How Often Can You Get Yellow Peel in Dubai for Maintenance?

Health |

2026-04-25 07:13:09

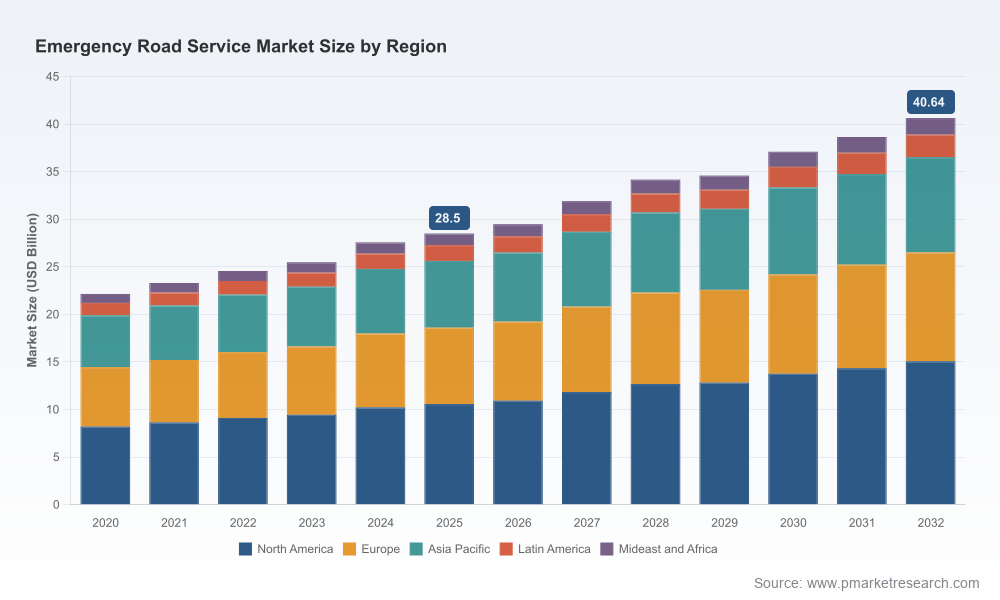

As organizations plan budgets and strategic initiatives for 2026, the emergency roadside services (ERS) sector is at an inflection point. PW Consulting’s latest market study — covering 2020–2025 as the historical baseline and projecting through 2026–2032 — shows the global market expanding from roughly USD 22 billion in 2020 to about USD 28.5 billion in 2025, and forecasted to approach USD 40.6 billion by 2032 at a compound annual growth rate (CAGR) of 5.2%. These headline metrics mask rapid structural change beneath the surface. This briefing highlights the strategic value of the full report for executive decision-making in 2026 while deliberately reserving detailed segmentation outputs to the primary publication.

Worldwide Emergency Road Service Market

Resilient growth with operational unpredictability: A stable mid-single-digit CAGR coupled with episodic cost pressure (notably rising labor costs and evolving regulatory requirements) means leaders must balance scale investments with nimble operational playbooks.

Worldwide Emergency Road Service Market

Consolidation opportunity set: Market concentration metrics indicate a market where several large incumbents coexist with an extensive independent provider base — a structure that rewards focused M&A and platform plays that can stitch networks and technology together.

Worldwide Emergency Road Service Market

Technology as a differentiator: Providers that couple physical fleet capacity with superior digital routing, telematics integration, and customer-facing apps are improving response times and unit economics at scale.

Regulatory and data risks: New compliance vectors (e.g., mandatory telematics/GPS tracing requirements and tightened data privacy rules) will materially affect operational design and vendor selection for global players.

Our study has been engineered as an operational toolkit for decision-makers. Components include:

Executive dashboards that translate market growth, cost inflation, and concentration dynamics into actionable KPIs for corporate planning.

Scenario financial models (base, accelerated digital adoption, and high-consolidation) that stress-test capital expenditure, driver labor cost inflation, and service reimbursement assumptions over 2026–2032.

Provider network optimization templates, including provider-tiering logic, dynamic dispatch rules, and SLA indexing to link reimbursement to performance.

Go-to-market playbooks for insurers, automakers, and independent providers — covering pricing, bundling, and partnership archetypes tailored to distinct strategic goals (retention, revenue diversification, or platform monetization).

M&A screening criteria and valuation yardsticks tuned to ERS market dynamics: synergies from network densification, technology integration uplift, and claims-cost arbitrage.

Compliance and implementation checklists for GPS/telematics mandates and data-privacy requirements, including operational controls and anonymization workflows aligned to recent regulatory guidance.

The ERS ecosystem is anchored by a mix of legacy auto clubs, insurer-affiliated programs, and high-scale B2B platforms that dispatch a broad network of independent providers. Key players we profile in depth include global auto clubs and insurer-integrated programs that retain high-touch member relationships, and technology-led dispatch platforms that optimize network efficiency.

