Silver Bracelets: The Ultimate Guide to Timeless Elegance and Everyday Style

Shopping |

2026-04-12 10:02:47

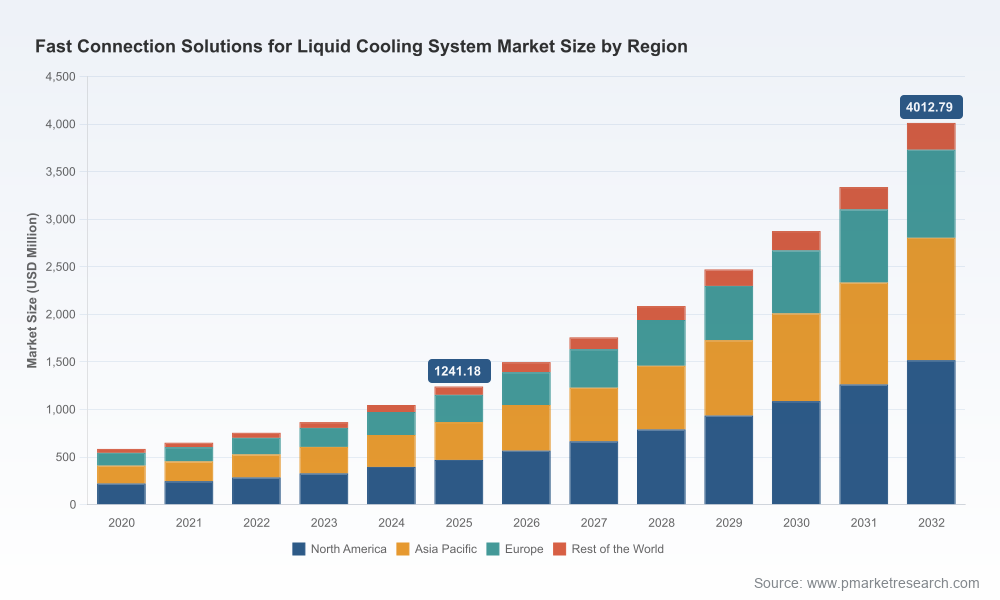

PW Consulting today publishes a strategic preview of its forthcoming market research report, “Worldwide Fast Connection Solutions for Liquid Cooling System Market.” Anchored on a 2025 base year and offering a forward-looking forecast for 2026–2032, the analysis quantifies a robust industry expansion with a compound annual growth rate (CAGR) of 18.25% across the forecast window. In currency terms (USD, revenue unit: Million), the market is already transitioning from a phase of steady recovery to one of accelerated commercialization driven by direct liquid cooling (DLC), blind‑mate architectures, and cross‑industry electrification initiatives.

Worldwide Fast Connection Solutions for Liquid Cooling System Market

Portfolio prioritization: With industry growth accelerating at an 18.25% CAGR, companies must reassess R&D and product investment timelines. Early mover investments in blind‑mate and non‑spill quick disconnect solutions will disproportionately influence market share as systems scale from prototype to rack‑level and campus deployments.

Worldwide Fast Connection Solutions for Liquid Cooling System Market

Supply‑chain resilience: The market’s ongoing maturation increases procurement complexity—materials selection (metal versus polymer), supplier qualification cycles, and manufacturing capacity constraints all become strategic levers. The report identifies decision points to balance cost, purity, and leak‑tight performance for high‑value applications.

Worldwide Fast Connection Solutions for Liquid Cooling System Market

Regulatory and compliance alignment: Evolving standards (ASHRAE updates and ISO/IEC data‑center efficiency measures) are rapidly shifting the compliance baseline. Firms that embed regulatory trajectories into product roadmaps and go‑to‑market plans will minimize retrofit risk and accelerate procurement approvals in regulated regions.

Customer segmentation & channel strategy: As liquid cooling migrates from specialized HPC facilities to broader data center, EV infrastructure, and industrial deployments, channel models and partner ecosystems must be redesigned to support blind‑mate serviceability, field maintenance, and rapid swap‑out procedures.

PW Consulting’s full deliverable is designed as a playbook for corporate strategy teams, product leaders, and M&A professionals. Key operational modules include:

Top‑down market sizing and scenario modelling: deterministic and probabilistic projections across 2026–2032 with sensitivity to adoption curves, thermal load distributions, and technology substitution rates.

Go‑to‑market playbooks for device OEMs, CDUs, and hyperscalers that translate cooling architecture choices into sales motion, pricing, and installation support requirements.

Supply‑chain and materials intelligence: an actionable assessment of metal and polymer sourcing, yield and corrosion risk, and supplier concentration with mitigation strategies for near‑term disruption.

Regulatory impact analysis: granular implications of ASHRAE updates, ISO/IEC metrics, and regional energy efficiency mandates on product specs and procurement cycles.

Competitive landscaping and partner matchmaking: capability maps, white‑space identification, and a validated shortlist of potential manufacturing and distribution partners tailored to specific application segments.

