Worldwide K‑12 Art Course Market: Strategic Outlook for 2026 Decision‑Makers

PW Consulting’s latest market research brief, “Worldwide K‑12 Art Course Market (Base Year 2025) — Strategic Outlook 2026–2032,” distils actionable intelligence for executives, product leaders, investors, and district procurement teams preparing for the next phase of education transformation. Our analysis synthesizes historical performance (2020–2025), primary research with district and vendor stakeholders, and a forward‑looking quantitative model to project market dynamics through 2032. The headline: the global market has grown into a multi‑billion dollar sector and is set to accelerate, with a compounded annual growth rate (CAGR) of 8.52% across the 2026–2032 forecast window.

Worldwide K12 Art Course Market

Why this report matters for 2026 strategy

- Timing: 2026 marks the inflection when blended delivery models and creative‑tech integration shift from experimental pilots to procurement line items. Organizations that align product development, sales, and compliance resources now will capture disproportionate share as budgets reset.

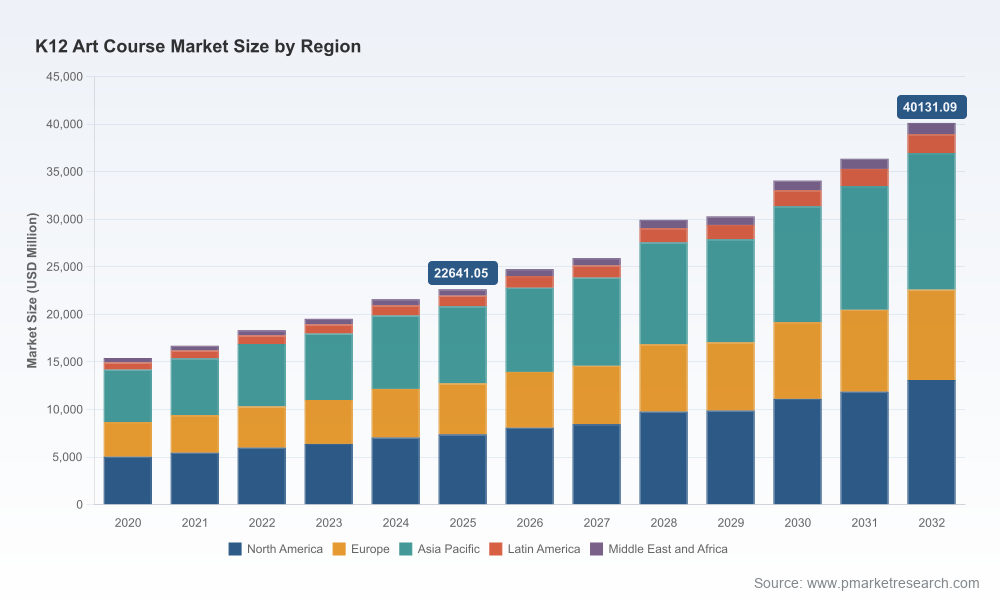

- Capital allocation: With the market reaching roughly USD 22.6 billion in 2025 and a projected trajectory toward roughly USD 40.1 billion by 2032, investors and corporate strategy teams must model longer sales cycles and bundling opportunities that leverage software, content, and services.

- Risk management: Regulatory clarification on student data privacy and the persistent dependence on certified arts educators create two simultaneous constraints — compliance complexity and human capital bottlenecks. These will define acceptable partnership models and technology adoption roadmaps in 2026.

Topline market signal — growth, scale, and structure

Our model indicates the global K‑12 art course market expanded steadily during 2020–2025 and entered 2026 with significant momentum. In 2025 the market scale was approximately USD 22.6 billion (expressed in revenue units consistent with our methodology), and under present assumptions we forecast growth to just over USD 40.1 billion by 2032 at a CAGR of 8.52%. Despite healthy growth, market concentration remains low — the three largest vendors account for roughly double‑digit share but well under levels that would suggest oligopolistic behavior (CR3 ≈ 11.4%; CR5 ≈ 16.8%). This fragmentation creates both a competitive opportunity for entrants and a diligence imperative for buyers evaluating vendor stability.

Worldwide K12 Art Course Market

Strategic implications for product and commercial leaders

- Design for educator augmentation, not replacement. K‑12 art instruction continues to rely heavily on certified teachers; successful digital products in 2026 will be those that reduce administrative burden, enable differentiated instruction, and support assessment without attempting to substitute the teacher’s role.

- Bundle software with curriculum and community. Buyers increasingly favour integrated solutions that combine content, creative tools, and teacher professional development. Standalone tools face margin pressure unless they can demonstrate seamless curriculum mapping and measurable learning outcomes.

- Prioritize privacy‑first architectures. With COPPA and FERPA enforcement clarified in recent years, platforms must embed verifiable consent workflows, robust data minimization, and clear controls for school‑authorized data use to be eligible for district procurement.

- Operationalize hybrid delivery. Schools will continue to mix in‑person, online, and hybrid modalities. Vendor roadmaps should include offline‑first lesson plans, synchronous and asynchronous delivery, and analytics that make hybrid teaching visible and actionable for administrators.

- Plan for creative‑tech adoption curves. The demand for digital and media arts, powered by industry tools, will grow faster than legacy elective models. Partnerships with creative software vendors and turnkey licensing options will unlock adoption at scale.

