Worldwide Industrial High-Resolution Camera Market: Strategic Outlook and Decision Playbook for 2026

Executive summary

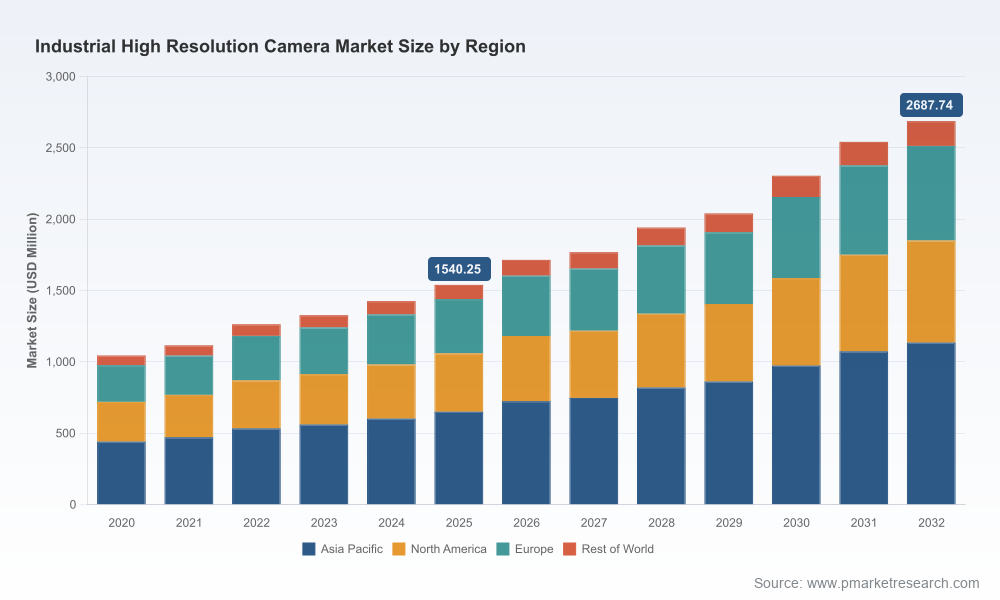

PW Consulting’s new Worldwide Industrial High Resolution Camera Market report delivers a pragmatic, decision-ready view of a market that has evolved from a niche instrumentation category into a foundational enabler for advanced automation, inspection and sensing. Measured in USD million, the market expanded from approximately 1,045.3 in 2020 to 1,540.3 in our 2025 base year and is forecast to grow to roughly 2,687.7 by 2032 — a compound annual growth rate (CAGR) of 8.28% for the 2026–2032 forecast period. The 2026 inflection point (forecast ~1,715.6 million) marks a transition from pandemic recovery dynamics toward broad-based adoption across manufacturing, logistics, life sciences and increasingly, autonomous systems.

Worldwide Industrial High Resolution Camera Market

Why this matters for corporate strategy in 2026

- Capital allocation and product roadmaps: With sustained mid-single-digit to high-single-digit CAGR and accelerating technology refresh cycles, R&D and capex plans must prioritize sensor-roadmap alignment, interface bandwidth (10/25/100GigE capabilities), and embedded intelligence to preserve product differentiation.

- Supply chain and procurement: Component lead times and tariff regimes are reshaping sourcing strategies. Manufacturers and end-users will need tactical inventory policies and diversified supplier pools to avoid production slowdowns.

- M&A and partnership timing: Moderate concentration (top-three and top-five supplier shares indicate a market where leadership is meaningful but acquisition opportunities remain) means 2026 is a window for strategic bolt-ons that deliver either scale in high-growth niches or capability in ultra-high-resolution and high-bandwidth architectures.

- Go-to-market and verticalization: Buyers increasingly prefer integrated vision systems (cameras + compute + optics + AI) over standalone sensors; commercial models that move up the value chain command premium margins.

What the report provides — practical, implementable content

PW Consulting designed this study as an operational playbook for executives, investors, product managers and procurement leads. The deliverables include:

Worldwide Industrial High Resolution Camera Market

- Market model (2020–2032) with base-year calibration and scenario sensitivity to component shortages, tariffs and demand shocks.

- Forward-looking technology roadmap that maps sensor architectures (CMOS variants, global/rolling hybrid shutters), interface evolution (GigE/10/25/100GigE, CoaXPress, USB3), and pixel/throughput trade-offs relevant for 2D/3D/line-scan use cases.

- Supplier diagnostic scorecards covering product breadth, integration readiness (embedded AI, IP67 ruggedization), vertical focus, manufacturing footprint, and liquidity/scale metrics for M&A prioritization.

- Manufacturing and procurement playbook outlining inventory hedging, dual-sourcing thresholds, and execution timelines to mitigate lead-time risk and tariff exposure.

- Commercial playbook for OEMs and systems integrators: pricing sensitivity matrices, channel strategies, and enterprise procurement templates for aligning SLAs with inspection throughput requirements.

- Scenario planning tools and three-tiered demand forecasts that allow users to stress-test strategies under constrained supply, aggressive technology adoption, or policy-driven market segregation.