Large auto-club incumbents maintain strong customer loyalty through membership models and integrated services. Their investments in consumer apps and ancillary services are central to member retention strategies.

Insurer-aligned motor clubs and motorist assistance products are increasingly leveraged not only for claims mitigation but also as a customer acquisition and retention channel; these relationships create upside for providers who can guarantee response performance and cost predictability.

Technology-first B2B platforms act as orchestration layers between insurers, OEMs, and local service providers. Their ability to deliver predictive routing, telematics integration, and real-time dispatching is a primary differentiator.

Recent strategic moves validate these dynamics. Notably, a leading B2B dispatch platform announced an AI-driven partnership with a major insurer to accelerate predictive routing and dispatch efficiency. One of the long-standing auto clubs upgraded its consumer app to include EV charging locators and battery diagnostics — an explicit signal that incumbent players are evolving to capture EV-related roadside revenue. A major European club piloted drone-assisted breakdown scouting to accelerate response in rural zones, demonstrating innovation at the intersection of hardware and operations.

The market displays moderate concentration at the top while remaining materially fragmented overall — a profile that creates multiple strategic pathways. Players with strong balance sheets can pursue network aggregation, technology consolidation, and exclusive insurer/OEM partnerships. Smaller providers can compete by specializing (e.g., EV-first mobile charging, heavy-tow logistics, or regional rapid-repair capabilities) and by partnering with orchestration platforms.

For corporates contemplating M&A or alliance strategies, the decision framework we provide links measurable operational outcomes (response time, first-time fix, and per-incident cost) to valuation multiples and integration roadmaps. The key is proving service-level improvements and cost takeout from day one.

Labor market pressures: Tow-operator wages rose materially in recent years due to driver shortages, increasing the unit labor cost baseline. This trend necessitates higher productivity per technician and better route optimization to preserve margins.

Reimbursement realities: Insurer reimbursement patterns have shifted upward in recent years, putting near-term pressure on payers while creating revenue upside for providers able to demonstrate cost-of-service governance and fraud controls.

Regulation and compliance: New EU mandates for real-time GPS tracking of roadside vehicles and updated data-protection guidelines requiring anonymization within tight windows are reshaping telematics architectures and data-retention policies.

EV and new-technology service demand: Electrification increases demand for mobile battery services and on-site charging solutions while introducing new safety protocols and equipment needs for technicians.

Investments that consistently show positive ROI in our models include:

Predictive dispatch and routing using telematics and AI to reduce drive-time and enable higher job density per shift.

Customer-facing mobile experiences that integrate diagnostics, live ETAs, and frictionless claims submission — reducing call-center volume and improving NPS.

Specialized EV service capabilities (mobile chargers, battery health tooling, technician certification programs) to capture a growing share of emergent service demand.

Data governance platforms that automate anonymization and retention policies to meet regional privacy rules — a practical necessity in cross-border operations.

Prioritize platform partnerships: If you are an insurer or OEM, partner with a dispatch platform that demonstrates measurable ETA reduction and transparent SLA reporting rather than trying to build a national network from scratch.

Execute a capability-led M&A roadmap: Target acquisitions that fill capability gaps (e.g., EV mobile charging, heavy-tow capacity, or regional rapid-repair hubs) and model integration synergies conservatively.

Deploy targeted digital pilots at scale: Run regionally concentrated pilots for AI routing, app-based claims flow, and telematics-driven dynamic pricing to generate live evidence for full roll-out decisions.

Invest in workforce productivity: Use routing, scheduling, and multi-job bundling to offset wage inflation and raise per-shift revenue; pair this with certification programs for EV and high-voltage safety.

Harden data and compliance posture: Build anonymization pipelines and auditable retention policies now to avoid costly retrofits as privacy and telematics mandates proliferate.

The full study supplies the granular tools and data investors and operators need to operationalize these strategic moves: downloadable models calibrated to alternative cost and reimbursement scenarios, a vendor due-diligence checklist, a regional implementation playbook, and a prioritized technology investment roadmap. For leaders who want to translate the 5.2% CAGR and market expansion into defensible 2026 budgets and 3–5 year strategies, the report provides both the evidence base and the playbook templates.

The Worldwide Emergency Road Service market is growing steadily, yet its near-term economics and competitive balance are being rewritten by labor market dynamics, regulatory change, and rapid technology adoption. Organizations that combine select investments in dispatch technology, EV service capability, and workforce productivity — underpinned by a disciplined M&A and partnership strategy — will disproportionately capture value as the market scales toward 2032. PW Consulting’s full report is designed to bridge the gap between headline market forecasts and executable 2026 playbooks: it delivers the diagnostic evidence and the operational templates needed to move from strategy to execution. For access to detailed segmentation, granular financial models, and our customized implementation guides, consult the full report.

For detailed analysis of this topic, please visit the official page:Worldwide Emergency Road Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com