USD 6.45 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 13.52% across the 2026–2032 forecast window, reaching roughly USD 15.67 billion by 2032. This release is designed for executives who must convert technology signals into commercial advantage — we reveal the directional market dynamics and structural risks that should drive boardroom decisions in 2026, while preserving the granular segment maps and supplier scorecards available in the full report.

Worldwide Optical Networking IC Market

AI-driven demand patterns: The rapid scaling of generative AI and large-scale model training continues to re-shape optical-interconnect requirements. Network architects are prioritizing density, low-latency connectivity, and energy efficiency — attributes that directly influence optical IC selection and module architecture strategies.

Worldwide Optical Networking IC Market

Energy and cost pressure: U.S. data centers consumed roughly 176 TWh in 2023, a meaningful baseline for energy-sensitive procurement and design choices. Combined with the high and variable civil costs of fiber deployment (ranging significantly by terrain and urban complexity), these pressures force buyers to evaluate total cost of ownership (TCO) and lifecycle energy performance, not only raw cost-per-bit.

Worldwide Optical Networking IC Market

Architecture transition: The industry is actively validating co-packaged optics (CPO) and linear pluggable optics (LPO) approaches. Independent demonstrations and vendor roadmaps indicate potential power savings of up to 65% for CPO/LPO architectures versus traditional pluggable DSP-based modules in tightly coupled AI clusters — a material input to long-term operating expense forecasts.

Standards and interoperability momentum: Multi-vendor interoperability events in early 2026 showcased the practical path to deployable ecosystems. These efforts reduce integration risk for buyers but also accelerate commoditization pressure on lower-differentiated IC functions.

Our study is intentionally practice-oriented. Beyond market sizing and growth trajectories, the report delivers repeatable decision frameworks tailored for procurement, product, and strategy teams:

Market-sizing methodology and transparent assumptions — enabling clients to stress-test outcomes under alternative AI adoption and deployment scenarios.

Scenario-based financial models for TCO and energy-cost sensitivity across pluggable, co-packaged, and hybrid optical architectures.

Technology roadmaps for optical IC classes (signal processors, driver/TIA families, clock/data recovery and more) aligned with packaging trends and node transitions.

A vendor strategic matrix and risk heatmap (technology depth, supply resilience, roadmap clarity, IP posture) to support sourcing and partnership decisions.

Supply-chain playbooks — including contract templates, dual-sourcing strategies, and logistics stress tests for high-volume module ramp scenarios.

Regulatory and funding alignment guidance — practical checklists for leveraging public broadband and backbone programs to accelerate fiber and interconnect investments.

Interoperability and standards readiness checklists to shorten time-to-deployment and reduce integration cost overruns.

The market exhibits meaningful concentration, with the top-three suppliers controlling north of sixty percent of the market by revenue and the top-five approaching eighty percent. That structure creates a dual dynamic: consolidation-driven scale benefits for incumbents and persistent opportunities for focused challengers that can de-risk specific performance vectors (power, cost-per-bit, or integrated photonics).

Broadcom Inc. — With the recent introduction of a 3nm, 400G/lane PAM4 DSP family positioned for 1.6T pluggables, Broadcom is doubling down on high-performance, low-power DSPs aimed at AI data center interconnects. This move tightens its position in high-end pluggable markets and raises the technology bar on power-per-bit metrics.

Marvell Technology — The acquisition of a plasmonics-focused player signals a strategic bet on alternative modulation approaches and silicon photonics scaling beyond current coherent limits. Marvell’s playbook appears designed to combine DSP/IP stacks with modulation primitives that enable multi-terabit coherent links.

Intel — Intel’s silicon photonics and CPO initiatives remain central to its strategy to verticalize optical interconnects for hyperscale and HPC customers. Expect continued emphasis on platform integration and co-development deals with switch and switch-ASIC vendors.

Cisco / Acacia — Cisco’s coherent optics competency (bolstered by prior acquisitions) targets operators and data-center fabrics that require turnkey optical systems. Cisco’s scale and systems integration capability remain a competitive moat for customers seeking single-vendor delivery.

Semtech — Recent live demonstrations of high-rate TIAs and driver families for 1.6T interconnects demonstrate Semtech’s role in enabling next-step multi-lane optics for AI clusters, particularly in architectures favoring linear pluggable approaches.

Specialists and OEMs (Coherent, Lumentum, Infinera, Ciena, Lumentum) — These players are differentiating through optoelectronic components, PICs, and coherent engines; their relevance varies by deployment class (long-haul vs. metro vs. hyperscale interconnects) and by the degree of system-level integration customers demand.

NVIDIA — As a hyperscaler-facing platform vendor, NVIDIA’s investments in silicon photonics and co-packaged optics, especially when integrated with its switching fabrics, create forward pressure on system architectures and offer a potential pull-through for partner optical IC suppliers.

Early 2026 activity crystallizes the pace of technology migration: high-performance DSP launches, strategic M&A in photonics and plasmonics, and multi-vendor interoperability demos at major optical conferences. Collectively, these events point to an accelerating modularization of optical systems — more capable ICs, denser photonics, and a bifurcation in architectures between highly integrated CPO deployments and more conservative pluggable-module upgrades.

Adopt a phased CPO/LPO evaluation: Prioritize pilot programs aligned with the highest-cost-per-watt workloads in 2026, and preserve pluggable options where operational simplicity and vendor diversity are paramount.

Integrate energy-cost metrics into procurement rules: Require vendors to disclose energy-per-bit under defined load profiles and include this metric in TCO comparisons over realistic lifecycle horizons.

Stress-test supply chains and plan for dual-sourcing of critical IC classes: Given the market concentration and recent supplier consolidation, buyers should negotiate flexible supply terms and qualify secondary sources for critical components.

Leverage interoperability events and open testbeds: Participation in multi-vendor demonstrations reduces integration risk and can accelerate time-to-revenue for new module form factors.

Align capital plans with public funding windows: National broadband and backbone programs create opportunities to co-fund fiber buildouts that materially change deployment economics; coordinate procurement timelines to capture these funding levers.

Prepare for architectural heterogeneity: Design network roadmaps that accommodate a mixed estate (pluggable, co-packaged, hybrid) and use scenario analysis to budget for migration paths and stranded-asset risk.

Monitor standards and protocol workstreams closely: Emerging electrical and photonic interfaces will determine interoperability and port economics; investors and architects should follow key interoperability forums and incorporate conformance testing into procurement.

For executives who must move from technical debate to board-level commitment, PW Consulting’s report delivers the calibrated market sizing, scenario models, and vendor intelligence to prioritize near-term investments and de-risk multi-year deployments. Our analysis clarifies where to invest (and where to wait), how to structure vendor relationships, and which architectural choices yield the most defensible TCO outcomes under multiple AI and cloud-growth scenarios.

To access the complete segmentation, vendor scorecards, and downloadable TCO models that underpin these conclusions, please visit the report page on PW Consulting — the full dataset and actionable appendices remain available to subscribers and licensed purchasers.

For detailed analysis of this topic, please visit the official page:Worldwide Optical Networking IC Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com