Surface Mount LED Market 2026 to Reach New Growth Milestone Through 2034 with Rising Demand

Dance |

2026-07-06 11:43:37

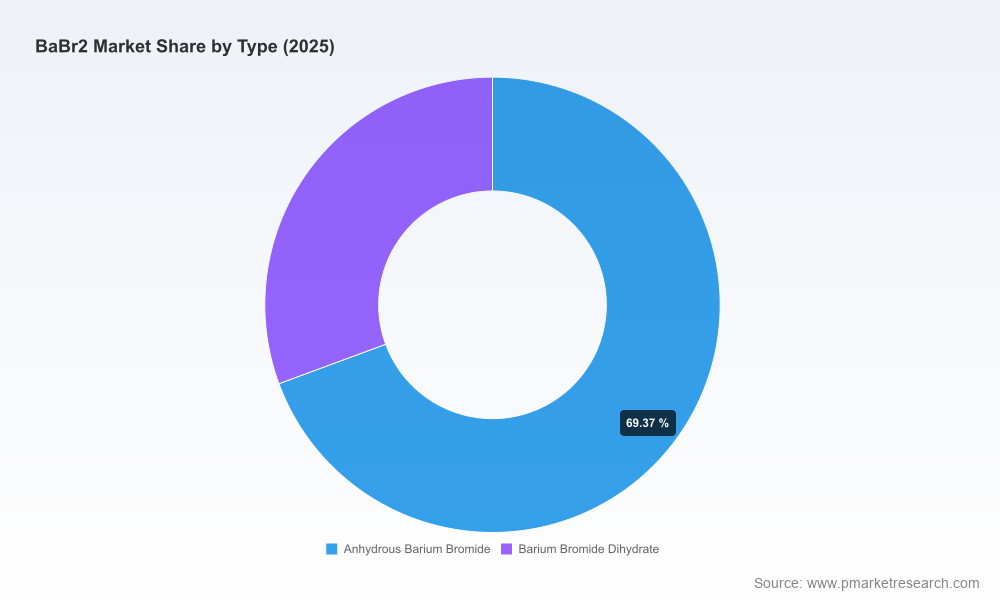

PW Consulting’s latest BaBr2 Market report (base year 2025; historical window 2020–2025; forecast 2026–2032) distills the signals that will matter for companies making strategic choices in 2026. The global BaBr2 market has demonstrated steady expansion from the start of the decade, rising from the low‑forties in USD million terms in 2020 to approximately USD 47.6 Million in 2025. Our baseline outlook sees continued, mid‑single‑digit compound annual growth through 2032 (CAGR ~4.3%), reaching an upper‑sixties million USD scale by the terminal year under a central scenario.

BaBr2 Market

This briefing follows our “preview, not reveal” principle: it surfaces the high‑value implications, frameworks, and recommended actions derived from our deep analysis while preserving segmented detail within the full report to encourage direct engagement for procurement, product, and M&A teams. Below we outline the dynamics that will shape supplier advantage, buyer risk, and value creation opportunities in 2026.

BaBr2 Market

Demand resilience across specialty end‑markets. The market’s steady expansion through 2025 has been driven by persistent demand in advanced materials, specialty imaging, and select chemical processing applications. While not a high‑volume commodity, BaBr2 benefits from pockets of technical use where purity and reliability command premium pricing.

BaBr2 Market

Feedstock and energy cost pressures. Production of BaBr2 remains tied to conventional synthesis routes (e.g., reacting barium carbonate or barium sulfide with hydrobromic acid). In 2025, producers in Europe reported meaningful upward pressure on feedstock and logistics costs—an input story that is expected to continue influencing supplier margins and contract pricing through 2026.

Regulatory and transport constraints increasing complexity. Barium bromide is subject to hazardous‑substance regulatory frameworks and is classified under transport rules that impose specific packing and handling requirements. In particular, European chemical regulation frameworks and marine environmental policies include BaBr2 among monitored substances, raising compliance and documentation burdens for exporters and importers.

Supply structure: quality segmentation over capacity. The market is characterized by a spectrum of producers—from commodity powder manufacturers to specialists supplying ultra‑high‑purity beads for research and scintillation applications. This segmentation creates room for differentiated commercial strategies (premium positioning for high‑purity, cost discipline for bulk industrial supply).

Procurement: move from spot dependence to tiered contracts. Buyers should adopt a two‑track sourcing model combining longer‑dated, volume‑protected contracts with select high‑purity suppliers and tactical spot buying for lower‑spec material. Contract terms must explicitly address feedstock inflation pass‑through and freight volatility clauses.

Risk mitigation: prioritize logistical and regulatory resilience. Given UN and regional regulatory obligations, manufacturers and distributors should audit transport compliance, invest in robust documentation systems, and qualify alternate packaging and consolidators to avoid shipment delays and fines.