Competitive landscape — who matters and what they signal

The market map is characterized by a mix of curriculum incumbents, edtech platforms, creative‑software vendors, and niche community players. Our competitive analysis profiles leading and fast‑moving participants to explain where competitive advantage will emerge in 2026.

Worldwide K12 Art Course Market

- Curriculum and virtual school operators: Organizations delivering full K‑12 curricula through online or blended schools have embedded art offerings as part of their student experience. These players leverage scale and distribution to test curricular innovations and student engagement models.

- Creative software companies: Providers of industry‑grade creative tools are increasingly tailoring suites and licensing models for K‑12, enabling digital art courses that mirror professional workflows while adding classroom features such as simplified interfaces and classroom management.

- Platform and marketplace entrants: Community marketplaces for supplemental art classes and artifact hosting platforms create alternative routes to market. Their strength lies in breadth and flexibility, but they must demonstrate assessment validity and data governance to gain district trust.

- Niche and classical providers: Providers focused on fine arts, humanities‑infused curricula, or low‑cost classical syllabi are important demand anchors in certain buyer segments where values and local policy shape adoption.

Representative companies we examined in detail include established curriculum vendors and virtual school operators that have developed dedicated art offerings, creative‑software incumbents adapting licensing for schools, digital hosting and exhibition platforms for student work, and marketplaces that facilitate live instructor‑led supplemental art instruction. Recent corporate actions — such as national student art competitions, districtwide arts education plan rollouts, and curriculum integration partnerships — validate our thesis that both product and programmatic levers are being used to accelerate engagement and procurement.

Regulatory and operational dynamics to factor into 2026 plans

- Data privacy enforcement is non‑negotiable: Updated guidance clarifies that schools may consent to certain data processing only when strictly educational and not for commercial targeting. Product teams must segregate telemetry used for product improvement from data that could be construed as advertising‑related.

- FERPA implications for third‑party vendors: Vendor contracts and data processing agreements must explicitly address educational records and disclosure limitations, with audit rights and clear data retention policies.

- Human capital constraints: The labor intensity of arts instruction means that scale will depend on staffing models — certified teacher deployment, professional development pathways, and the intelligent use of paraprofessionals and community instructors to extend access.

Report contents — practical deliverables inside PW Consulting’s brief

We designed the report to be immediately usable by commercial teams, district leaders, and investors. Key operational sections include:

- Market sizing and forecasting methodology (transparent assumptions and scenario modelling for 2026–2032)

- Demand drivers and elasticity analysis, covering budget cycles, policy interventions, and parent‑driven supplemental demand

- Product and technology map, including maturity assessment for creative‑tech, LMS integration pathways, and data architectures compliant with K‑12 regulations

- Go‑to‑market playbooks for vendor types: district procurement strategies, channel partnerships, and direct‑to‑consumer models for supplemental education marketplaces

- Pricing archetypes, revenue levers (subscription, licensing, services), and margin benchmarks

- M&A and partnership screening: a prioritised list of capability adjacencies and acquisition targets structured to accelerate content, technology, or distribution

- Case studies and procurement templates tailored for district RFPs and supplier due diligence

Each section is accompanied by executable templates, prioritisation matrices, and a decision tree that helps organisations translate market projections into two‑year tactical plans and five‑year strategic roadmaps.

How to use these insights in 2026 planning cycles

- For product leaders: Allocate R&D to privacy‑preserving analytics, educator usability, and interoperability with district LMS/Roster systems. Prototype partnerships with creative‑software vendors and pilot co‑licensed lesson bundles.

- For sales and GTM heads: Reframe value propositions around district pain points — administrator visibility, staff PD, and measurable arts outcomes. Structure commercial pilots to transition into multi‑year implementations.

- For investors and corporate development: Look for targets that provide immediate content depth, teacher enablement capabilities, or licensing relationships with major creative‑software providers. Fragmentation presents roll‑up opportunities, but diligence must validate recurring revenue quality.

- For district leaders: Use the report’s procurement templates to assess vendor compliance with COPPA/FERPA, integrate arts metrics into broader learning outcome dashboards, and plan workforce investments to sustain arts programming at scale.

Why PW Consulting — evidence, not conjecture

Our analysis combines longitudinal market data, supplier and buyer interviews, and a reproducible forecasting engine. We explicitly stress‑test scenarios for funding shocks, regulatory tightening, and rapid creative‑tech adoption so that clients receive not only a point estimate for 2026 budgeting but also contingency pathways for downside and upside cases.

Next steps and where to get the full intelligence

This article provides a strategic preview — a “trailer” designed to surface the most consequential insights for 2026 decision cycles while preserving the granular datasets, segmentation tables, and vendor benchmarking that you will need to act. For access to the full report, downloadable datasets, and custom advisory packages (including bespoke district readiness assessments, M&A target screens, and pilot design workshops), please visit the PW Consulting research portal. Our teams are also available for one‑on‑one briefings to walk through the forecast model and align findings to your specific operating context.

In a market on track to nearly double in size over the coming decade, 2026 is the year to convert strategic intent into operational commitments. Those who design for teachers, embed privacy by design, and bundle content with demonstrable outcomes will define leadership in the K‑12 art education market.

For detailed analysis of this topic, please visit the official page:Worldwide K12 Art Course Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com