Commercial due diligence tools: margin and pricing benchmarks, CR thresholds for M&A, and a transaction playbook to accelerate integration in an increasingly concentrated market.

The shift to liquid cooling is not academic—it is being catalyzed by insatiable compute density in AI/HPC, increased adoption of direct‑to‑chip cooling architectures, and electrification trends in vehicles and energy storage. Governmental and standards bodies are tightening efficiency expectations; liquid cooling is proving an effective path to lower PUEs and to meet evolving energy intensity mandates.

From a materials perspective, traditional metals continue to dominate high‑pressure quick disconnect solutions due to strength and thermal durability, while polymer innovations (PVDF and engineered polyolefins) are gaining traction for polymer‑based valve assemblies and distribution plumbing where purity, weight, and flow optimization matter. These material tradeoffs increasingly define supplier selection and lifecycle cost models.

The market is unevenly concentrated: a handful of firms command meaningful scale, with the top three and top five suppliers exerting disproportionate commercial influence. This concentration has practical consequences for OEM sourcing, qualification time, and the competitive dynamics of new architecture rollouts.

Profiles and strategic implications of leading players:

CPC (Colder Products Company) — Strengths: purpose‑built Everis® series (including blind‑mate and non‑spill platforms) tailored for electronics and data center cooling. Strategic move: product families optimized for field serviceability and high‑flow, making CPC a preferred partner for retrofit and modular rack solutions.

Parker Hannifin Quick Coupling Division — Strengths: industrial pedigree in dripless, high‑pressure quick disconnects. Strategic move: thought leadership on pressure‑drop minimization and energy efficiency, positioning Parker to influence system‑level thermal design conversations.

CEJN — Strengths: OCP‑aligned high‑flow, low‑pressure‑drop couplings and blind‑mate interoperability. Strategic move: close engagement with hyperscalers gives CEJN early insight into rack‑level connector standards and mass‑deployed architectures.

Danfoss (Hansen®) — Strengths: flow‑path engineering to reduce pressure loss. Strategic move: targeting data center and edge thermal control with components that integrate directly into cooling distribution units (CDUs).

Stäubli — Strengths: clean‑break, quick‑disconnect solutions that perform at elevated temperatures. Strategic move: recent product miniaturization efforts expose new applications in optics and high‑density module cooling.

Amphenol Industrial Operations — Strengths: broad connector portfolio that spans blind‑mate and high‑flow needs across data center, EV, and ESS use cases. Strategic move: system integration capability positions Amphenol as a cross‑segment enabler.

Gates, Specialty Manufacturing, TITAN Fluid, Motivair — Each brings differentiated value: from full‑flow, direct‑to‑chip couplings to specialized stainless‑steel universal quick disconnects and OEM‑aligned Everis™ derivatives. Collectively, these suppliers supply the innovation and customization layer for high‑performance bespoke systems.

Polymer adoption and system‑level polymer CDUs have gained momentum with new product releases that demonstrate valve integrity and flow optimization—underscoring an industry willingness to substitute metal where purity and weight advantages prevail.

Major component launches and exhibitions in 2025–2026 have spotlighted miniaturized quick disconnects for optical modules, full‑scope polymer cooling infrastructures for direct‑to‑chip deployments, and refined guidance on pressure‑drop management—clear indicators that suppliers are racing on both miniaturization and flow efficiency fronts.

Thought leadership from legacy hydraulic and coupling companies continues to shift discourse from component specs to system‑level energy performance, reinforcing the linkage between connector choice and operational TCO.

Prioritize modularity in product roadmaps: design connectors and CDUs for blind‑mate interoperability and serviceability to reduce field downtime and enable rapid scaling across racks and sites.

Lock in dual‑sourced material pathways: metals will remain critical for high‑pressure segments, while validated polymer alternatives can offer competitive cost and installation benefits. Early supplier qualification eases time‑to‑market pressure.

Embed regulation into procurement criteria: incorporate ASHRAE and ISO/IEC metrics into RFPs to avoid costly retrofits and to accelerate approvals for large-scale deployments.

Use competitive concentration as a merger and partnership lever: consider targeted acquisitions or strategic alliances with established coupling specialists to accelerate access to qualified product families and certification track records.

Beyond forecasting, the report is engineered as an executable intelligence package: modelling outputs are delivered alongside commercial playbooks, supplier readiness checklists, and a validated partner matrix. Crucially, the study preserves commercial confidentiality where it matters—detailed subsegment splits and proprietary client benchmarks are intentionally summarized in this preview to encourage direct access to the full report for transactional decisions.

For companies evaluating entry, expansion, or M&A in the fast connections market for liquid cooling, 2026 represents a pivotal inflection point. PW Consulting’s complete report supplies the granular regional, application, and product‑level intelligence required to build defensible strategies and execute with confidence. Access to the full dataset, scenario models, and supplier scorecards is available through PW Consulting’s market research portal.

For detailed analysis of this topic, please visit the official page:Worldwide Fast Connection Solutions for Liquid Cooling System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com