Product strategy: focus R&D and commercialization on application‑specific differentiation. Opportunities for margin expansion are concentrated in high‑purity formulations, bead forms optimized for optical and scintillation applications, and custom reagent grades for life sciences. Firms that can authenticate trace‑level purity and supply small‑batch, high‑value lots will outcompete commodity suppliers.

Supply‑chain playbook: consider selective vertical integration or strategic alliances. For mid‑size chemical firms, investing selectively in purification or finishing capacity can secure supply and capture downstream margin. Larger players and specialized suppliers may seek offtake partnerships with material users in optics and imaging to lock multi‑year demand.

M&A and partnerships: seek bolt‑on technology and distribution assets. Consolidation is probable among regional producers and distributors that lack scale in regulatory compliance and international logistics. Strategic buyers should target assets that enhance high‑purity processing, certifications (e.g., ISO), or access to tier‑one customers in advanced materials.

Our analysis of active market players reveals a clear pattern: differentiation is achieved through combinations of product purity, regulatory certifications, integrated production footprint, and distribution reach.

Regional specialty exporters: Companies headquartered in major chemical hubs have leveraged export networks and adherence to international quality standards to serve pharmaceutical, dyes, and chemical intermediates markets. Their value proposition is reliability and regulatory alignment for cross‑border customers.

Industrial‑grade domestic suppliers: Several India‑ and China‑based producers focus on industrial and laboratory grade material with certifications such as ISO 9001. Their competitive edge lies in cost‑to‑serve, local distribution, and ability to meet high‑volume industrial specifications.

High‑purity and research‑oriented suppliers: US‑based and global laboratory brands supply ultra‑high‑purity BaBr2 in bead and reagent forms, servicing research, advanced materials, and niche optical applications. These suppliers justify premium pricing through rigorous trace‑metal specifications, small‑lot availability, and strong product data packages.

Examples of profiles informing these archetypes include established exporters with broad end‑market coverage, ISO‑certified industrial manufacturers, integrated Chinese producers blending R&D and factory pricing, and laboratory brands that dominate the highest‑spec segments. For buyers and investors, the competitive playbook is straightforward: map supplier archetypes to your quality, lead time, and cost tolerance; then align contracting and inventory policies accordingly.

PW Consulting’s full BaBr2 Market report equips decision‑makers with operational tools and analyses designed for immediate use:

Validated market sizing and scenario models (base year 2025; forecast 2026–2032; central CAGR ~4.3%) with upside and downside demand scenarios tied to end‑market adoption.

Supplier scorecards and risk maps that assess quality certifications, capacity, compliance posture, logistics constraints, and commercialization capability—enabling rapid shortlisting of contractual partners.

Procurement playbooks, including sample contract clauses for pass‑through adjustments, penalty frameworks for non‑compliance, and standard testing protocols for incoming materials.

Regulatory checklist and incident playbook covering transport classification, packaging recommendations, and steps to secure cross‑border movement under regional chemical safety regimes.

Commercial assessment templates and valuation heuristics for M&A and JV evaluation, focused on capture of high‑purity segments and integration of purification capabilities.

Collectively, these deliverables enable procurement, supply‑chain, and corporate development teams to translate market signals into quantifiable initiatives with defined KPIs for 2026.

Complete a supplier compliance and certification audit for all BaBr2 vendors; prioritize remediation plans for any gaps tied to transport and REACH‑style obligations.

Negotiate at least one anchor offtake agreement with a high‑purity supplier to secure access for critical product lines; include clauses to mitigate feedstock cost escalation.

Run a quick P&L sensitivity for 2026 that tests margin impact under alternative feedstock and freight scenarios; use this to calibrate pricing and inventory buffers.

Identify bolt‑on acquisition targets or technology partners that add purification or finishing capabilities within your geography of interest.

Stand up a cross‑functional compliance taskforce (procurement, legal, quality, logistics) to streamline shipments and preempt regulatory delays.

As 2026 begins, market participants will be judged less on broad forecasts and more on execution: the ability to secure compliant supply, to selectively invest in higher‑value product capability, and to design contracting that protects margins from input volatility. The BaBr2 market’s moderate, steady growth provides a predictable envelope, but within that envelope winners will be those who combine technical product differentiation with robust regulatory and logistics execution.

This release highlights the strategic framing and practical tools available in PW Consulting’s full BaBr2 Market report. The comprehensive dataset, segmented demand analysis, supplier‑level benchmarking, and downloadable contract and compliance templates are intentionally reserved for the report to preserve competitive advantage and ensure clients can act decisively. To access the full report, supplier scorecards, and scenario models that underpin the recommendations above, please visit our report page or contact your PW Consulting account lead.

PW Consulting — translating chemical market complexity into operational clarity for 2026 decision-makers.

For detailed analysis of this topic, please visit the official page:BaBr2 Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com