Competitive landscape — where incumbents and challengers stand

The market’s competitive architecture balances established European and North American engineering houses with agile entrants in Asia focusing on price-performance and scale. Key strategic vectors we analyze in the report are: sensor partnerships, interface leadership, resolution and frame-rate specialization, IP in optics and software, and go-to-market channel depth.

Worldwide Industrial High Resolution Camera Market

- European systems and sensor integrators: Firms headquartered in Germany, Switzerland, Denmark and the Netherlands are profiled for their broad portfolios and deep channel relationships that favor precision metrology and factory automation. These players typically emphasize high-resolution area-scan and line-scan offerings with robust industrial interfaces.

- North American innovators: Canadian and U.S. companies are notable for pushing ultra-high-resolution and ultra-high-throughput architectures, with early commercial deployments in semiconductor inspection and volumetric imaging. Their strengths include advanced sensor integration, high-speed interfaces and strategic patents in camera electronics.

- Asian scale and integration: Large manufacturers based in China deliver competitive pricing and increasingly sophisticated product stacks, including optics and embedded software, enabling aggressive OEM partnerships in regional markets.

- Concentration and consolidation: Our CR3 and CR5 indicators point to a market where leading vendors capture a meaningful share — enough to influence standards and supply — yet still leave room for acquisitions and disruptive entrants. This positioning creates a tactical opportunity set for companies looking to scale via inorganic expansion or to acquire differentiated capabilities.

Recent technology and supply-chain developments — implications for 2026

- High-bandwidth camera launches: New ultra-high-resolution, multi-hundred-MP models with 10/25/100GigE connectivity are moving from lab demos to product lines. These platforms change host-compute requirements and create premium tiers in system pricing.

- Sensor ecosystem refresh: New CMOS image sensors with hybrid shutter modes and mid-resolution class options are entering mass production, enabling a broader set of industrial use cases and easing, in part, pressure on very-high-end sensor supply chains.

- 3D inline metrology improvements: New triangulation and line-density solutions multiply throughput for profile scanning, directly impacting throughput economics for automated inline inspection.

- Macro-policy and raw material pressures: Tariffs on semiconductor imports, U.S. export controls affecting advanced computing components, persistent sensor lead times and rising silicon-wafer costs collectively represent non-trivial headwinds that can increase BOM costs and extend time-to-revenue.

Strategic implications and 10 tactical recommendations for 2026

Based on our modeling and supplier diagnostics, PW Consulting recommends the following actions to preserve optionality and capture upside:

- Prioritize modular product architectures to decouple sensor availability from camera-level SKUs. Design for multiple sensor suppliers to reduce single-source risk.

- Lock predictable volumes through multi-year agreements with key sensor and component suppliers while building clause-based protections for tariffs and licensing delays.

- Invest selectively in software and AI wrappers that raise the switching cost for customers — quality inspection algorithms, anomaly-detection models and calibration suites.

- Target inorganic deals that either add high-resolution throughput capabilities or expand access to high-value verticals (semiconductor loadouts, medical imaging, automotive validation).

- Reassess channel compensation models — reward system integrators for selling integrated solutions (camera + compute + AI) rather than cameras alone.

- Validate pricing models against 10/25/100GigE-enabled product tiers and consider value-based pricing for high-bandwidth, low-latency systems used in wafer fabs and automotive validation labs.

- Create an internal “supply shock” playbook — pre-defining reorder points, emergency freight options, and substitute component lists to reduce downtime risk.

- Accelerate partnerships with sensor foundries or secure wafer commitments for vendors that control critical imaging nodes.

- Use scenario-driven demand forecasts from the report to guide hiring and factory ramp decisions — avoid over-committing capacity in the near term given tariff and export-control uncertainty.

- Monitor regulatory trajectories closely; map product roadmaps to jurisdictions with more predictable trade regimes to safeguard exports and IP flows.

How to use this report in boardroom and procurement workflows

Executives can immediately incorporate the report’s scenario model into budget cycles, using the supply-risk matrices and price-sensitivity tables to stress-test 2026 capex and procurement. Product teams can adapt sensor roadmaps and interface decisions to align with forecasted demand tiers. M&A teams should use the supplier scorecards and concentration metrics to identify target profiles that improve time-to-market for high-resolution capabilities.

Closing — the strategic value proposition

PW Consulting’s analysis translates the market’s trajectory — from USD million-scale base in 2025 to a near-term forecast above 1.7 billion in 2026 and long-term projection to nearly 2.7 billion by 2032 — into actionable choices for executives. The combination of technological velocity (new sensors, higher bandwidth interfaces), persistent supply-side friction (tariffs, lead times, wafer costs) and evolving customer preferences (integrated vision + compute solutions) creates both risk and differentiated opportunity. Firms that align modular product design, supply resilience and software differentiation will secure higher margins and defensible market positions as the industry expands.

For executives seeking the granular datasets, regional and application revenue splits, supplier scorecards, and downloadable scenario models referenced in this release, the report’s full content and supplementary tools are available on PW Consulting’s project page. The executive summary here is intentionally selective to preserve the strategic utility of the full intelligence package and to guide decision-makers to the complete dataset required for precise 2026 planning.

For detailed analysis of this topic, please visit the official page:Worldwide Industrial High Resolution Camera Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com